رجحان بریک آؤٹ موونگ ایوریج ٹریکنگ حکمت عملی

جائزہ

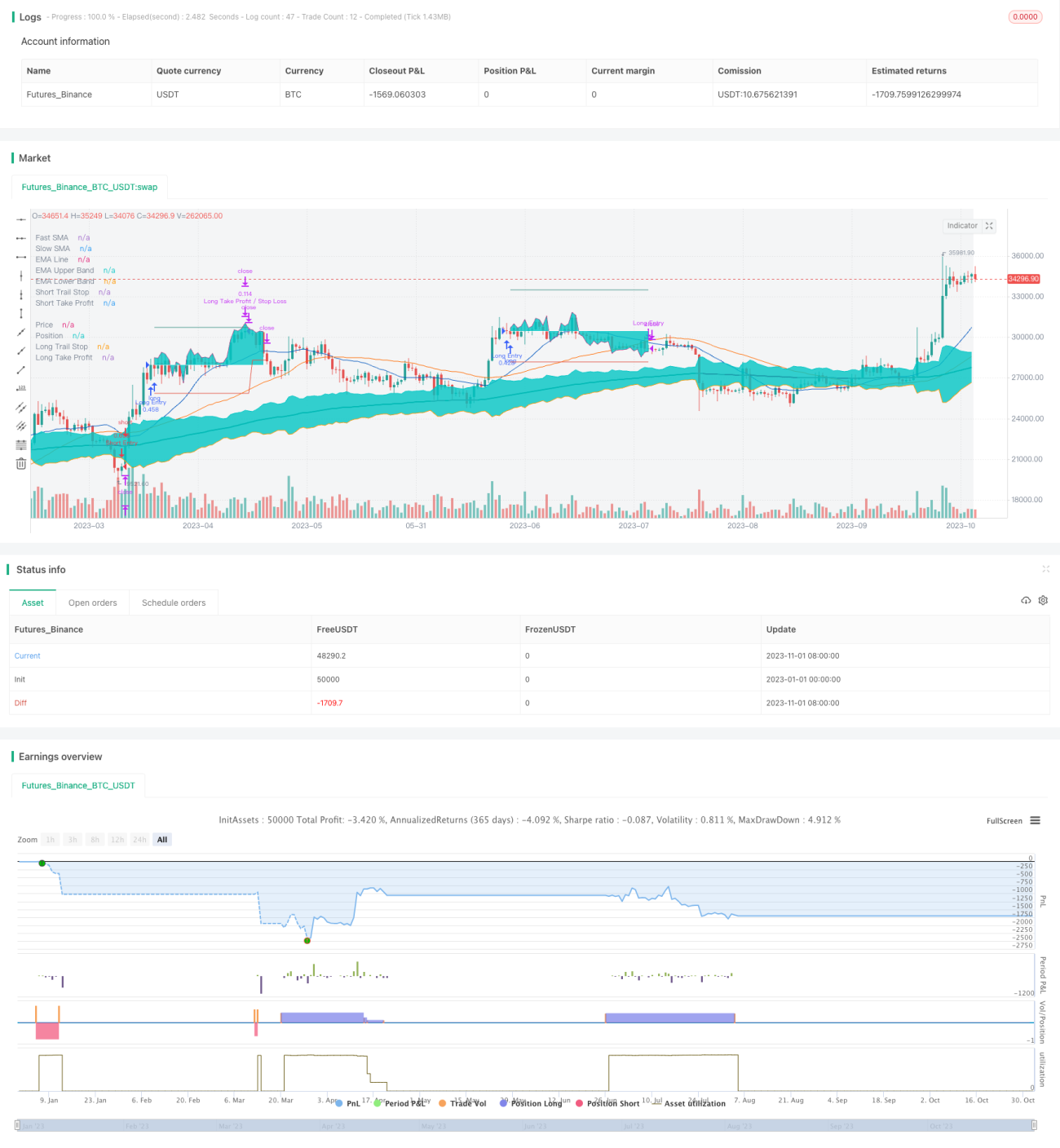

یہ حکمت عملی سادہ موونگ اوسط کے گولڈن کراس اور ڈیتھ کراس کے ذریعے رجحان کی سمت کا تعین کرتی ہے، رجحان کے آغاز میں پوری پوزیشن کے ساتھ لمبی یا چھوٹی پوزیشن کھولتی ہے، اور رسک کنٹرول کے لیے اسٹاپ لاس اور ٹیک پرافٹ آرڈر رکھتی ہے۔ پوزیشن کھولنے کے بعد، موونگ اوسط کے ذریعے مسلسل رجحان کی پیروی کی جاتی ہے، اور رجحان کی مخالفت ہونے پر بروقت نقصان روک لیا جاتا ہے۔ اس حکمت عملی میں قابل ترتیب اسٹاپ لاس، ٹیک پرافٹ اور پوزیشن مینجمنٹ ماڈیول بھی ہیں، جس سے پیرامیٹرز کو لچکدار طریقے سے ایڈجسٹ کیا جا سکتا ہے اور یہ مختلف مصنوعات کے لیے موزوں ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر سادہ موونگ اوسط کے گولڈن کراس اور ڈیتھ کراس کے ذریعے رجحان کے آغاز اور اختتام کا تعین کرتی ہے۔ حکمت عملی پہلے تیز رفتار SMA (مثلاً 21 دن کی لائن) اور سست رفتار SMA (مثلاً 49 دن کی لائن) کے تعلق کی بنیاد پر رجحان کی سمت کا تعین کرتی ہے۔ جب تیز رفتار لائن نیچے سے اوپر آ کر سست رفتار لائن کو عبور کرتی ہے تو مارکیٹ میں اوپر کا رجحان سمجھا جاتا ہے اور اس وقت لمبی پوزیشن کھولی جاتی ہے۔ جب تیز رفتار لائن اوپر سے نیچے آ کر سست رفتار لائن کو عبور کرتی ہے تو مارکیٹ میں نیچے کا رجحان سمجھا جاتا ہے اور اس وقت چھوٹی پوزیشن کھولی جاتی ہے۔

