Estratégia quantitativa de acompanhamento de tendência baseada no SAR

Visão Geral

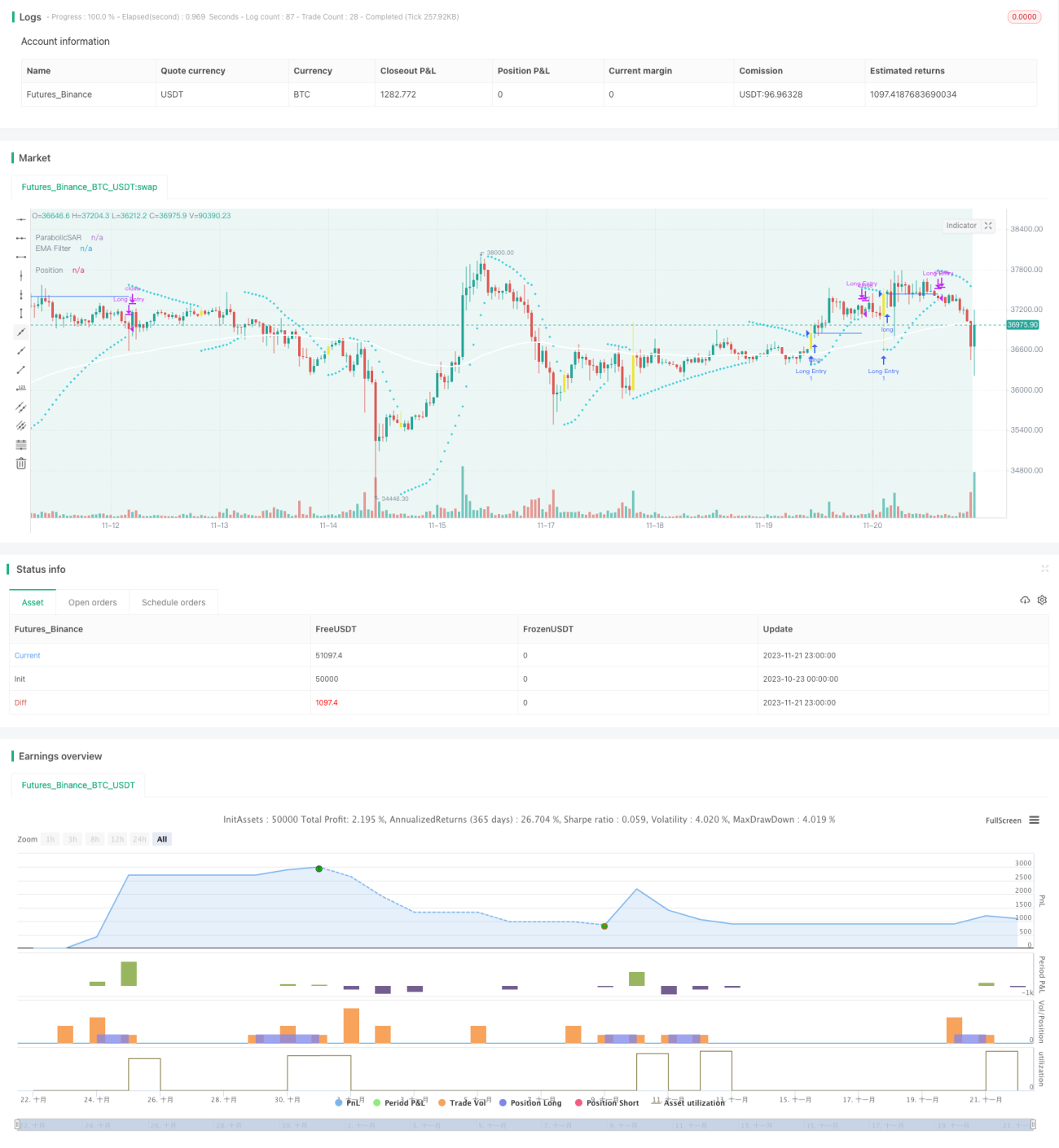

A Estratégia de Gap Especulativo é uma estratégia de negociação quantitativa que segue tendências. Ela usa a curva suavizada SAR como principal sinal de negociação, complementada por múltiplos filtros como EMA, Momentum Squeeze e Oscilador de Volatilidade. Através da configuração dos parâmetros SAR, identifica pontos de reversão de tendência para realizar o acompanhamento de tendência de baixo risco. Esta é uma estratégia muito adequada para investimentos de médio e longo prazo.

