Strategi Perdagangan Dua Hala Panjang dan Pendek Talian Ayunan Dwi Landasan RSI

Gambaran Keseluruhan

Strategi Perdagangan Dua Hala Panjang Pendek dengan Landasan Berganda RSI ialah strategi yang menggunakan penunjuk RSI untuk urus niaga dua hala. Strategi ini memanfaatkan prinsip terlebih beli dan terlebih jual penunjuk RSI, digabungkan dengan penetapan landasan berganda dan isyarat perdagangan purata bergerak, untuk membuka dan menutup kedudukan secara dua hala dengan cekap.

Prinsip Strategi

Strategi ini terutamanya membuat keputusan perdagangan berdasarkan prinsip terlebih beli dan terlebih jual penunjuk RSI. Strategi mula-mula mengira nilai penunjuk RSI, vrsi, serta landasan atas sn dan landasan bawah ln bagi landasan berganda. Apabila nilai RSI menembusi ke bawah landasan bawah ln, isyarat beli dihasilkan; apabila nilai RSI menembusi ke atas landasan atas sn, isyarat jual dihasilkan.

Strategi juga mengesan perubahan kenaikan dan penurunan lilin (K-line) untuk menjana isyarat beli dan jual selanjutnya. Secara khusus, apabila lilin menembusi ke atas dari bawah, isyarat beli longLogic dihasilkan; apabila lilin menembusi ke bawah dari atas, isyarat jual shortLogic dihasilkan. Selain itu, strategi menyediakan suis parameter yang membolehkan perdagangan hanya beli, hanya jual, atau penyongsangan isyarat.

Selepas isyarat beli dan jual dihasilkan, strategi akan mengira bilangan isyarat dan mengawal bilangan pembukaan kedudukan. Melalui parameter, peraturan penambahan kedudukan yang berbeza boleh ditetapkan. Syarat penutupan kedudukan termasuk ambil untung, henti rugi, henti rugi bergerak, dsb., dengan peratusan ambil untung dan henti rugi yang boleh ditetapkan.

Secara ringkasnya, strategi ini menggabungkan pelbagai teknik seperti penunjuk RSI, persilangan purata bergerak, penambahan kedudukan statistik, ambil untung dan henti rugi, untuk merealisasikan perdagangan dua hala automatik panjang dan pendek.

Kelebihan Strategi

- Menggunakan prinsip terlebih beli dan terlebih jual penunjuk RSI untuk membina kedudukan beli dan jual pada tahap yang munasabah.

- Penetapan landasan berganda mengelakkan isyarat palsu. Landasan atas menghalang penutupan awal kedudukan beli, landasan bawah menghalang penutupan awal kedudukan jual.

- Isyarat perdagangan purata bergerak menapis penembusan palsu. Isyarat hanya dihasilkan apabila harga saham menembusi purata bergerak, mengelakkan isyarat palsu.

- Bilangan isyarat dan bilangan penambahan kedudukan dikira untuk mengawal risiko.

- Peratusan ambil untung dan henti rugi boleh disesuaikan, menjadikan risiko dan pulangan terkawal.

- Henti rugi bergerak mengikuti kedudukan untuk mengunci keuntungan selanjutnya.

- Boleh berdagang hanya beli, hanya jual, atau menyongsangkan isyarat, menyesuaikan dengan keadaan pasaran yang berbeza.

- Sistem perdagangan automatik mengurangkan kos operasi manual.

Risiko Strategi

- Penunjuk RSI mempunyai risiko kegagalan pembalikan. RSI yang memasuki zon terlebih beli atau terlebih jual tidak semestinya akan berbalik.

- Titik ambil untung dan henti rugi tetap mempunyai risiko terperangkap. Penetapan yang tidak sesuai boleh menyebabkan henti rugi atau ambil untung pramatang.

- Bergantung pada penunjuk teknikal, terdapat risiko pengoptimuman parameter. Parameter penunjuk yang tidak sesuai akan menjejaskan prestasi strategi.

- Pelbagai syarat yang dicetuskan serentak boleh menyebabkan risiko kehilangan pesanan.

- Sistem perdagangan automatik mempunyai risiko ralat luar biasa.

Untuk mengatasi risiko di atas, penambahbaikan boleh dilakukan dengan mengoptimumkan tetapan parameter, melaraskan strategi henti rugi dan ambil untung, menambah penapisan kecairan, mengoptimumkan logik penjanaan isyarat, dan menambah pemantauan ralat luar biasa.

Arah Pengoptimuman Strategi

- Menguji parameter kitaran yang berbeza untuk mengoptimumkan parameter penunjuk RSI.

- Menguji tetapan peratusan ambil untung dan henti rugi yang berbeza.

- Menambah penapisan volum dagangan atau kadar pulangan untuk mengelakkan kecairan yang tidak mencukupi.

- Mengoptimumkan logik penjanaan isyarat dan menambah baik cara persilangan purata bergerak.

- Menambah ujian semula berbilang tempoh masa untuk mengesahkan kestabilan.

- Mempertimbangkan untuk menambah penunjuk lain untuk mengoptimumkan prestasi isyarat.

