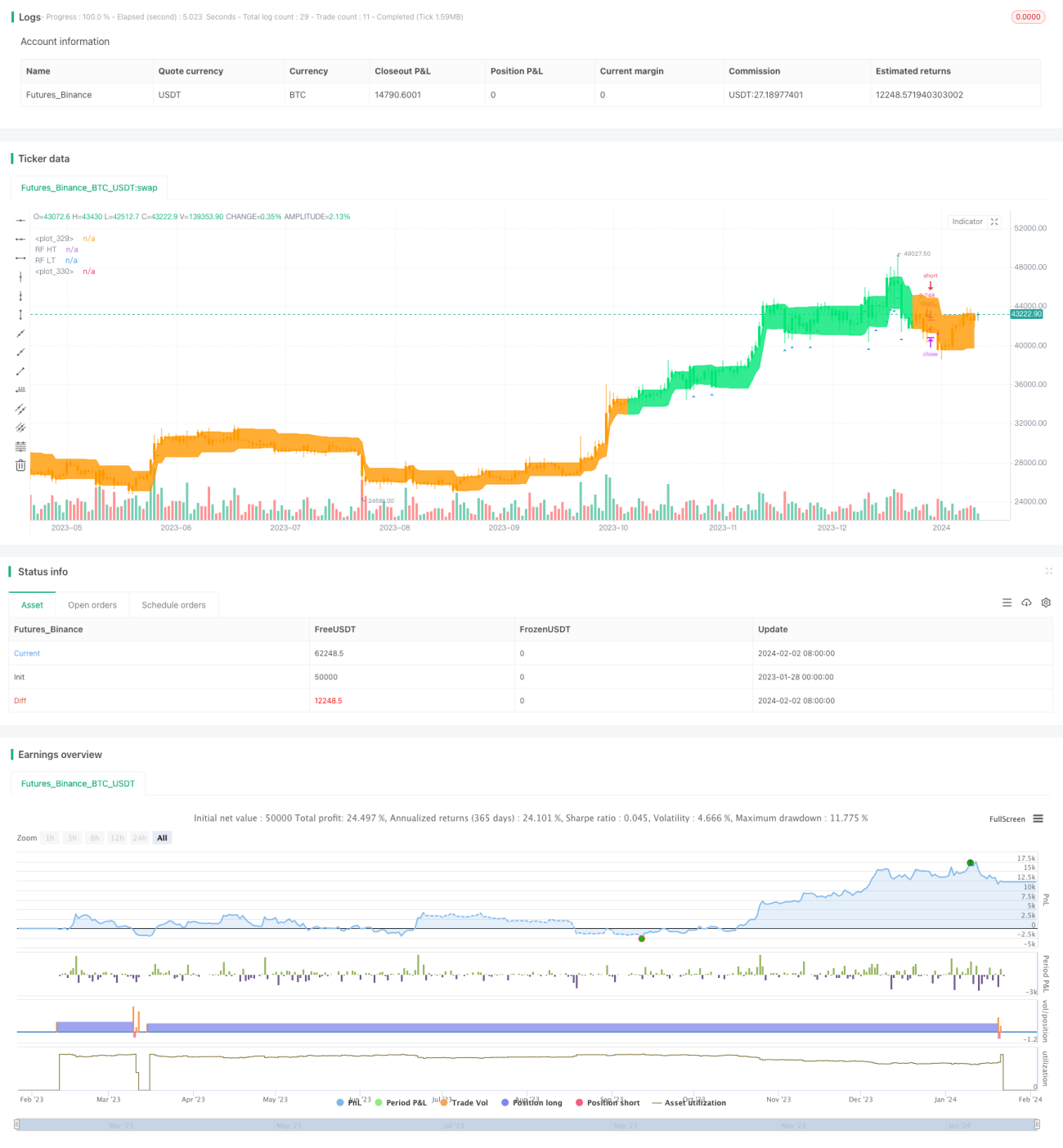

Estratégia de trading quantitativo baseada em média móvel dinâmica de múltiplos ativos

Visão Geral

Esta estratégia utiliza sinais combinados de múltiplos indicadores técnicos para realizar negociações dinâmicas em ativos como ações e criptomoedas. A estratégia pode identificar automaticamente as tendências do mercado e realizar o rastreamento de tendências. Ao mesmo tempo, a estratégia incorpora um mecanismo de stop loss para controlar o risco.

Princípio da Estratégia

Esta estratégia utiliza principalmente vários indicadores, como Médias Móveis, Índice de Força Relativa (RSI), Average True Range (ATR) e Índice de Movimento Direcional (ADX), para gerar sinais de negociação por meio da combinação de indicadores.

Especificamente, a estratégia primeiro forma sinais de cruzamento (golden cross e death cross) usando duas médias móveis. O período da média rápida é de 10 dias, e o período da média lenta é de 50 dias. Quando a média rápida cruza acima da média lenta, gera-se um sinal de compra; quando a média rápida cruza abaixo da média lenta, gera-se um sinal de venda. Este sistema de médias móveis duplas pode identificar efetivamente as reversões de tendência de médio e longo prazo no mercado.

Com base nas médias móveis duplas, a estratégia também introduz o indicador RSI para confirmar os sinais de tendência e evitar falsos rompimentos. O RSI mede a força do mercado pela diferença entre as médias rápida e lenta, com um comprimento de 14. Quando o RSI cruza acima de 30, gera-se um sinal de compra; quando cruza abaixo de 70, gera-se um sinal de venda.

