Estratégia de Trading Bidirecional ADX

Visão Geral

A estratégia de negociação ADX Bidirecional é uma estratégia quantitativa que utiliza o indicador ADX (Average Directional Index) para realizar negociações em ambas as direções. Ela calcula o ADX juntamente com a diferença entre os indicadores DIPlus e DIMinus, define um limite para determinar se um sinal de negociação é gerado e realiza operações de compra e venda para obter lucros.

Princípios da Estratégia

- Calcular o True Range (Faixa Real)

- Calcular o Direcional Movement Plus (Movimento Direcional Positivo) e o Direcional Movement Minus (Movimento Direcional Negativo)

- Calcular o Smoothed True Range (Faixa Real Suavizada)

- Calcular o Smoothed Directional Movement Plus (Movimento Direcional Positivo Suavizado) e o Smoothed Directional Movement Minus (Movimento Direcional Negativo Suavizado)

- Calcular os indicadores DIPlus, DIMinus e ADX

- Calcular a diferença entre DIPlus e ADX, e entre DIMinus e ADX

- Definir os limiares de diferença para negociações de compra e venda

- Quando a diferença for maior que o limiar, determina-se que um sinal de negociação foi gerado

- Gerar ordens de compra e venda

O núcleo desta estratégia está em usar indicadores de movimento direcional como o ADX para julgar a direção e a força da tendência, combinando com a regra de diferença para definir limiares e realizar negociações automáticas.

Análise de Vantagens

- Usar o ADX para julgar a direção da tendência permite capturar com precisão as tendências do mercado

- A aplicação da regra de diferença pode filtrar efetivamente sinais falsos

- Negociação em ambas as direções permite capturar plenamente oportunidades de alta e baixa

- Negociação totalmente automática, sem necessidade de intervenção manual

- A lógica da estratégia é clara, fácil de entender e modificar

Análise de Riscos

- O indicador ADX apresenta atraso, podendo perder pontos de reversão de tendência

- O risco de negociação em ambas as direções é maior, podendo ampliar as perdas

- Parâmetros inadequados podem levar a negociações excessivas

- Os dados de backtest não representam o mercado real, portanto, o risco de negociação ao vivo ainda existe

Soluções:

- Combinar com outros indicadores para confirmar os sinais de negociação

- Otimizar parâmetros e controlar a frequência de negociação

- Gerenciar rigorosamente o tamanho da posição (Position Sizing) para controlar as posições

Direções de Otimização

- Otimizar os parâmetros do ADX para melhorar sua sensibilidade

- Adicionar outros indicadores para filtrar sinais

- Aplicar algoritmos de aprendizado de máquina para otimizar parâmetros

- Utilizar estratégias avançadas de stop loss para controlar o risco de perdas

- Combinar previsões de modelos para obter sinais de negociação mais precisos

Resumo

A estratégia de negociação ADX Bidirecional é, em geral, uma estratégia quantitativa muito prática. Ela utiliza o indicador ADX para identificar tendências e capturar oportunidades de negociação em ambas as direções. Ao mesmo tempo, aplica a regra de diferença para garantir a validade dos sinais. A lógica da estratégia é clara e simples, fácil de modificar e otimizar, sendo uma estratégia de acompanhamento de tendências bidirecional. Com a otimização adequada de parâmetros, aplicação de estratégias de stop loss e filtragem de sinais, é possível aumentar ainda mais a estabilidade e a lucratividade da estratégia.

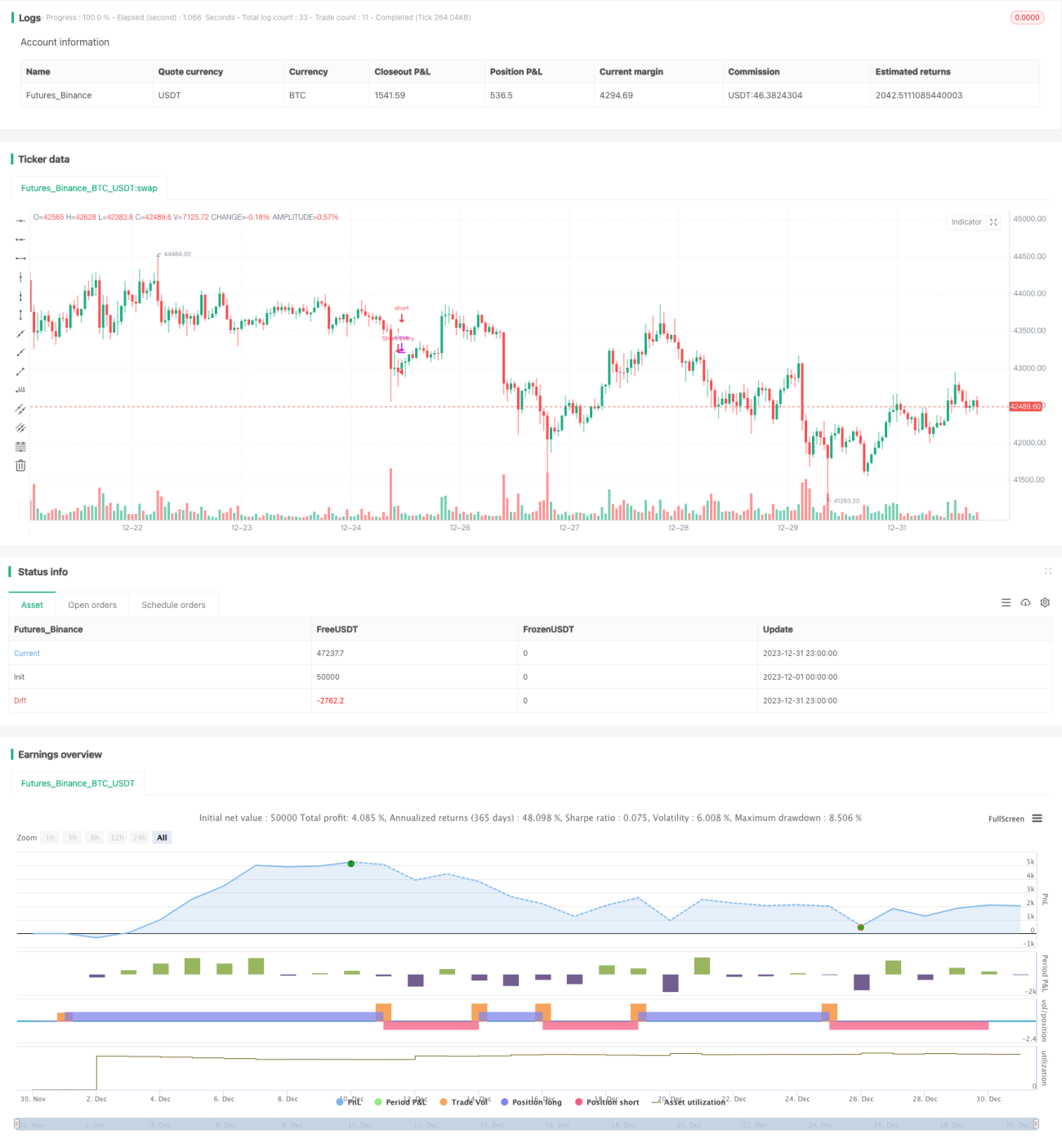

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1