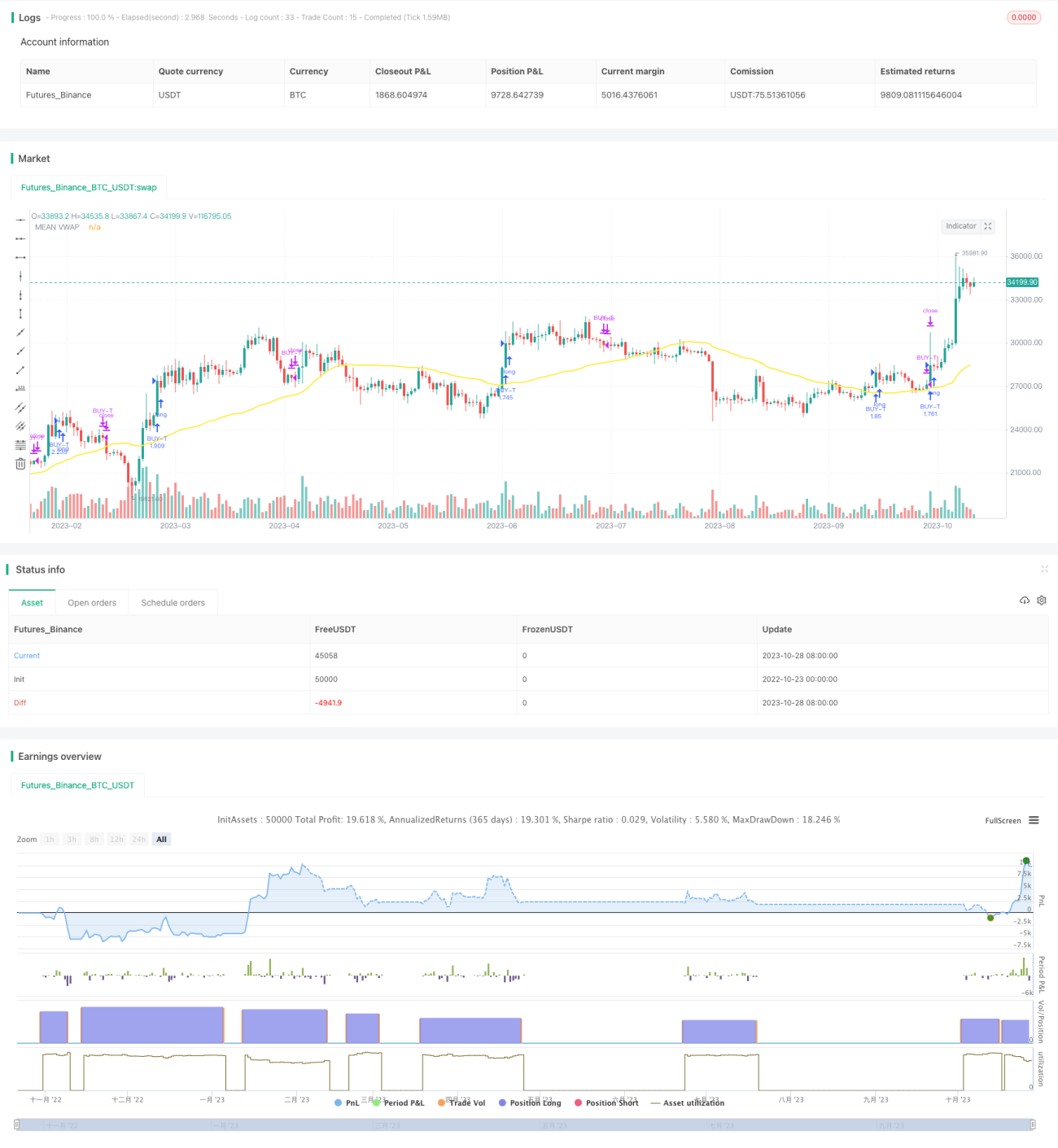

Strategi Perdagangan Algoritma Penjejakan Dua Garis

Gambaran Keseluruhan

Strategi ini terutamanya menggunakan prinsip persilangan purata bergerak, digabungkan dengan isyarat pembalikan RSI, dan algoritma penjejakan dua garis tersuai untuk melaksanakan dagangan penjejakan persilangan purata bergerak. Strategi ini menjejaki persilangan dua purata bergerak dengan tempoh berbeza, satu purata bergerak pantas untuk mengikuti trend jangka pendek, dan satu purata bergerak perlahan untuk mengikuti trend jangka panjang. Apabila purata bergerak pantas melintasi ke atas purata bergerak perlahan, ini menunjukkan trend jangka pendek menaik, dan boleh beli; apabila purata bergerak pantas melintasi ke bawah purata bergerak perlahan, ini menunjukkan trend jangka pendek berakhir, dan harus ditutup.