پوزیشن کھولنے کے بعد، حکمت عملی قیمت اور SMA کے تعلق کی حقیقی وقت میں نگرانی کرتی ہے۔ جب قیمت اوپر سے نیچے آ کر SMA کو عبور کرتی ہے تو اوپر کا رجحان ختم سمجھا جاتا ہے اور لمبی پوزیشن بند کر دی جاتی ہے۔ جب قیمت نیچے سے اوپر آ کر SMA کو عبور کرتی ہے تو نیچے کا رجحان ختم سمجھا جاتا ہے اور چھوٹی پوزیشن بند کر دی جاتی ہے۔

خطرے پر قابو پانے کے لیے، حکمت عملی پوزیشن کھولتے وقت اسی وقت اسٹاپ لاس اور ٹیک پرافٹ آرڈر بھی دیتی ہے۔ اسٹاپ لاس کا فاصلہ ATR کی بنیاد پر سیٹ کیا جاتا ہے، جبکہ ٹیک پرافٹ کا فاصلہ فیصد کی بنیاد پر یا ATR کی بنیاد پر منتخب کیا جا سکتا ہے۔ پوزیشن کھولنے کے بعد، اسٹاپ لاس قیمت کی حقیقی وقت میں پیروی کرتا ہے، جس سے رجحان کی پیروی کا اثر حاصل ہوتا ہے۔ ٹیک پرافٹ تک پہنچنے پر پوزیشن کا ایک حصہ بند ہو جاتا ہے، باقی حصہ مکمل بند ہونے تک پیروی کرتا رہتا ہے۔

اس حکمت عملی میں پوزیشن مینجمنٹ ماڈیول بھی ہے جو ہر تجارت میں سرمائے کے استعمال کی شرح کو محدود کر سکتا ہے، اس طرح ایک ہی تجارت کے خطرے کی نمائش کو کنٹرول کیا جا سکتا ہے۔ اسی کے ساتھ، زیادہ سے زیادہ ڈرا ڈاؤن کی ترتیب حکمت عملی کے مجموعی خطرے کو کنٹرول کر سکتی ہے۔

