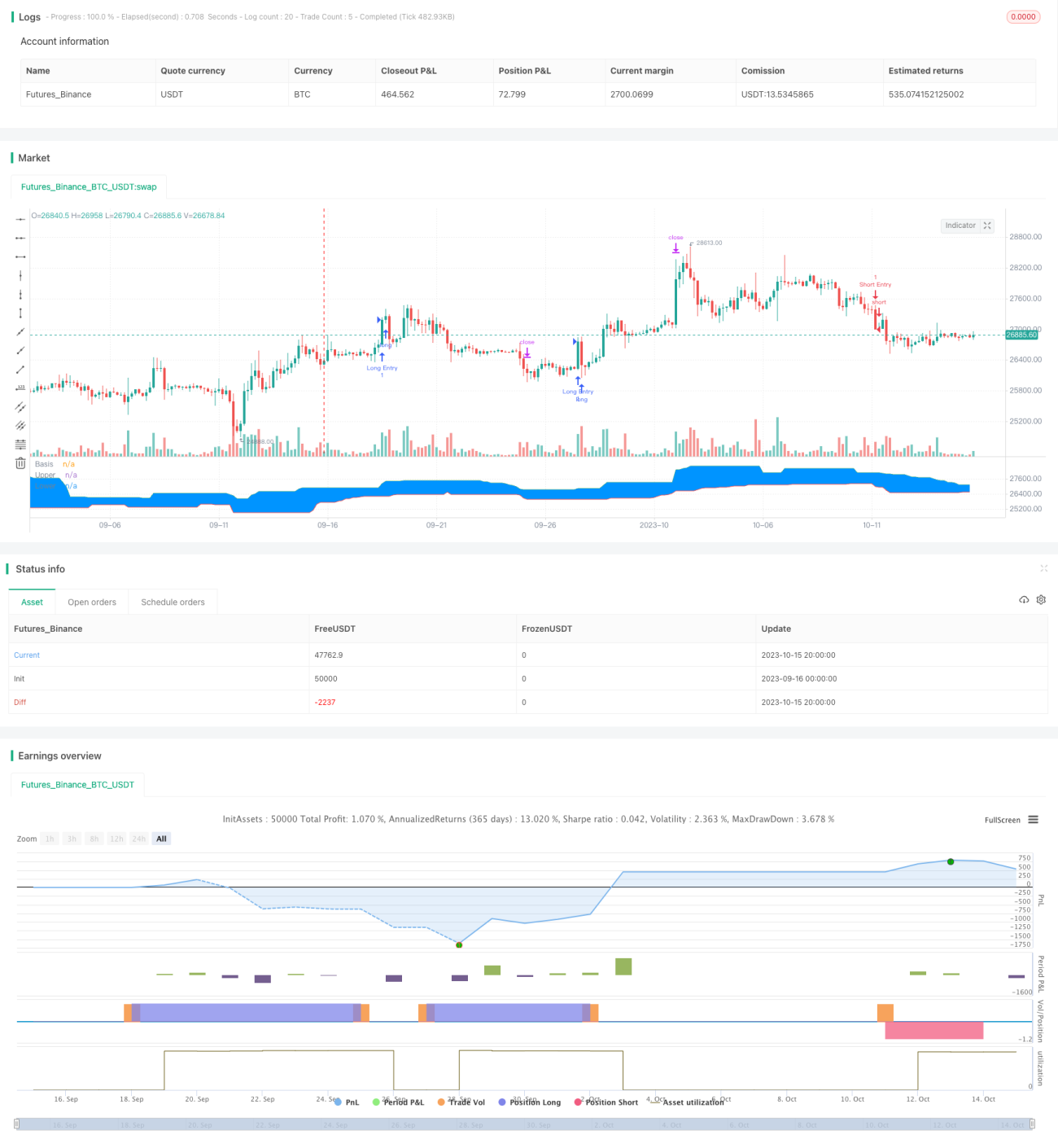

Chiến lược đột phá theo dõi

Tổng quan

Chiến lược này chủ yếu thực hiện giao dịch phá vỡ theo xu hướng thông qua chỉ báo "Kênh Donchian". Chiến lược kết hợp hai tư duy giao dịch: xu hướng và phá vỡ, dựa trên đánh giá xu hướng dài hạn, tìm kiếm điểm phá vỡ trong chu kỳ ngắn hơn để vào lệnh, thực hiện giao dịch thuận theo xu hướng trong thị trường có xu hướng. Ngoài ra, chiến lược còn thiết lập mức cắt lỗ và chốt lời để kiểm soát tỷ lệ lợi nhuận/rủi ro cho mỗi giao dịch. Nhìn chung, chiến lược có lợi thế bám theo xu hướng, có thể thuận theo xu hướng và nắm bắt cơ hội xu hướng dài hạn.