Prinsip Strategi

-

Kira dua set garis purata VWAP dengan parameter berbeza, masing-masing mewakili trend jangka panjang dan trend jangka pendek

- Garis langit perlahan dan garis asas mengira trend jangka panjang

- Garis langit pantas dan garis asas mengira trend jangka pendek

-

Ambil purata dua set garis langit dan garis asas masing-masing sebagai purata bergerak perlahan dan purata bergerak pantas

-

Kira indikator Bollinger Band untuk menilai pengukuhan dan penembusan

- Garis tengah adalah purata purata bergerak pantas dan purata bergerak perlahan

- Jalur atas dan bawah Bollinger digunakan untuk menilai penembusan

-

Kira indikator TSV untuk menilai tenaga volum dagangan

- TSV > 0 menunjukkan kuasa kenaikan lebih besar daripada kuasa penurunan

- TSV > EMA(TSU) menunjukkan peningkatan kuasa

-

Kira indikator RSI untuk menilai terlebih beli dan terlebih jual

- RSI < 30 adalah zon terlebih jual, boleh beli

- RSI > 70 adalah zon terlebih beli, harus jual

-

Syarat masuk:

- Purata bergerak pantas melintasi ke atas purata bergerak perlahan

- Harga tutup melintasi ke atas jalur atas Bollinger

- TSV > 0 dan TSV > EMA(TSV)

- RSI < 30

-

Syarat keluar:

- Purata bergerak pantas melintasi ke bawah purata bergerak perlahan

- RSI > 70

Analisis Kelebihan

-

Menggunakan sistem dua purata bergerak, dapat menangkap trend jangka panjang dan jangka pendek serentak

-

Indikator RSI mengelakkan pembelian di zon terlebih beli dan penjualan di zon terlebih jual

-

Indikator TSV memastikan volum dagangan yang mencukupi untuk menyokong trend

-

Menggunakan Bollinger Band untuk menilai titik penembusan utama

-

Gabungan pelbagai indikator berkesan menapis penembusan palsu

Analisis Risiko

-

Sistem purata bergerak mudah menghasilkan isyarat palsu, memerlukan bantuan indikator untuk menapis

-

Parameter indikator RSI perlu dioptimumkan, jika tidak mungkin terlepas titik beli/jual

-

Indikator TSV juga sensitif terhadap parameter, perlu diuji dengan teliti

-

Penembusan jalur atas Bollinger mungkin adalah penembusan palsu, perlu disahkan

-

Gabungan pelbagai indikator menyukarkan pengoptimuman parameter, mudah menyebabkan overfitting

-

Data latihan dan ujian yang tidak mencukupi boleh menyebabkan overfitting

Arah Pengoptimuman

-

Uji lebih banyak parameter kitaran untuk mencari kombinasi parameter terbaik

-

Cuba gantikan atau gabungkan dengan indikator lain seperti MACD, KD bersama RSI

-

Pengoptimuman parameter perlu memanfaatkan sepenuhnya analisis walk forward

-

Tambah strategi stop loss untuk mengawal kerugian setiap dagangan

-

Pertimbangkan untuk menambah model pembelajaran mesin untuk membantu penilaian isyarat

-

Laraskan parameter untuk pasaran yang berbeza, jangan terlalu bergantung pada satu kombinasi parameter

Kesimpulan

Strategi ini menangkap trend jangka panjang dan jangka pendek melalui sistem dua purata bergerak, sambil menggunakan pelbagai indikator seperti RSI, TSV, Bollinger Band untuk menapis isyarat. Kelebihan strategi adalah dapat mengikuti trend dan menangkap gelombang kenaikan jangka panjang. Walau bagaimanapun, terdapat juga risiko isyarat palsu, memerlukan pengoptimuman parameter lanjut dan kawalan stop loss untuk mengurangkan risiko. Secara keseluruhan, strategi ini menggabungkan penjejakan trend dan indikator pembalikan, memberikan hasil yang baik dalam pasaran menaik jangka panjang, tetapi perlu pelarasan parameter untuk pasaran yang berbeza.

- 1