حکمت عملی کے فوائد

- موونگ اوسط کے موازنے سے رجحان کی سمت کا تعین، اصول سمجھنے میں آسان

- پوزیشن کھولنے کے بعد حقیقی وقت میں اسٹاپ لاس کی پیروی، زیادہ تر منافع کو محفوظ کیا جا سکتا ہے

- قابل ترتیب اسٹاپ لاس اور ٹیک پرافٹ کے طریقے، مختلف مصنوعات کے مطابق ایڈجسٹ کیا جا سکتا ہے

- ایک ہی تجارت میں خطرہ قابل کنٹرول، پورے سرمائے کے ساتھ تجارت نہیں کرتا

- زیادہ سے زیادہ ڈرا ڈاؤن کی ترتیب، حکمت عملی کے مجموعی نقصان کو محدود کر سکتی ہے

خطرات اور حل

- ڈبل موونگ اوسط کراس میں کچھ تاخیر ہوتی ہے، رجحان کے آغاز کے بہترین داخلے کے مقام سے محروم ہو سکتے ہیں

- پیرامیٹرز کو بار بار ایڈجسٹ کرنے کی ضرورت، مختلف ادوار کی موونگ اوسط کے امتزاج کی جانچ

- موونگ اوسط کراس میں کچھ غلط سگنل ہوتے ہیں، داخلے کی درستگی 100% نہیں ہو سکتی

- فالو اپ اسٹاپ لاس آسانی سے ٹوٹ سکتا ہے، تمام منافع کو محفوظ نہیں کر سکتا

- اسٹاپ لاس کے فاصلے کو مناسب طور پر ڈھیلا رکھنا ضروری ہے، قیمت کو کچھ واپسی کی گنجائش دینا

- زیادہ سے زیادہ ڈرا ڈاؤن کی حد بہت قدامت پسند ہو سکتی ہے، اوپر کے مواقع کھو سکتے ہیں

- زیادہ سے زیادہ ڈرا ڈاؤن کے تناسب کو مناسب طور پر بڑھایا جا سکتا ہے، حکمت عملی کو زیادہ غلطی کی گنجائش دینا

بہتری کی سمت

- مختلف پیرامیٹر امتزاج آزمائیں، بہترین موونگ اوسط ادوار کا انتخاب کریں

- رجحان کی طاقت کا اشارہ شامل کریں، داخلے کی درستگی بہتر بنائیں

- اسٹاپ لاس کی حکمت عملی کو بہتر بنائیں، رجحان میں زیادہ سے زیادہ قیمت کے ساتھ چلیں

- مختلف ٹیک پرافٹ حکمت عملیوں کی جانچ کریں، بہترین ٹیک پرافٹ پوائنٹ کا انتخاب کریں

- پوزیشن مینجمنٹ کے منصوبے کو بہتر بنائیں، سرمائے کے استعمال کی کارکردگی بڑھائیں

- زیادہ سے زیادہ ڈرا ڈاؤن کی ترتیب کو ایڈجسٹ کریں، منافع اور خطرے میں توازن رکھیں

خلاصہ

یہ حکمت عملی مجموعی طور پر ابتدائیوں کے لیے ایک بہت موزوں داخلے کی حکمت عملی ہے، جس کے اصول سادہ اور سمجھنے اور سیکھنے میں آسان ہیں۔ اسی کے ساتھ اس میں مناسب خطرے پر قابو پانے کی صلاحیت بھی ہے، جس سے بڑے نقصان کے امکانات کم ہو سکتے ہیں۔ پیرامیٹر کی بہتری سے اچھے نتائج حاصل کیے جا سکتے ہیں۔ تاہم، اس کی بنیادی خامیاں اسے انتہائی درست آپریشن کرنے سے روکتی ہیں۔ تجویز ہے کہ اسے ابتدائی مشق کی حکمت عملی کے طور پر استعمال کیا جائے، لیکن یہ اعلی کارکردگی اور اعلی جیت کی شرح کے خواہاں تاجروں کے لیے موزوں نہیں ہے۔ اگر بہتر تجارتی نتائج حاصل کرنے ہیں تو مضبوط پیش گوئی کی صلاحیت رکھنے والی حکمت عملی تلاش کرنی ہوگی۔

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1