Полосы Боллинджера + RSI + ADX + ATR: стратегия разворотной торговли

Обзор

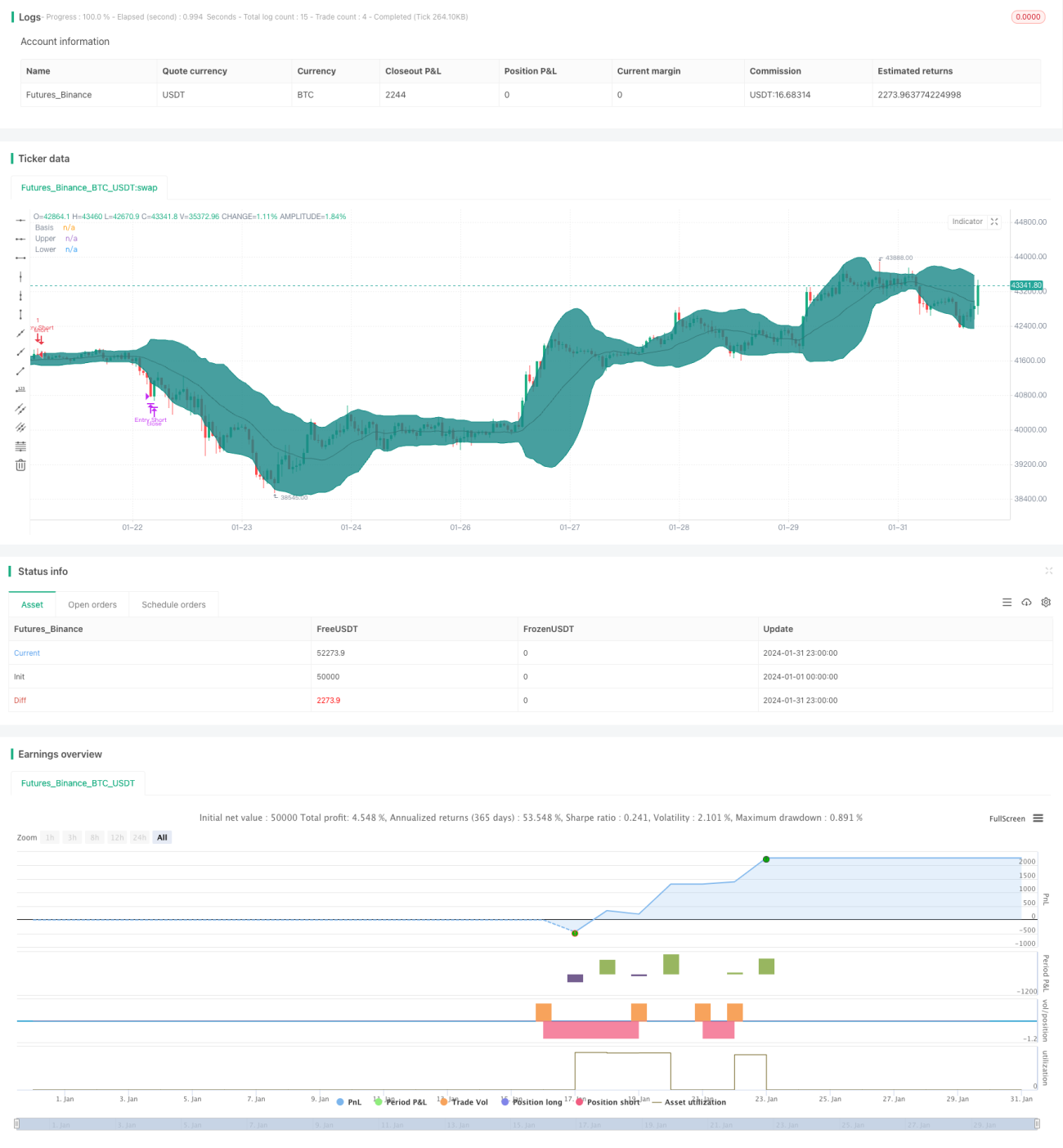

Данная стратегия объединяет несколько технических индикаторов. Когда индикатор полос Боллинджера подает сигнал о развороте цены, она использует RSI, ADX и ATR для оценки рыночной структуры, чтобы найти высоковероятные разворотные торговые возможности.

Принцип стратегии

-

Используются полосы Боллинджера с периодом 20. При достижении ценой верхней или нижней границы ожидается формирование разворотной свечи, дающей сигнал на покупку или продажу.

-

Индикатор RSI определяет, находится ли рынок в диапазоне консолидации: RSI выше 60 указывает на бычий диапазон, ниже 40 — на медвежий.

-

ADX ниже 20 указывает на боковой рынок, выше 20 — на трендовое состояние.

-

Установка стоп-лосса на основе ATR и трейлинг-стопа.

-

Фильтрация сигналов с помощью скользящей средней EMA.

Преимущества стратегии

-

Объединение нескольких индикаторов формирует высоковероятные торговые сигналы.

-

Настраиваемые параметры позволяют адаптироваться к разным рыночным условиям.

-

Строгие правила стоп-лосса эффективно контролируют риск.

Анализ рисков стратегии

-

Неправильная настройка параметров может привести к чрезмерно частым сделкам.

-

Вероятность неудачных разворотов сохраняется.

-

Трейлинг-стоп может не сработать на определенных рынках.

Направления оптимизации

-

Протестировать больше комбинаций индикаторов для поиска более подходящих настроек параметров.

-

После неудачного пробоя своевременно выявлять возможности продолжения разворота.

-

Протестировать различные способы установки стоп-лосса для его интеллектуализации.

Заключение

Данная стратегия использует полосы Боллинджера как базовый торговый сигнал, а несколько вспомогательных индикаторов образуют высоковероятную систему фильтрации. Правила стоп-лосса также достаточно полны. Путем настройки параметров и оптимизации индикаторов можно дополнительно усилить результаты стратегии. В целом, стратегия формирует надежную систему разворотной торговли.

- 1