Количественная торговая стратегия на основе динамических скользящих средних по нескольким инструментам

Обзор

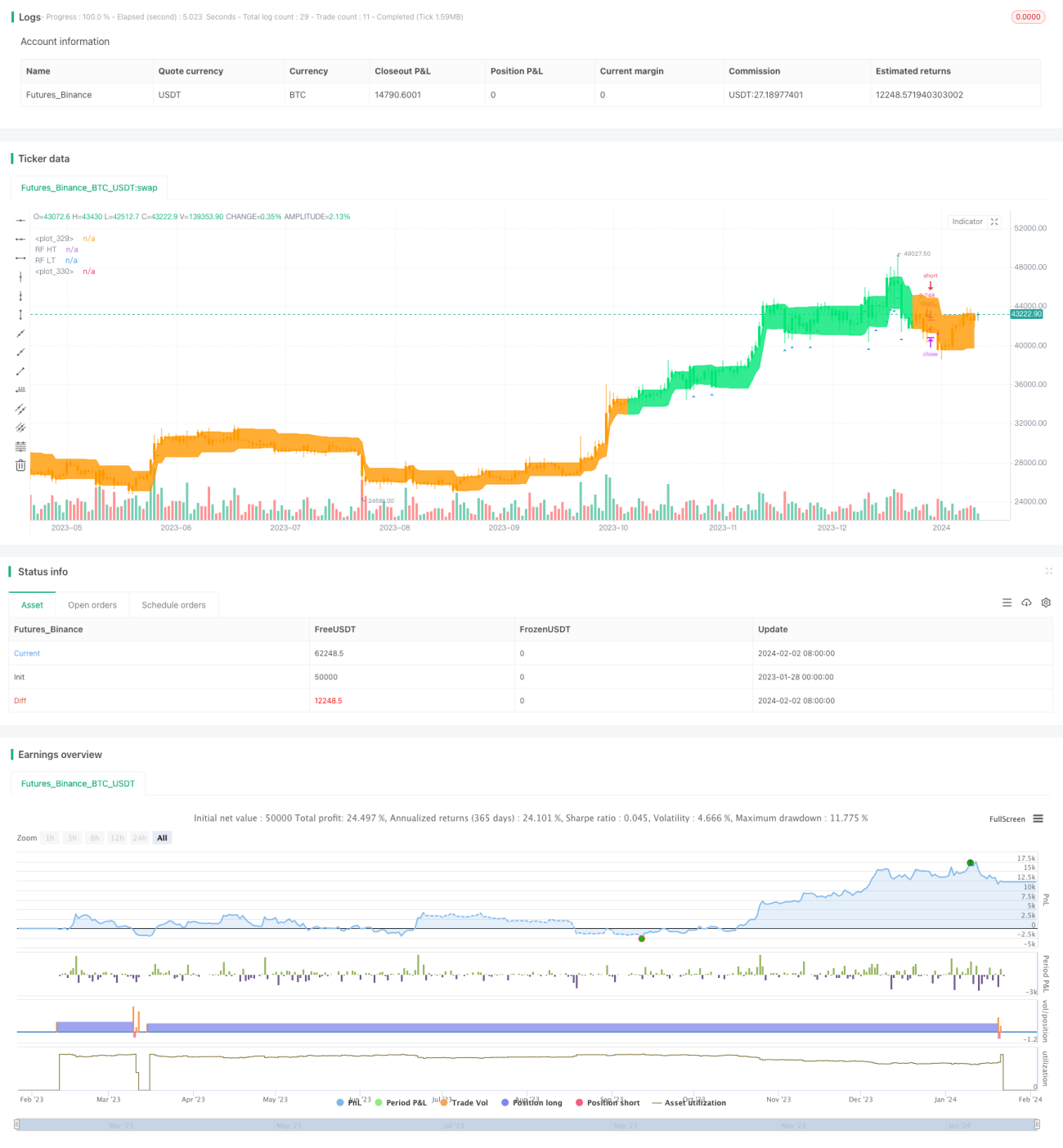

Данная стратегия использует комбинированные сигналы нескольких технических индикаторов для динамической торговли такими активами, как акции и криптовалюты. Стратегия автоматически определяет рыночные тренды и осуществляет следование за трендом. Кроме того, в стратегию добавлен механизм стоп-лосса для контроля рисков.

Принцип стратегии

Стратегия в основном использует несколько индикаторов, таких как скользящие средние, индекс относительной силы (RSI), средний истинный диапазон (ATR) и индекс направленного движения (ADX), для генерации торговых сигналов на основе их комбинации.

В частности, стратегия сначала использует двойные скользящие средние для формирования сигналов «золотого креста» и «смертельного креста». Длина быстрой линии составляет 10 дней, медленной – 50 дней. Когда быстрая линия пересекает медленную снизу вверх, генерируется сигнал на покупку; когда быстрая линия пересекает медленную сверху вниз, генерируется сигнал на продажу. Эта система двойных скользящих средних эффективно выявляет развороты среднесрочных и долгосрочных трендов.

