Estratégia de Negociação de Duas Médias Móveis em Timeframes Cruzados

Visão Geral

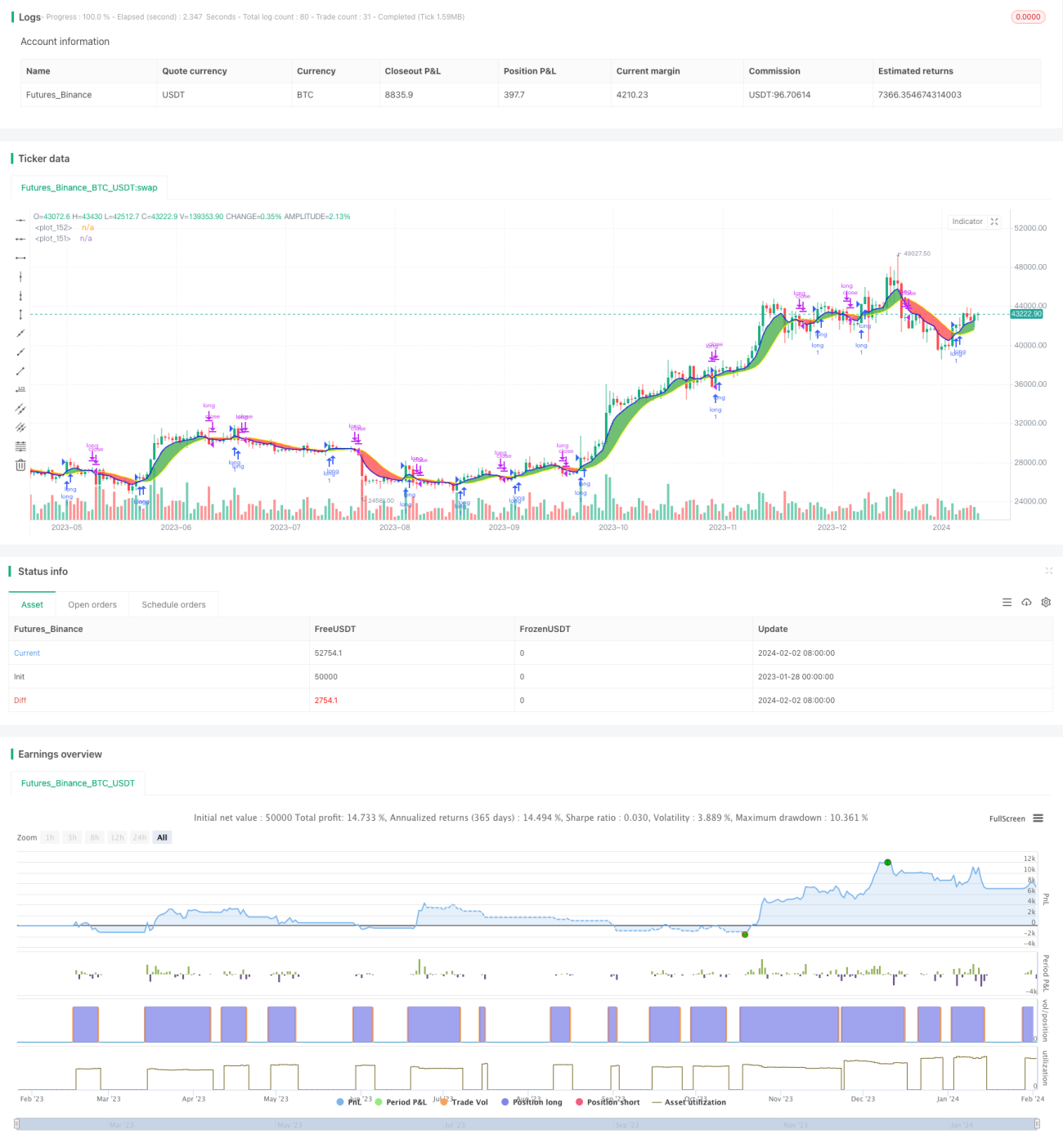

Esta estratégia calcula dois tipos diferentes de médias móveis, gerando sinais de compra e venda em dois períodos de tempo distintos. É uma excelente estratégia sandbox para experimentar diferentes tipos de médias móveis e combinações de prazos.

Princípio da Estratégia

A estratégia utiliza duas médias móveis: uma rápida e uma lenta. O período de tempo da média rápida deve ser maior ou igual ao período do gráfico. Quando a média móvel rápida cruza para cima da média lenta, gera um sinal de compra; quando cruza para baixo, gera um sinal de venda.

O usuário pode escolher vários tipos diferentes de médias móveis, como SMA, EMA, KAMA, etc. Os períodos de tempo podem ser diferentes, permitindo experimentar combinações para encontrar os parâmetros ideais.

Análise de Vantagens

A maior vantagem desta estratégia é a facilidade de ajustar os parâmetros para experimentar diferentes combinações e encontrar a configuração ideal.

O usuário pode selecionar livremente o tipo, o comprimento e o período de tempo das duas médias móveis, e o sistema calcula e exibe os resultados em tempo real. Isso é muito mais fácil do que testar combinações de parâmetros uma por uma.

Além disso, a estratégia possui funções embutidas de stop loss e take profit, que podem reduzir riscos e aumentar a probabilidade de lucro.

Análise de Riscos

O maior risco desta estratégia é que uma configuração inadequada de parâmetros pode levar a sinais de negociação excessivamente frequentes, aumentando os custos de transação e as perdas por slippage.

Além disso, as médias móveis duplas são propensas a gerar sinais falsos; se os parâmetros não forem bem escolhidos, os sinais de compra e venda podem não ser confiáveis.

Esses riscos podem ser mitigados otimizando os parâmetros ou combinando outros indicadores.

Direções de Otimização

Pode-se considerar adicionar outros indicadores ao sistema de médias móveis duplas para filtrar sinais, como o RSI para confirmar sinais de compra e venda, reduzindo assim sinais falsos.

Outra possibilidade é treinar e otimizar os parâmetros das médias móveis para encontrar a melhor combinação. Também se pode considerar o uso de aprendizado de máquina para otimizar dinamicamente os parâmetros.

Resumo

Esta estratégia é uma excelente sandbox para experimentar médias móveis duplas. Sua vantagem está na capacidade de iterar rapidamente diferentes combinações de parâmetros para encontrar a melhor estratégia de negociação. É claro que existem riscos de configuração inadequada de parâmetros, que podem ser reduzidos adicionando outros indicadores para filtrar. Se continuar otimizando essa estratégia, é provável que se obtenham melhores resultados de negociação.

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.- 1