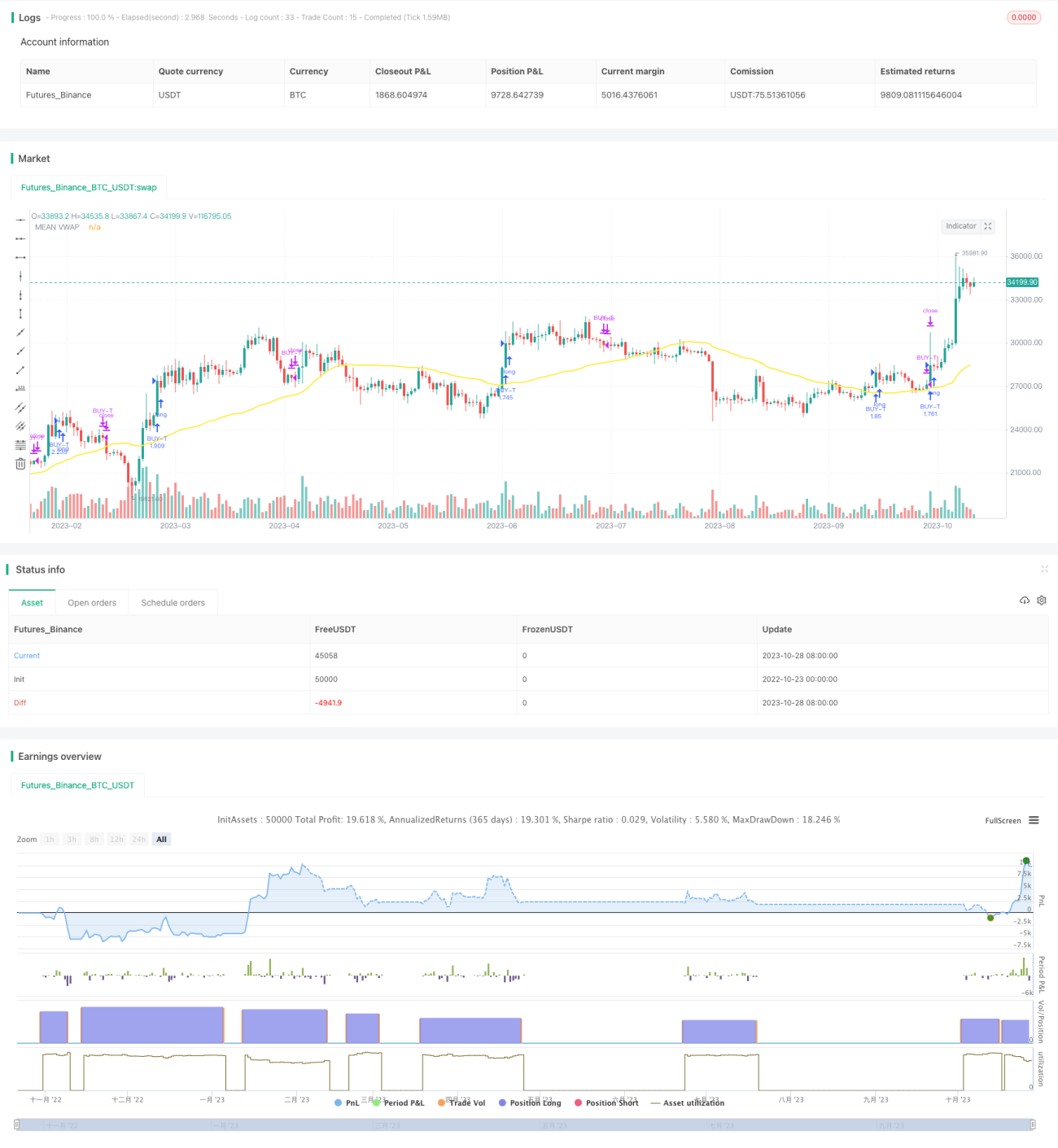

Алгоритмическая торговая стратегия с двойным отслеживанием

Обзор

Данная стратегия в основном использует принцип пересечения скользящих средних в сочетании с сигналами разворота индикатора RSI и пользовательским алгоритмом двойной линии для отслеживания пересечения скользящих средних. Стратегия отслеживает пересечение двух скользящих средних с разными периодами: быстрая скользящая средняя отслеживает краткосрочный тренд, а медленная – долгосрочный. Когда быстрая скользящая средняя пересекает медленную снизу вверх, это указывает на восходящий краткосрочный тренд – можно покупать. Когда быстрая скользящая средняя пересекает медленную сверху вниз, краткосрочный тренд завершается – следует закрывать позицию.