Além disso, a estratégia utiliza o indicador ATR para ajustar automaticamente o nível de stop loss. O ATR pode refletir efetivamente o grau de volatilidade do mercado. Quando a volatilidade do mercado aumenta, a estratégia define o stop loss de forma mais ampla, reduzindo a possibilidade de ser estopado.

Por fim, a estratégia usa o indicador ADX para avaliar a força da tendência. O ADX mede a força da tendência pela diferença entre o indicador direcional positivo (DI+) e o indicador direcional negativo (DI-). Quando o valor do ADX cruza acima de 20, considera-se que a tendência está estabelecida, e então são gerados os sinais reais de negociação.

Através da combinação de múltiplos indicadores, a estratégia pode ser mais cautelosa ao emitir sinais de negociação, evitando ser enganada por falsos sinais no mercado, obtendo assim uma taxa de acerto mais alta.

Vantagens da Estratégia

Esta estratégia possui as seguintes vantagens:

-

Combinação de múltiplos indicadores, avaliação abrangente do mercado, melhorando a precisão das decisões

Ao combinar vários indicadores como médias móveis, RSI, ATR, ADX, etc., é possível melhorar a precisão das decisões de negociação, evitando julgamentos errôneos causados por um único indicador.

-

Ajuste automático do stop loss, controlando o risco

Ajustar automaticamente o nível de stop loss de acordo com a volatilidade do mercado pode reduzir a probabilidade de o stop loss ser acionado, controlando efetivamente o risco da negociação.

-

Avaliação da força da tendência, reduzindo operações contrárias

Ao avaliar a força da tendência com o ADX antes de realmente negociar, é possível reduzir as perdas causadas por operações contrárias.

-

Grande espaço para otimização de parâmetros

Parâmetros como o comprimento das médias móveis, o período do RSI, o ciclo do ATR, o ciclo do ADX, etc., podem ser ajustados e otimizados de acordo com diferentes mercados, oferecendo forte adaptabilidade.

-

Proteção dos lucros de longo prazo

Através do sistema de médias móveis rápidas e lentas para avaliar a tendência de longo prazo, combinado com indicadores como RSI para reduzir a influência do ruído de curto prazo, é possível manter posições de longo prazo durante a tendência, obtendo maiores retornos.

Riscos e Contramedidas

Esta estratégia também apresenta alguns riscos, sendo os principais:

-

Risco de otimização de parâmetros

A combinação de múltiplos parâmetros aumenta a dificuldade de otimização, e uma combinação inadequada de parâmetros pode levar a um desempenho inferior da estratégia. Este risco pode ser mitigado com backtesting mais completo e ajuste de parâmetros.

-

Risco de falha dos indicadores

Todos os indicadores técnicos têm condições de mercado em que são mais adequados. Quando o mercado entra em um estado especial, os indicadores envolvidos na estratégia podem falhar simultaneamente. É necessário estar atento ao risco trazido por eventos do tipo Cisne Negro.

-

Risco de perda em posições vendidas

A estratégia permite negociações a descoberto (vendas). As vendas a descoberto envolvem inerentemente o risco de perdas ilimitadas. Este risco pode ser reduzido através da definição de stop loss.

-

Risco de reversão

Em uma reversão de tendência, os sinais dos indicadores podem não reagir rapidamente, o que pode facilmente levar a perdas na direção oposta. Pode-se encurtar adequadamente alguns parâmetros dos indicadores para aumentar a sensibilidade.

Ideias de Otimização

Esta estratégia ainda possui espaço para otimização adicional, sendo as principais ideias:

-

Aumentar pesos adaptativos dos indicadores

Ao analisar a correlação entre diferentes indicadores e as condições do mercado, pode-se projetar um mecanismo para ajustar dinamicamente os pesos de cada indicador, melhorando a eficácia das decisões em diferentes ambientes de mercado.

-

Adicionar suporte de modelos de aprendizado profundo

Usar modelos como aprendizado profundo para prever a direção das mudanças de preço, auxiliando as regras de decisão projetadas manualmente, melhorando a precisão das decisões da estratégia.

-

Otimizar a adaptação automática de parâmetros

Projetar um módulo de otimização automática de parâmetros com base em dados históricos de janela deslizante, permitindo o ajuste dinâmico dos parâmetros dos indicadores, tornando a estratégia mais adaptável às mudanças do mercado.

-

Introduzir análise de ciclo variável

Adicionar métodos de análise de ciclo variável, como a Teoria das Ondas, para auxiliar na avaliação das tendências de médio e longo prazo, aumentando a probabilidade de lucro nas posições.

Resumo

Esta estratégia integra o uso de múltiplos indicadores como Médias Móveis, RSI, ATR e ADX para projetar um conjunto relativamente completo de regras de decisão. Ela pode tanto avaliar tendências de longo prazo através do sistema de médias móveis, quanto reduzir a interferência de ruídos de curto prazo através de indicadores de ciclo curto como o RSI. Ao mesmo tempo, a estratégia possui um grande espaço para otimização, podendo obter um desempenho ainda melhor. No geral, esta estratégia melhora a eficácia das decisões ao combinar indicadores, controla o risco e merece estudo e aplicação adicionais.

- 1