Стратегия следования за трендом на основе пробоя скользящей средней

Обзор

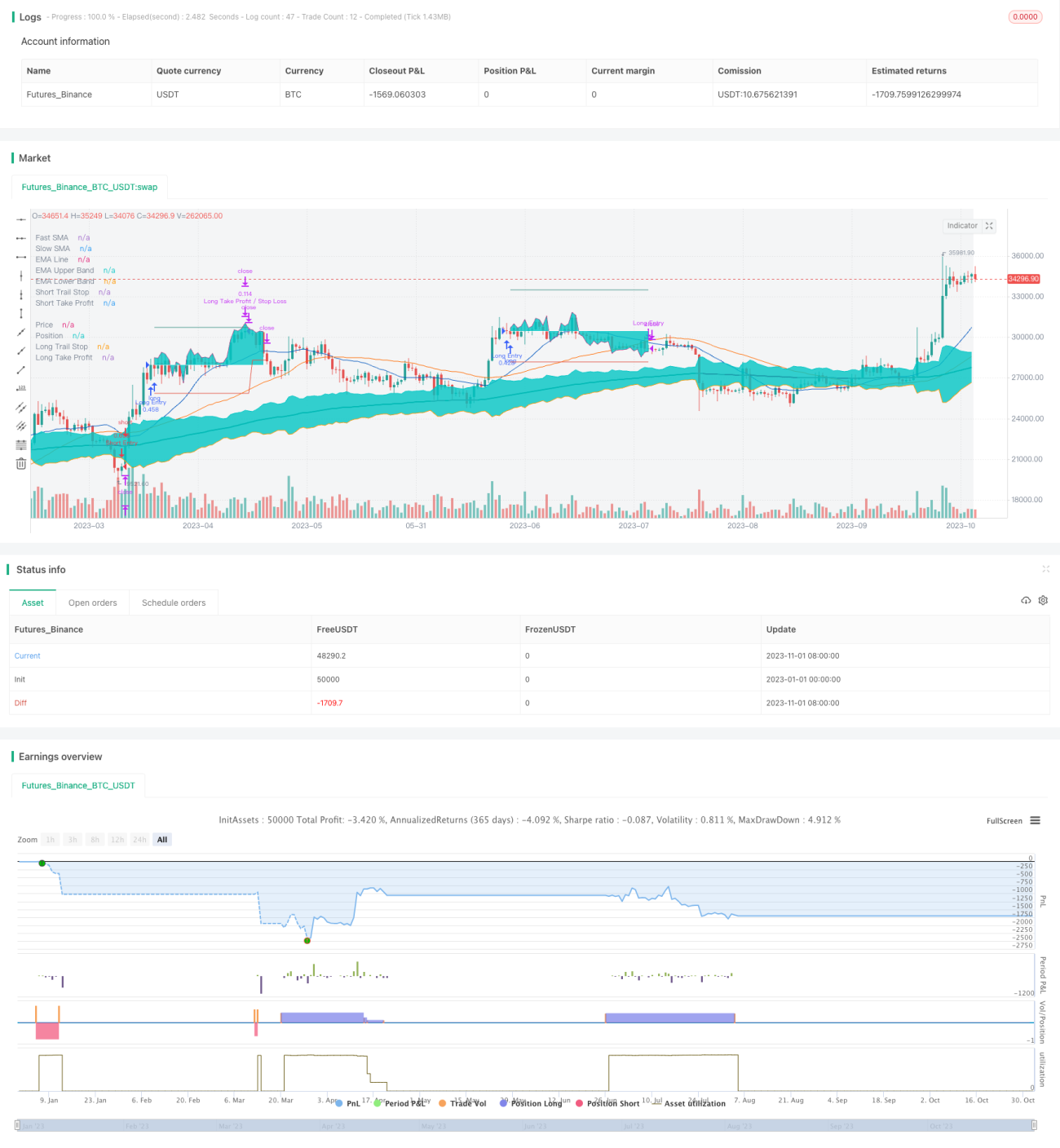

Данная стратегия использует пересечение простых скользящих средних (SMA) для определения направления тренда. В начале тренда она открывает полную позицию в длинную или короткую сторону и устанавливает стоп-лосс и тейк-профит для контроля риска. После входа в позицию стратегия непрерывно отслеживает тренд с помощью скользящих средних и закрывает позицию при расхождении с трендом. Стратегия также включает настраиваемые модули управления стоп-лоссом, тейк-профитом и размером позиции, что позволяет гибко настраивать параметры для различных инструментов.