- Menambah strategi pengurusan kedudukan.

- Menambah pemantauan ralat luar biasa.

- Mengoptimumkan algoritma henti rugi automatik.

- Mempertimbangkan untuk menambah pembelajaran mesin untuk meningkatkan strategi.

Kesimpulan

Strategi Perdagangan Dua Hala Panjang Pendek dengan Landasan Berganda RSI merealisasikan perdagangan dua hala automatik dengan menggabungkan pelbagai teknik seperti penunjuk RSI, pembukaan kedudukan statistik dan prinsip henti rugi. Strategi ini mempunyai kebolehsesuaian yang tinggi; pengguna boleh melaraskan parameter mengikut keperluan untuk menyesuaikan dengan keadaan pasaran yang berbeza. Pada masa yang sama, strategi ini mempunyai ruang untuk penambahbaikan, seperti mengoptimumkan tetapan parameter, strategi kawalan risiko, dan logik penjanaan isyarat, menjadikan strategi lebih stabil dan boleh dipercayai. Secara keseluruhan, strategi ini menyediakan pengguna dengan penyelesaian perdagangan kuantitatif yang agak cekap.

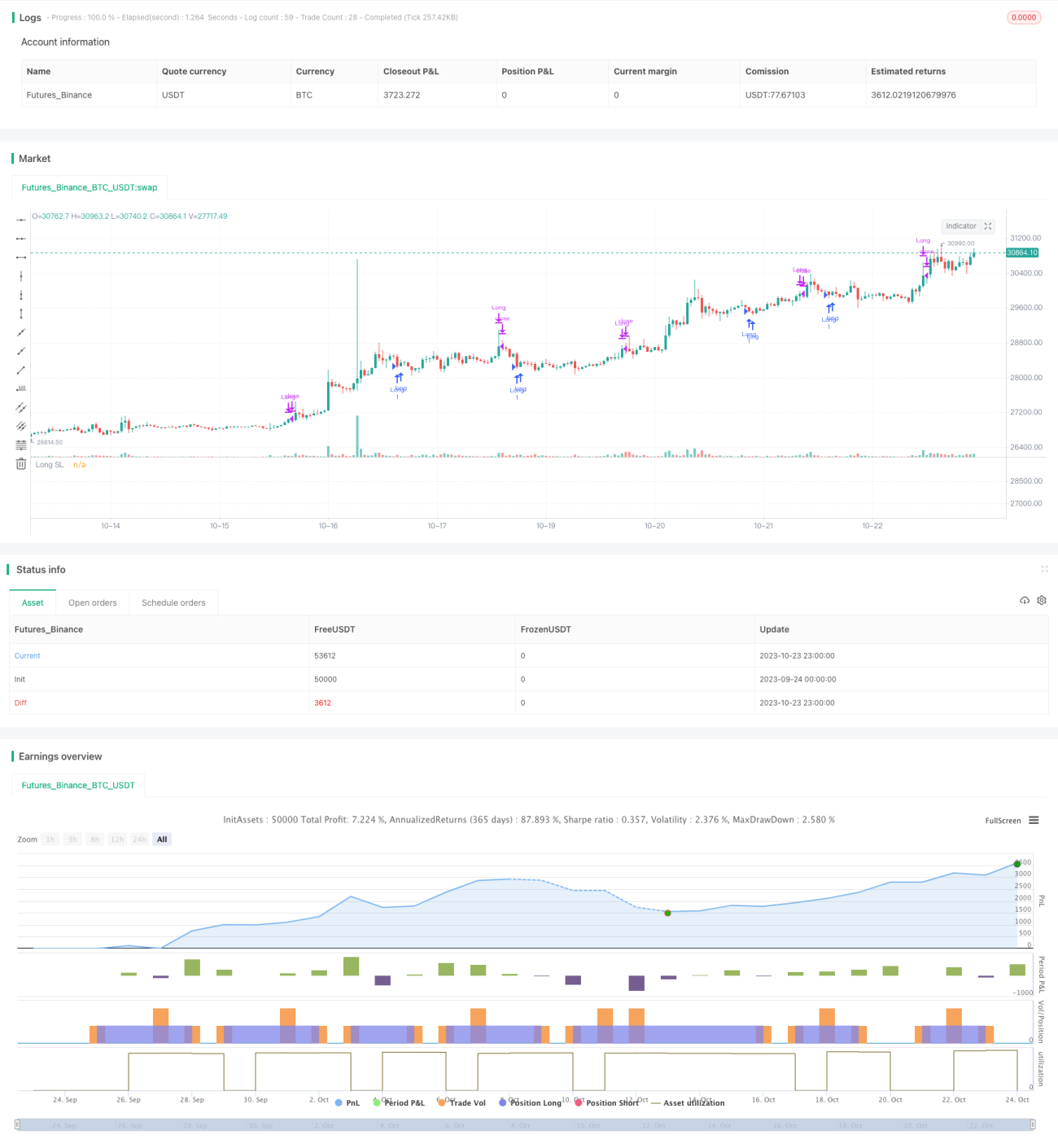

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1