Nguyên lý chiến lược

- Thiết lập tham số của chỉ báo "Kênh Donchian", mặc định chu kỳ 20;

- Thiết lập đường trung bình động làm mịn EMA, mặc định chu kỳ 200;

- Thiết lập tỷ lệ lợi nhuận/rủi ro, mặc định 1,5;

- Thiết lập tham số phá vỡ và hồi lại, lần lượt cho vị thế mua và vị thế bán;

- Ghi nhận lần phá vỡ trước đó là đỉnh cao hay đáy thấp;

- Tín hiệu mua: Nếu lần phá vỡ trước đó là đáy thấp, và giá cao hơn dải trên của Kênh Donchian đồng thời cao hơn đường EMA, thì tạo tín hiệu mua;

- Tín hiệu bán: Nếu lần phá vỡ trước đó là đỉnh cao, và giá thấp hơn dải dưới của Kênh Donchian đồng thời thấp hơn đường EMA, thì tạo tín hiệu bán;

- Sau khi vào vị thế mua, đặt cắt lỗ tại dải dưới của Kênh Donchian trừ đi 5 điểm, chốt lời bằng tỷ lệ lợi nhuận/rủi ro nhân với khoảng cách cắt lỗ;

- Sau khi vào vị thế bán, đặt cắt lỗ tại dải trên của Kênh Donchian cộng thêm 5 điểm, chốt lời bằng tỷ lệ lợi nhuận/rủi ro nhân với khoảng cách cắt lỗ.

Bằng cách này, chiến lược kết hợp đánh giá xu hướng và giao dịch phá vỡ, có thể thuận theo xu hướng, nắm bắt cơ hội trong chu kỳ ngắn hơn khi xu hướng dài hạn tồn tại. Đồng thời, thiết lập cắt lỗ và chốt lời có thể kiểm soát tỷ lệ lợi nhuận/rủi ro cho mỗi giao dịch.

Phân tích ưu điểm

- Bám theo xu hướng dài hạn, thuận theo xu hướng, tránh giao dịch ngược xu hướng.

- Kênh Donchian là chỉ báo dài hạn, kết hợp với bộ lọc EMA, có thể đánh giá hướng xu hướng khá tốt.

- Cơ chế cắt lỗ và chốt lời kiểm soát rủi ro mỗi lệnh, hạn chế tổn thất có thể xảy ra.

- Tối ưu tỷ lệ lợi nhuận/rủi ro, có thể mở rộng tỷ lệ lãi/lỗ, theo đuổi lợi nhuận vượt trội.

- Tham số backtest linh hoạt, có thể điều chỉnh tổ hợp tham số tối ưu cho các thị trường khác nhau.

Phân tích rủi ro

- Kênh Donchian và đường EMA là chỉ báo lọc có thể đưa ra tín hiệu sai.

- Giao dịch phá vỡ dễ bị mắc kẹt, cần xác định rõ bối cảnh xu hướng.

- Khoảng cách cắt lỗ và chốt lời cố định, không thể điều chỉnh theo mức độ biến động của thị trường.

- Không gian tối ưu tham số hạn chế, hiệu quả giao dịch thực tế khó đảm bảo.

- Hệ thống giao dịch không chịu được nhiều sự kiện ngẫu nhiên, sự kiện thiên nga đen có thể gây thua lỗ lớn.

Hướng tối ưu

- Có thể cân nhắc thêm nhiều chỉ báo để lọc, ví dụ chỉ báo dao động, nâng cao chất lượng tín hiệu.

- Có thể thiết lập cắt lỗ và chốt lời thông minh, điều chỉnh vị trí lãi/lỗ động dựa trên mức độ biến động thị trường và chỉ báo ATR.

- Có thể sử dụng phương pháp học máy để kiểm tra và tối ưu tham số, làm cho nó gần với thị trường thực hơn.

- Có thể tối ưu logic vào lệnh, thiết lập chỉ báo khối lượng hoặc độ biến động làm điều kiện phụ trợ, tránh bẫy.

- Có thể cân nhắc kết hợp với chiến lược theo đuổi xu hướng hoặc học máy, hình thành chiến lược hỗn hợp, nâng cao tính ổn định.

Tổng kết

Chiến lược này, với tư cách là một chiến lược phá vỡ theo xu hướng, ý tưởng cốt lõi là trên cơ sở xác định xu hướng dài hạn, lấy tín hiệu phá vỡ để giao dịch thuận xu hướng, đồng thời thiết lập cắt lỗ và chốt lời để kiểm soát rủi ro mỗi giao dịch. Chiến lược này có những ưu điểm nhất định, nhưng cũng tồn tại một số không gian tối ưu. Nhìn chung, nếu có thể xử lý tốt các vấn đề như cài đặt tham số, lựa chọn thời điểm vào lệnh, và kết hợp với các kỹ thuật khác để tăng cường, chiến lược này có thể trở thành một chiến lược theo đuổi xu hướng thực dụng. Tuy nhiên, nhà đầu tư vẫn cần nhớ rằng bất kỳ hệ thống giao dịch nào cũng không thể tránh khỏi rủi ro thị trường hoàn toàn, cần quản lý rủi ro tốt.

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1