Поверх двойных скользящих средних стратегия также использует индикатор RSI для подтверждения трендовых сигналов и избежания ложных пробоев. RSI оценивает силу рынка по разнице между быстрой и медленной линиями, период Length равен 14. Когда RSI пересекает 30 снизу вверх, формируется сигнал на покупку; когда пересекает 70 сверху вниз – сигнал на продажу.

Кроме того, стратегия использует индикатор ATR для автоматической корректировки уровня стоп-лосса. ATR эффективно отражает волатильность рынка. При увеличении волатильности стратегия устанавливает более широкий стоп-лосс, уменьшая вероятность его срабатывания.

Наконец, стратегия применяет индикатор ADX для оценки силы тренда. ADX определяет силу тренда на основе разницы между положительным индикатором направленности DI+ и отрицательным DI-. Когда значение ADX пересекает 20 снизу вверх, считается, что тренд установлен, и только тогда формируется фактический торговый сигнал.

Комбинация нескольких индикаторов делает стратегию более осторожной при подаче торговых сигналов, помогая избежать обмана ложными сигналами на рынке и тем самым повышая процент выигрышных сделок.

Преимущества стратегии

Данная стратегия обладает следующими преимуществами:

-

Комбинация нескольких индикаторов для всесторонней оценки рынка и повышения точности решений

Использование комбинации таких индикаторов, как скользящие средние, RSI, ATR, ADX, позволяет повысить точность торговых решений и избежать ошибок, связанных с использованием только одного индикатора. -

Автоматическая корректировка стоп-лосса для контроля риска

Автоматическая регулировка уровня стоп-лосса в зависимости от волатильности рынка снижает вероятность его срабатывания и эффективно контролирует торговые риски. -

Оценка силы тренда для уменьшения контртрендовых операций

Использование индикатора ADX для оценки силы тренда перед фактической торговлей позволяет уменьшить убытки от контртрендовых операций. -

Большое пространство для оптимизации параметров

Параметры стратегии, такие как длины скользящих средних, период RSI, период ATR, период ADX, могут быть оптимизированы под разные рынки, что обеспечивает высокую адаптивность. -

Защита долгосрочной прибыли

Система быстрых и медленных скользящих средних позволяет определить долгосрочный тренд, а комбинация с такими индикаторами, как RSI, снижает влияние краткосрочного шума, что позволяет удерживать позиции вдоль тренда и получать более высокую доходность.

Риски и меры противодействия

Данная стратегия также имеет некоторые риски, основные из них включают:

-

Риск оптимизации параметров

Комбинация множества параметров увеличивает сложность оптимизации; неподходящий набор параметров может ухудшить результаты стратегии. Этот риск можно снизить за счет более тщательного бэктестинга и корректировки параметров. -

Риск отказа индикаторов

Технические индикаторы эффективны лишь в определенных рыночных состояниях. При переходе рынка в особое состояние используемые индикаторы могут одновременно перестать работать. Необходимо учитывать риск событий «черного лебедя». -

Риск убытков по коротким позициям

Стратегия допускает короткие продажи. Короткие позиции сами по себе несут риск неограниченных убытков. Этот риск можно снизить установкой стоп-лосса. -

Риск разворота тренда

При развороте тренда индикаторы могут не успеть среагировать, что может привести к убыткам от движения против позиции. Этот риск можно уменьшить, сократив периоды некоторых индикаторов для повышения чувствительности.

Направления оптимизации

Данная стратегия имеет потенциал для дальнейшей оптимизации, основные направления включают:

-

Добавление адаптивных весов индикаторов

Путем анализа корреляции между различными индикаторами и рыночными состояниями можно разработать механизм динамической корректировки весов индикаторов для повышения эффективности решений в различных рыночных условиях. -

Интеграция моделей глубокого обучения

Использование моделей глубокого обучения для прогнозирования направления изменения цены может дополнить вручную разработанные правила принятия решений и повысить точность стратегии. -

Оптимизация адаптации параметров

Разработка автоматического модуля оптимизации параметров на основе исторических данных в скользящем окне для динамической настройки параметров индикаторов, что позволит стратегии лучше адаптироваться к рыночным изменениям. -

Введение анализа с переменной длиной цикла

Включение методов анализа с переменной длиной цикла, таких как теория волн, для помощи в определении среднесрочных и долгосрочных трендов и повышения вероятности получения прибыли от удержания позиций.

Заключение

Данная стратегия комплексно использует несколько индикаторов, включая скользящие средние, RSI, ATR, ADX, и формирует достаточно полный набор правил принятия решений. Она позволяет как определять долгосрочные тренды с помощью системы скользящих средних, так и снижать влияние шума с помощью краткосрочных индикаторов, таких как RSI. Кроме того, стратегия обладает большим пространством для оптимизации, что дает возможность добиться лучших результатов. В целом, стратегия повышает эффективность решений за счет комбинации индикаторов и контролирует риски, что делает ее достойной дальнейшего изучения и применения.

- 1