Стратегия супер-тренда Ишимоку

Обзор

Стратегия «Ичимоку Супер» — это трендовая стратегия, основанная на торговых решениях по индикатору Ичимоку. Она использует взаимосвязь линии поворота, базовой линии и облака Ичимоку для определения текущего направления тренда, а также ценовые откаты для входа в рынок.

Стратегия «Ичимоку Супер» в основном подходит для среднесрочной и долгосрочной трендовой торговли, позволяя получать прибыль на крупных трендах. Она также обладает высокой способностью распознавать тренды.

Принцип стратегии

Стратегия «Ичимоку Супер» определяет направление торговли на основе следующих ключевых элементов:

- Взаимосвязь линии поворота и базовой линии: Если линия поворота выше — бычий сигнал, если ниже — медвежий.

- Цвет облака: Если облако зеленое — бычий сигнал, если красное — медвежий.

- Ценовой откат: Для входа необходимо, чтобы цена вернулась за пределы линии поворота и базовой линии.

Конкретно торговые сигналы стратегии:

Сигнал на покупку (Long):

- Линия поворота выше базовой линии

- Цена выше линии поворота и базовой линии

- Линия поворота и базовая линия выше облака

- Цена откатывается ниже линии поворота и базовой линии

Сигнал на продажу (Short):

- Линия поворота ниже базовой линии

- Цена ниже линии поворота и базовой линии

- Линия поворота и базовая линия ниже облака

- Цена откатывается выше линии поворота и базовой линии

При одновременном выполнении условий для покупки/продажи открывается позиция в соответствии с текущим положением.

Анализ преимуществ

Стратегия «Ичимоку Супер» имеет следующие преимущества:

- Комбинация индикаторов Ичимоку для определения направления тренда обеспечивает высокую точность.

- Линия поворота и базовая линия четко определяют кратко- и среднесрочный тренд, а облако — долгосрочный.

- Условие отката цены к линии поворота позволяет избежать убытков от ложных пробоев.

- Управление рисками осуществляется с помощью стоп-лосса на основе недавних максимумов и минимумов, что эффективно ограничивает убытки по одной сделке.

- Разумное соотношение прибыли и убытков, нацеленное на стабильный доход.

- Возможность применения на разных таймфреймах, подходит для среднесрочной и долгосрочной трендовой торговли.

- Логика стратегии ясна и проста для понимания, большой потенциал для оптимизации параметров.

- Хорошие результаты на различных рыночных условиях.

Анализ рисков

Стратегия «Ичимоку Супер» также имеет следующие риски:

- На боковом рынке стоп-лосс может срабатывать слишком часто, снижая прибыльность.

- При резкой смене тренда стратегия может не успеть развернуть позицию, что приведет к убыткам.

- Установленное соотношение прибыли и убытка подходит не для всех инструментов, требуется настройка параметров под конкретные активы.

- Если после пробоя облака потенциал роста ограничен, прибыль может быть небольшой.

- Параметры индикаторов требуют многократного тестирования и оптимизации, стратегия не подходит для инструментов с частой сменой параметров.

Снизить риски можно следующими способами:

- Оптимизация параметров для лучшего соответствия различным таймфреймам и инструментам.

- Фильтрация сигналов с помощью других индикаторов для избежания ложных пробоев на боковом рынке.

- Динамическая корректировка уровня стоп-лосса для уменьшения вероятности его срабатывания.

- Тестирование различных настроек соотношения прибыли и убытка.

- Использование графических паттернов и других методов для определения силы трендового сигнала.

Направления оптимизации

Стратегию «Ичимоку Супер» можно оптимизировать по следующим направлениям:

- Оптимизация параметров линии поворота и базовой линии для лучшего соответствия характеристикам торгуемого инструмента.

- Оптимизация параметров облака, чтобы оно точнее определяло долгосрочный тренд.

- Улучшение алгоритма стоп-лосса, например, использование ATR или динамического стоп-лосса.

- Добавление фильтрации сигналов с помощью других индикаторов и дополнительных условий для снижения вероятности ложных входов.

- Оптимизация настройки соотношения прибыли и убытка для адаптации к различным инструментам и таймфреймам.

- Использование мартингейла для управления позициями с учетом частоты колебаний рынка.

- Применение методов машинного обучения для оптимизации параметров с целью повышения стабильности.

- Настройка различных торговых сессий для учета особенностей ночной и дневной торговли.