Princípio da Estratégia

A estratégia utiliza o SAR parabólico como principal indicador de sinal de negociação. O SAR consegue identificar efetivamente os pontos de reversão da tendência de preços. Quando o sinal do SAR muda, indica uma reversão da tendência. Esta estratégia geralmente emite sinais de compra ou venda quando o SAR se inverte.

Além disso, a estratégia também oferece a opção de rompimento do SAR. Ou seja, antes que o SAR se inverta completamente, o preço já ultrapassou o último valor do SAR, gerando um sinal. Isso pode aumentar ainda mais a sensibilidade da estratégia.

Para filtrar sinais falsos, a estratégia também introduz três filtros auxiliares: EMA, Momentum Squeeze e Oscilador de Volatilidade, que podem ser usados individualmente ou em combinação para confirmar a tendência de preços e a confiabilidade dos sinais de negociação.

Por fim, a estratégia oferece três modos de stop loss e take profit: stop loss fixo, take profit fixo e stop loss baseado na relação risco-retorno. Isso permite que a estratégia se adapte de forma flexível às características de diferentes tipos de ativos negociados.

Análise de Vantagens

-

O SAR consegue identificar com precisão as reversões de tendência de preços e capturar novas tendências de forma oportuna, sendo adequado para acompanhamento de tendências de médio e longo prazo.

-

A configuração de múltiplos filtros reduz a probabilidade de falsos rompimentos, aumentando a confiabilidade dos sinais.

-

Configuração simples e flexível, permitindo personalizar parâmetros para se adaptar a diferentes ativos.

-

Oferece várias formas de take profit e stop loss, permitindo buscar um equilíbrio entre risco e retorno.

-

Pode ser conectado diretamente a robôs de negociação, possibilitando a automação das operações.

Análise de Riscos

-

Em mercados sem tendência definida, podem ocorrer mais sinais falsos e negociações ineficazes.

-

Parâmetros SAR configurados inadequadamente também podem afetar a precisão dos sinais.

-

Como estratégia de acompanhamento de tendência, em mercados com grandes oscilações, é fácil atingir o nível de stop loss.

Para mitigar os riscos acima, pode-se ajustar adequadamente os parâmetros SAR ou os filtros, reduzindo a probabilidade de negociações ineficazes. Também é possível ampliar os limites de stop loss para suportar maiores flutuações de mercado.

Direções de Otimização

-

Otimização dos parâmetros SAR. É possível otimizar os parâmetros de passo e incremento do SAR com base em dados históricos de backtest, obtendo uma estratégia de negociação mais estável e eficiente.

-

Introdução de indicadores de julgamento de tendência. Adicionar indicadores auxiliares como MACD, DMI, etc., para melhorar a capacidade de identificação de tendências.

-

Otimização da relação risco-retorno. Ajustar as porcentagens fixas de take profit e stop loss e o parâmetro de relação risco-retorno, assumindo riscos adequadamente maiores para obter retornos mais altos.

-

Adição de ativos de câmbio. Atualmente, a estratégia suporta apenas negociação de criptomoedas; pode ser expandida para incluir ativos de câmbio, commodities e mercados de ações.

Resumo

O Gap Especulativo é uma estratégia quantitativa de acompanhamento de tendência muito prática. Ela é responsiva, com julgamento de sinais confiável, e pode obter retornos estáveis e de longo prazo por meio do gerenciamento de stop loss e take profit. A otimização adequada de parâmetros e regras pode aumentar ainda mais a eficiência da estratégia. Esta é uma estratégia quantitativa eficiente que vale a pena utilizar a longo prazo.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1