Estratégia de Trading de Reversão com Bandas de Bollinger + RSI + ADX + ATR

Visão Geral

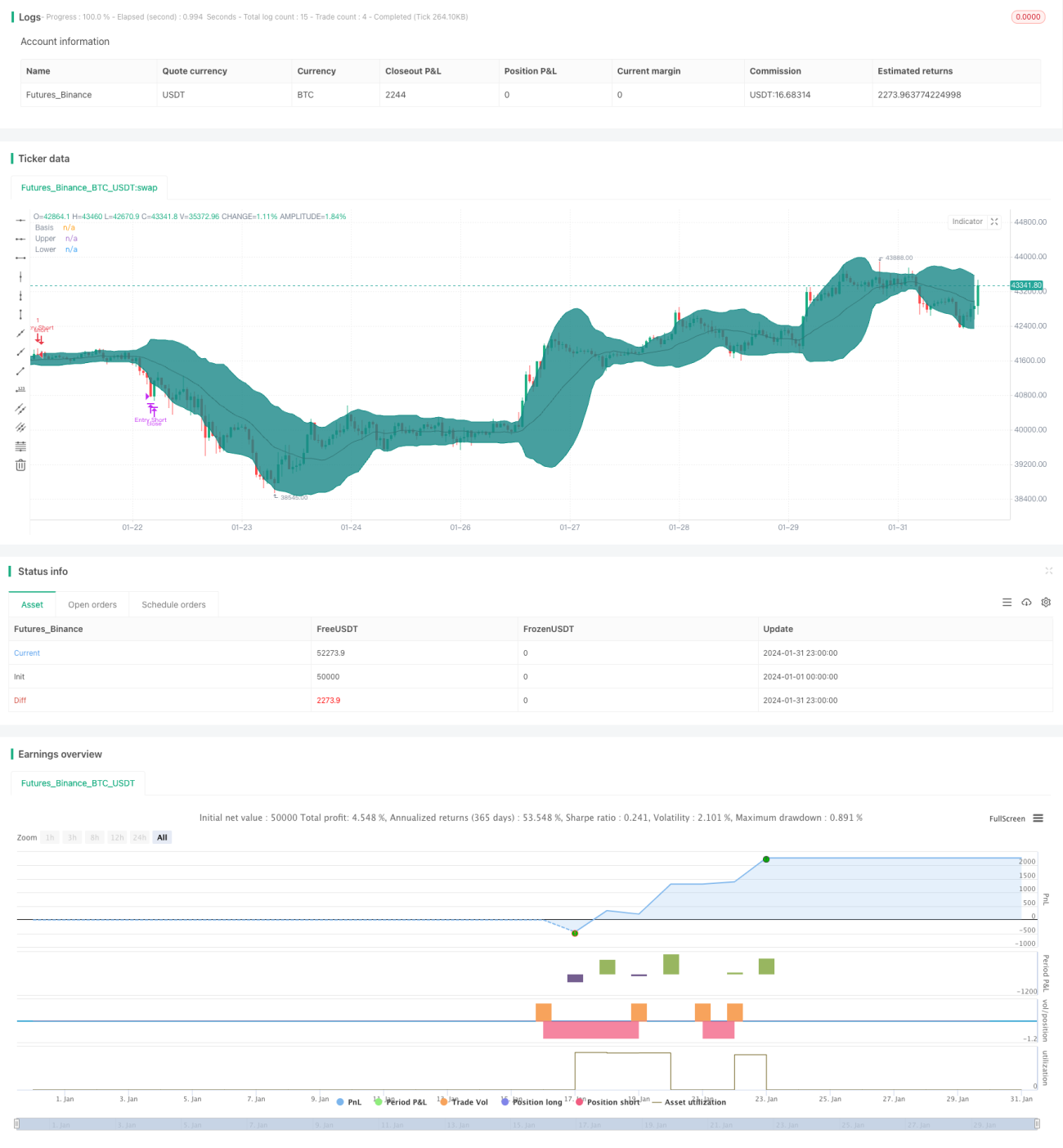

Esta estratégia combina múltiplos indicadores técnicos. Quando as Bandas de Bollinger emitem um sinal de reversão de preço, ela utiliza os indicadores RSI, ADX e ATR para avaliar a estrutura do mercado, buscando oportunidades de negociação de reversão com alta probabilidade.

Princípios da Estratégia

-

Utiliza Bandas de Bollinger de 20 períodos. Quando o preço atinge as bandas superior ou inferior, aguarda-se a formação de um candle de reversão para gerar sinais de compra ou venda.

-

O RSI avalia se o mercado está em uma faixa de oscilação. RSI acima de 60 indica zona de alta, abaixo de 40 indica zona de baixa.

-

ADX abaixo de 20 indica mercado lateral/em oscilação; acima de 20 indica mercado em tendência.

-

O ATR é usado para definição de stop loss e stop loss móvel (trailing stop).

-

Utiliza médias móveis EMA como filtro adicional de sinais.

Análise das Vantagens da Estratégia

-

Integração de múltiplos indicadores, gerando sinais de negociação de alta probabilidade.

-

Parâmetros configuráveis, adaptando-se a diferentes ambientes de mercado.

-

Regras rigorosas de stop loss, controlando efetivamente o risco.

Análise dos Riscos da Estratégia

-

Ajustes inadequados de parâmetros podem levar a negociações excessivamente frequentes.

-

Ainda existe a probabilidade de falha na reversão.

-

O stop loss móvel pode falhar em determinados mercados.

Direções de Otimização da Estratégia

-

Testar combinações de mais indicadores para encontrar configurações de parâmetros mais adequadas.

-

Identificar rapidamente oportunidades de continuação de reversão após uma quebra falha.

-

Testar diferentes métodos de stop loss para torná-lo mais inteligente.

Resumo

Esta estratégia utiliza as Bandas de Bollinger como sinal base de negociação, enquanto múltiplos indicadores auxiliares formam um sistema de filtragem de alta probabilidade, com regras de stop loss relativamente completas. O desempenho da estratégia ainda pode ser aprimorado por meio do ajuste de parâmetros e da otimização dos indicadores. No geral, a estratégia estabelece um sistema confiável de negociação de reversão.

- 1