Принцип стратегии

Стратегия в основном использует пересечение быстрой и медленной простых скользящих средних для определения начала и окончания тренда. Сначала стратегия сравнивает быструю SMA (например, 21-дневную) и медленную SMA (например, 49-дневную). Когда быстрая линия пересекает медленную снизу вверх, считается, что рынок входит в восходящий тренд, и в этот момент открывается длинная позиция. Когда быстрая линия пересекает медленную сверху вниз, считается, что рынок входит в нисходящий тренд, и в этот момент открывается короткая позиция.

После входа в позицию стратегия в реальном времени отслеживает отношение цены к SMA. Когда цена пробивает SMA сверху вниз, считается, что восходящий тренд завершён, и длинная позиция закрывается. Когда цена пробивает SMA снизу вверх, считается, что нисходящий тренд завершён, и короткая позиция закрывается.

Для контроля риска при открытии позиции одновременно устанавливаются стоп-лосс и тейк-профит. Расстояние до стоп-лосса задаётся на основе ATR, а расстояние до тейк-профита может быть задано либо в процентах, либо на основе ATR. После открытия позиции стоп-лосс отслеживает цену в реальном времени, обеспечивая скользящий стоп. При достижении тейк-профита часть позиции закрывается, а оставшаяся часть продолжает следовать за трендом до полного выхода.

Стратегия также включает модуль управления размером позиции, который позволяет ограничивать использование капитала на одну сделку, тем самым контролируя риск отдельной сделки. Кроме того, настройка максимальной просадки позволяет контролировать общий риск стратегии.

Преимущества стратегии

- Определение направления тренда на основе сравнения скользящих средних — принцип прост и понятен.

- После входа в позицию используется скользящий стоп-лосс, что позволяет зафиксировать большую часть прибыли.

- Настраиваемые способы стоп-лосса и тейк-профита позволяют адаптировать стратегию под различные инструменты.

- Риск по отдельной сделке контролируется — полная загрузка капитала не происходит.

- Настройка максимальной просадки позволяет ограничить общие убытки стратегии.

Риски и решения

- Пересечение двух скользящих средних имеет некоторую задержку, что может привести к пропуску оптимальной точки входа в начале тренда.

- Требуется многократная настройка параметров для тестирования различных комбинаций периодов скользящих средних.

- Пересечение скользящих средних имеет определённый уровень ложных сигналов — точность входа не достигает 100%.

- Скользящий стоп-лосс может быть пробит, что не позволяет зафиксировать всю прибыль.

- Необходимо устанавливать достаточно широкое расстояние до стоп-лосса, чтобы дать цене пространство для отката.

- Ограничение максимальной просадки может быть слишком консервативным, что приводит к потере возможностей роста.

- Можно немного увеличить допустимую максимальную просадку, чтобы дать стратегии больше пространства для погрешностей.

Направления оптимизации

- Испытать различные комбинации параметров для выбора оптимальных периодов скользящих средних.

- Добавить индикаторы силы тренда для повышения точности входа.

- Оптимизировать стратегию стоп-лосса для более эффективного следования за трендом.

- Протестировать различные стратегии тейк-профита для выбора оптимальной точки фиксации прибыли.

- Оптимизировать схему управления размером позиции для повышения эффективности использования капитала.

- Скорректировать настройку максимальной просадки для баланса между доходностью и риском.

Заключение

В целом, данная стратегия является отличной вводной стратегией для новичков: её принцип прост и легко понимается. В то же время она обладает достаточными возможностями контроля риска, что снижает вероятность крупных убытков. Путём оптимизации параметров можно добиться неплохих результатов. Однако её внутренние недостатки не позволяют ей достичь высокой точности операций. Рекомендуется использовать эту стратегию как тренировочную для новичков, но она не подходит трейдерам, стремящимся к высокой эффективности и высокой доле выигрышных сделок. Для достижения лучших результатов торговли необходимо искать стратегии с более сильной прогностической способностью.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1