Принцип стратегии

-

Рассчитываются две группы VWAP-скользящих средних с разными параметрами, представляющие долгосрочный и краткосрочный тренды.

- Медленная линия Тяньму и базовая линия рассчитывают долгосрочный тренд.

- Быстрая линия Тяньму и базовая линия рассчитывают краткосрочный тренд.

-

Берутся средние значения линий Тяньму и базовых линий каждой группы как медленная и быстрая скользящие средние.

-

Рассчитывается индикатор полос Боллинджера для определения консолидации и пробоя.

- Средняя линия – это среднее значение быстрой и медленной скользящих средних.

- Верхняя и нижняя полосы Боллинджера используются для определения пробоя.

-

Рассчитывается индикатор TSV для оценки объема сделок.

- TSV > 0 означает, что восходящая сила превышает нисходящую.

- TSV > своей EMA означает усиление силы.

-

Рассчитывается индикатор RSI для определения зон перекупленности/перепроданности.

- RSI < 30 – зона перепроданности, можно покупать.

- RSI > 70 – зона перекупленности, следует продавать.

-

Условия входа:

- Быстрая скользящая средняя пересекает медленную снизу вверх.

- Цена закрытия пересекает верхнюю полосу Боллинджера снизу вверх.

- TSV > 0 и TSV > своей EMA.

- RSI < 30.

-

Условия выхода:

- Быстрая скользящая средняя пересекает медленную сверху вниз.

- RSI > 70.

Анализ преимуществ

-

Использование системы двойных скользящих средних позволяет одновременно улавливать краткосрочные и долгосрочные тренды.

-

Индикатор RSI предотвращает покупку в зоне перекупленности и продажу в зоне перепроданности.

-

Индикатор TSV гарантирует достаточный объем сделок для поддержки тренда.

-

Полосы Боллинджера помогают определить ключевые точки пробоя.

-

Комбинация нескольких индикаторов позволяет эффективно отфильтровывать ложные пробои.

Анализ рисков

-

Система скользящих средних склонна давать ложные сигналы, требуется фильтрация вспомогательными индикаторами.

-

Параметры индикатора RSI нуждаются в оптимизации, иначе могут быть пропущены точки входа/выхода.

-

Индикатор TSV также чувствителен к параметрам, требует тщательного тестирования.

-

Пробой верхней полосы Боллинджера может оказаться ложным пробоем, требует подтверждения.

-

Комбинация нескольких индикаторов усложняет оптимизацию параметров и повышает риск переоптимизации.

-

Недостаточность обучающих и тестовых данных может привести к подгонке кривой.

Направления оптимизации

-

Протестировать больше периодов для поиска оптимальной комбинации параметров.

-

Попробовать заменить или дополнить RSI другими индикаторами, такими как MACD, KD.

-

При оптимизации параметров обязательно использовать анализ walk forward.

-

Добавить стратегию стоп-лосса для контроля убытков по каждой сделке.

-

Рассмотреть возможность включения моделей машинного обучения для вспомогательной оценки сигналов.

-

Адаптировать параметры для разных рынков, не полагаться чрезмерно на одну комбинацию.

Заключение

Данная стратегия с помощью системы двойных скользящих средних улавливает долгосрочные и краткосрочные тренды, одновременно фильтруя сигналы с помощью RSI, TSV, полос Боллинджера и других индикаторов. Преимущество стратегии – следование тенденции и захват долгосрочных восходящих волн. Однако существует определенный риск ложных сигналов, требуется дальнейшая оптимизация параметров и контроль стоп-лоссов для снижения рисков. В целом стратегия, сочетающая трендовые и разворотные индикаторы, показывает хорошие результаты на долгосрочных растущих рынках, но требует корректировки параметров для разных рынков.

- 1