Chiến lược giao dịch hai chiều dài ngắn với đường RSI hai dải

Tổng quan

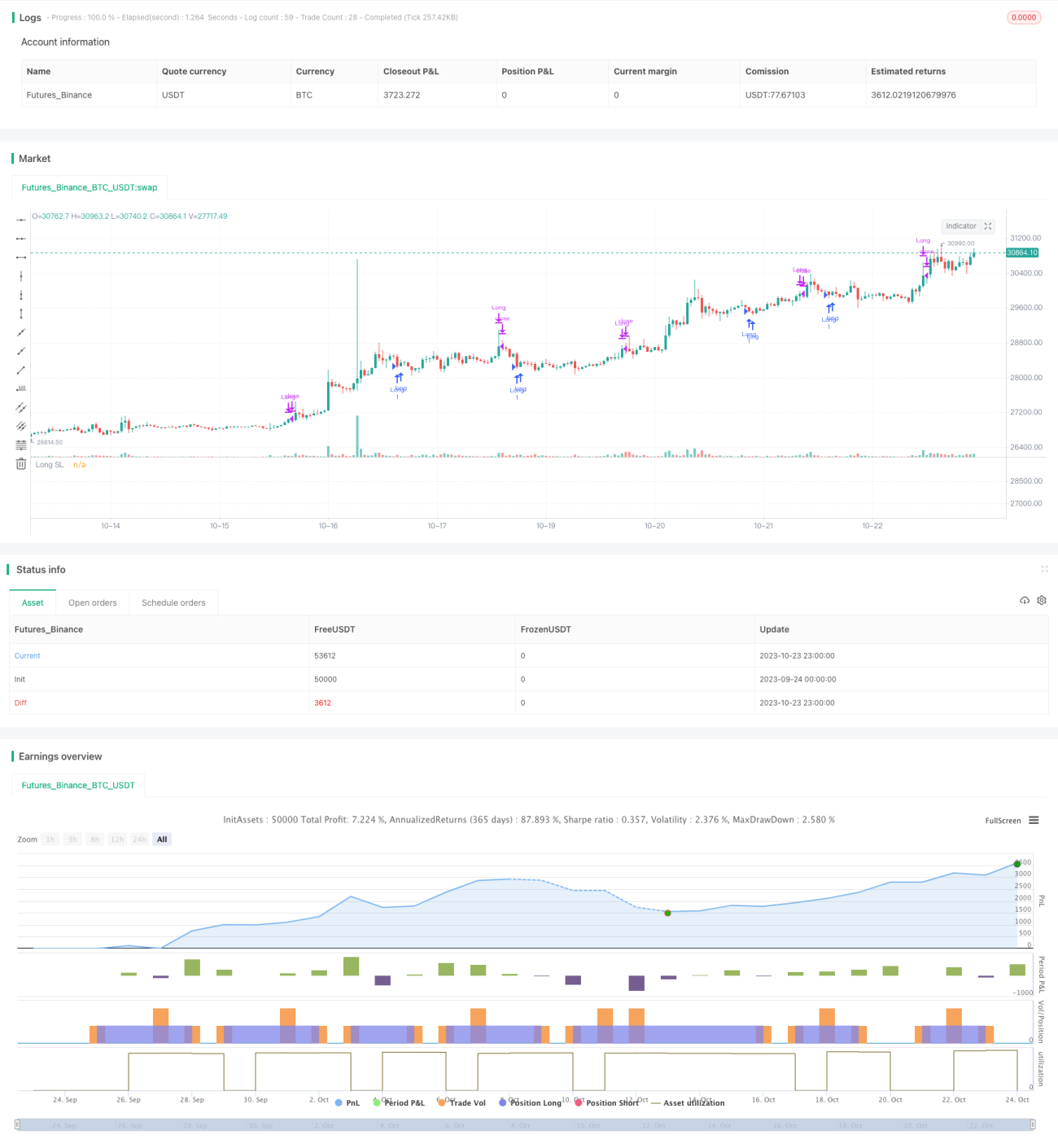

Chiến lược giao dịch hai chiều với dải dao động RSI kép là một chiến lược sử dụng chỉ báo RSI để thực hiện giao dịch hai chiều. Chiến lược này dựa trên nguyên lý quá mua/quá bán của chỉ báo RSI, kết hợp với thiết lập hai dải và tín hiệu giao dịch từ đường trung bình động, nhằm đạt được hiệu quả mở và đóng vị thế hai chiều.

Nguyên lý chiến lược

Chiến lược này chủ yếu đưa ra quyết định giao dịch dựa trên nguyên lý quá mua/quá bán của chỉ báo RSI. Đầu tiên, chiến lược tính toán giá trị của chỉ báo RSI (vrsi), cùng với dải trên (sn) và dải dưới (ln) của hai dải. Khi giá trị RSI cắt xuống dưới dải dưới (ln) sẽ tạo ra tín hiệu mua (long), và khi giá trị RSI cắt lên trên dải trên (sn) sẽ tạo ra tín hiệu bán (short).

Chiến lược cũng phát hiện sự thay đổi tăng giảm của nến, từ đó tạo ra thêm tín hiệu mua và bán. Cụ thể, khi nến phá vỡ từ dưới lên trên sẽ tạo ra tín hiệu mua (longLogic), khi nến phá vỡ từ trên xuống dưới sẽ tạo ra tín hiệu bán (shortLogic). Ngoài ra, chiến lược cung cấp công tắc tham số, có thể chỉ mua, chỉ bán, hoặc đảo ngược tín hiệu.

Sau khi tạo ra tín hiệu mua/bán, chiến lược sẽ thống kê số lần tín hiệu và kiểm soát số lần mở vị thế. Thông qua tham số, có thể thiết lập các quy tắc thêm vị thế khác nhau. Điều kiện đóng vị thế bao gồm chốt lời, cắt lỗ, cắt lỗ trượt, v.v., có thể thiết lập các tỷ lệ phần trăm chốt lời/cắt lỗ khác nhau.

Tóm lại, chiến lược này kết hợp nhiều kỹ thuật như chỉ báo RSI, giao cắt đường trung bình động, thống kê thêm vị thế, chốt lời/cắt lỗ để thực hiện giao dịch hai chiều tự động.

Ưu điểm của chiến lược

- Sử dụng nguyên lý quá mua/quá bán của chỉ báo RSI để thiết lập vị thế mua/bán ở mức hợp lý.

- Thiết lập hai dải giúp tránh tín hiệu sai. Dải trên ngăn vị thế mua đóng quá sớm, dải dưới ngăn vị thế bán đóng quá sớm.

- Tín hiệu giao dịch từ đường trung bình động lọc các đột phá giả. Chỉ khi giá phá vỡ đường trung bình động mới tạo tín hiệu, tránh tín hiệu nhiễu.

- Thống kê số lần tín hiệu và số lần thêm vị thế để kiểm soát rủi ro.

- Có thể tùy chỉnh tỷ lệ phần trăm chốt lời/cắt lỗ, kiểm soát lợi nhuận và rủi ro.

- Cắt lỗ trượt giúp theo dõi và khóa lợi nhuận thêm.

- Có thể chỉ mua, chỉ bán hoặc đảo ngược tín hiệu, thích ứng với các điều kiện thị trường khác nhau.

- Hệ thống giao dịch tự động, giảm chi phí thao tác thủ công.

Rủi ro của chiến lược

- Chỉ báo RSI có rủi ro đảo chiều thất bại. Khi RSI vào vùng quá mua/quá bán, không nhất thiết sẽ đảo chiều.

- Điểm chốt lời/cắt lỗ cố định có rủi ro bị kