Estratégia de momentum e reversão baseada em modelo multifatorial

Visão Geral

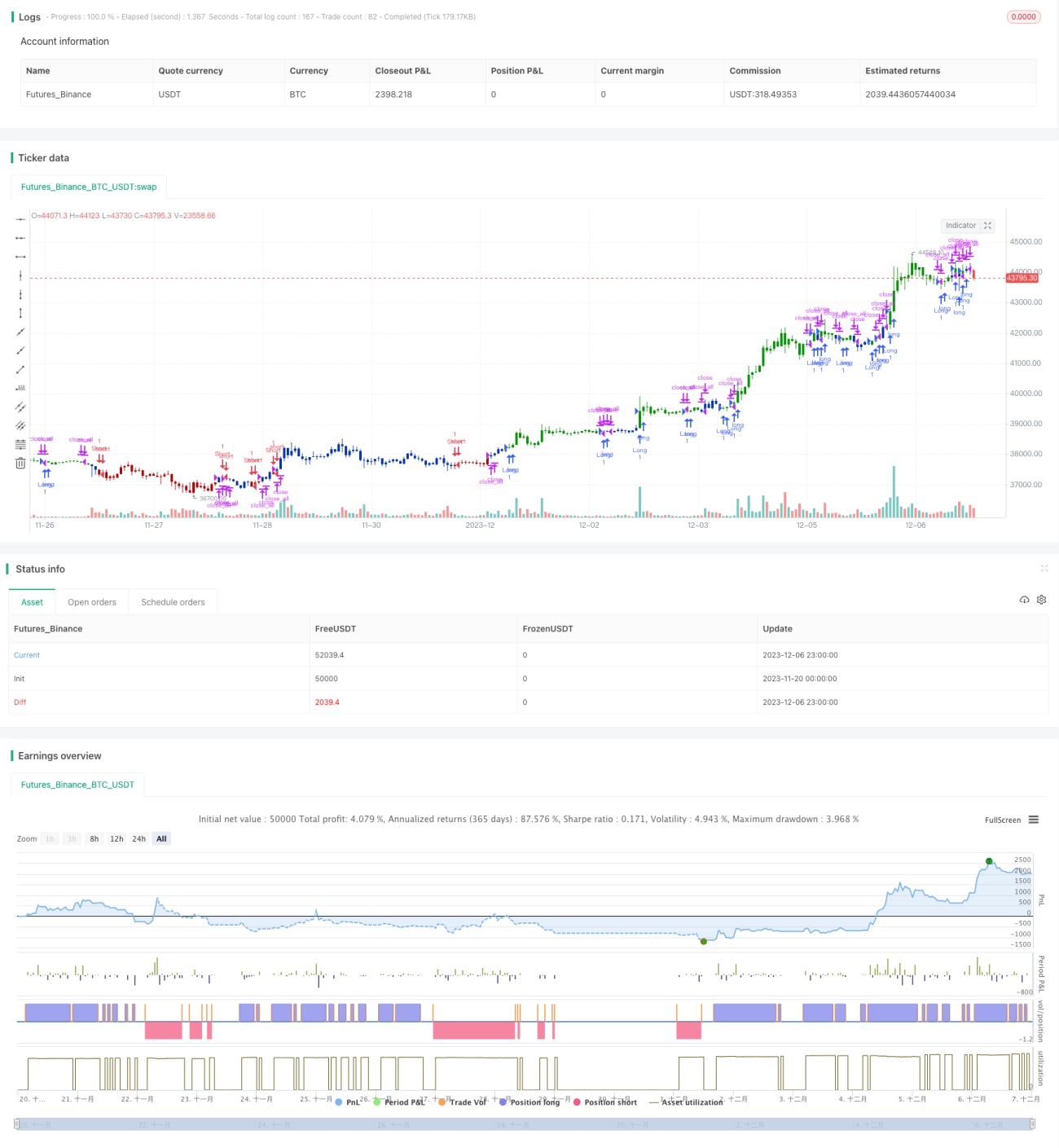

A estratégia de momentum reversão com modelo multifatorial combina o modelo multifatorial com a estratégia de momentum reversão para obter retornos mais estáveis e maiores. A estratégia utiliza a reversão 123 e o índice de ressonância como dois sinais independentes, e abre uma posição quando ambos os sinais estão consistentes.

Princípio da Estratégia

A estratégia de momentum reversão com modelo multifatorial é composta por duas subestratégias: a estratégia de reversão 123 e a estratégia do índice de ressonância.

A estratégia de reversão 123 baseia-se na alta ou baixa consecutiva do preço em 2 dias, combinada com o indicador STOCH para avaliar se o mercado está superesfriado ou superaquecido, gerando sinais de negociação. Especificamente, quando o preço sobe por 2 dias consecutivos e a linha lenta do STOCH de 9 dias está abaixo de 50, a visão é de alta; quando o preço cai por 2 dias consecutivos e a linha rápida do STOCH de 9 dias está acima de 50, a visão é de baixa.

A estratégia do índice de ressonância utiliza a sobreposição de médias móveis de diferentes períodos e indicadores osciladores para determinar a direção e a força da tendência. Inclui métodos como ponderação linear e soma senoidal para avaliar de forma abrangente a situação de alta ou baixa. Esse indicador é classificado em níveis, retornando de 1 a 9 para indicar uma forte tendência de alta, e de -1 a -9 para indicar uma forte tendência de baixa.

Por fim, a estratégia escolhe abrir uma posição comprada ou vendida quando os sinais de ambos os indicadores estão consistentes.

Análise de Vantagens

A estratégia de momentum reversão com modelo multifatorial combina fatores de reversão e fatores de momentum, capturando oportunidades de reversão enquanto segue a tendência e evita falsos rompimentos, resultando em uma maior taxa de acerto. As vantagens da estratégia são refletidas em:

-

A estratégia de reversão 123, como fonte de sinal de reversão, consegue capturar ganhos excessivos provenientes de reversões de curto prazo.

-

O índice de ressonância determina a direção e a força da tendência, evitando o risco de perdas causadas por um espaço de reversão excessivamente grande.

-

A combinação de ambos complementa as vantagens e suprir as deficiências até certo ponto, melhorando a qualidade dos sinais.

-

Em comparação com um modelo único, a combinação multifatorial pode aumentar a estabilidade da estratégia.

Análise de Riscos

Embora a estratégia de momentum reversão com modelo multifatorial tenha certas vantagens, ainda existem os seguintes riscos:

-

A reversão não é concluída, e o preço volta a cair novamente, causando perdas. Pode-se ajustar adequadamente o stop loss para prevenir.

-

Quando os sinais dos dois indicadores não estão consistentes, a direção não pode ser determinada. Pode-se ajustar os parâmetros para aumentar a correspondência entre eles.

-

O modelo é muito complexo, com muitos parâmetros, difícil de ajustar e otimizar.

-

É necessário prestar atenção a vários submodelos ao mesmo tempo, o que aumenta a dificuldade operacional e a pressão psicológica em negociações reais. Pode-se introduzir alguns elementos de negociação automatizada para aliviar a carga operacional.

Direções de Otimização

A estratégia de momentum reversão com modelo multifatorial pode ser otimizada nos seguintes aspectos:

-

Ajustar os parâmetros da estratégia de reversão 123 para tornar os sinais de reversão mais precisos e confiáveis.

-

Ajustar os parâmetros do índice de ressonância para que a tendência determinada se aproxime mais da tendência real.

-

Introduzir algoritmos de aprendizado de máquina para otimizar automaticamente a combinação de parâmetros.

-

Adicionar um módulo de gerenciamento de posição para tornar o ajuste de posição mais quantitativo e sistemático.

-

Adicionar um módulo de stop loss. Controlar efetivamente a perda de cada operação definindo um preço de stop loss com antecedência.

Resumo

A estratégia de momentum reversão com modelo multifatorial utiliza de forma abrangente fatores de reversão e fatores de momentum. Com base na garantia de alta qualidade do sinal, a sobreposição de múltiplos fatores obtém uma maior taxa de acerto. Esta estratégia possui a vantagem dupla de capturar oportunidades de reversão e seguir a tendência, sendo uma estratégia quantitativa eficiente e estável. No futuro, pode ser continuamente otimizada em termos de ajuste de parâmetros, controle de risco, etc., para melhorar ainda mais a relação risco-retorno da estratégia.

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 11/11/2019

// This is combo strategies for get a cumulative signal. - 1