Заключение

Стратегия «Ичимоку Супер» в целом очень хорошо подходит для среднесрочной и долгосрочной трендовой торговли. Она использует индикатор Ичимоку для определения направления тренда, что является явным преимуществом, а вход с учетом ценовых откатов позволяет эффективно избегать ложных входов. Оптимизация параметров позволяет добиться стабильной прибыльности на большем количестве инструментов и таймфреймов. Эта стратегия проста для понимания и имеет большой потенциал для оптимизации, что делает ее подходящей в качестве базовой стратегии для исследования и обучения.

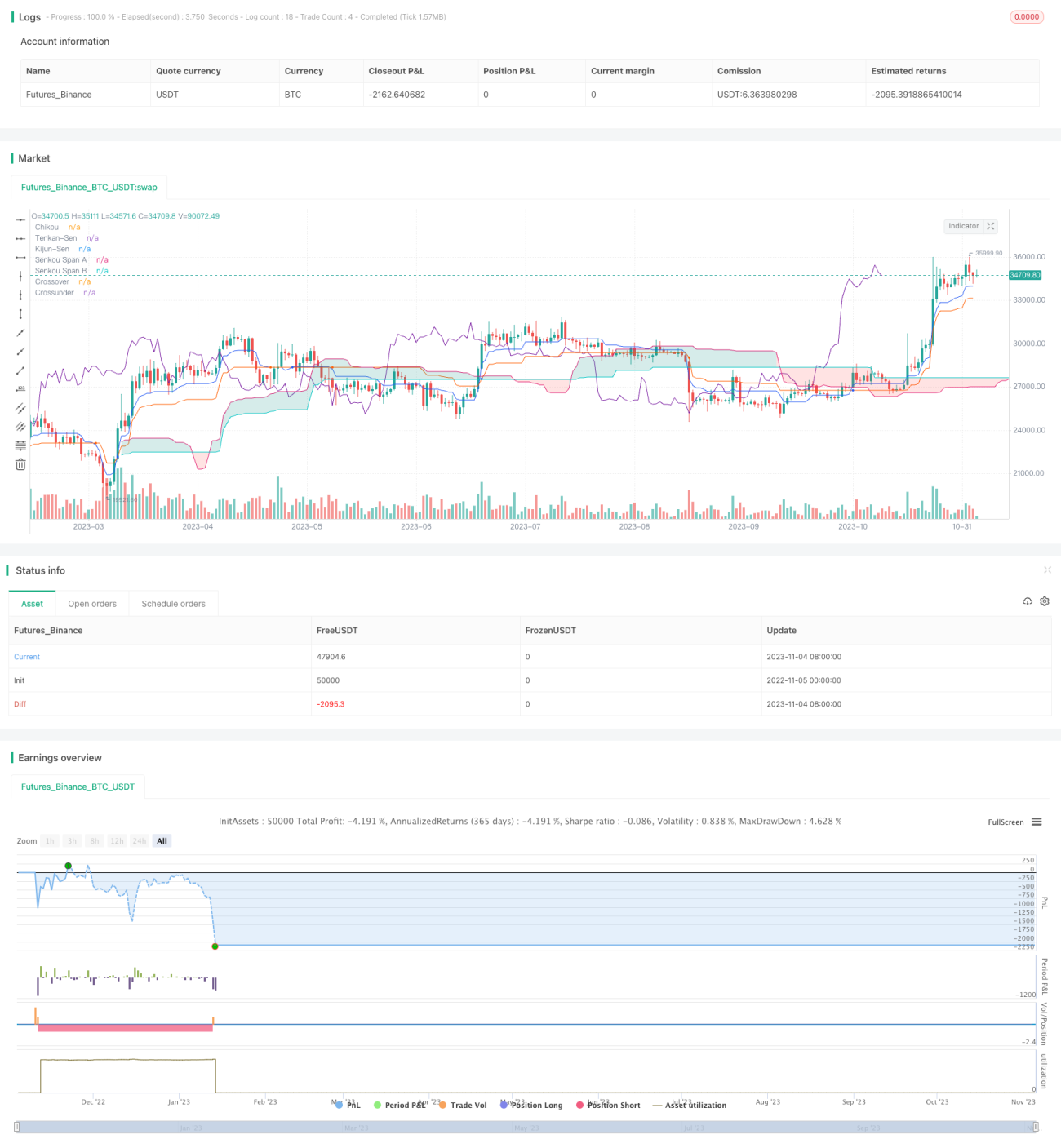

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1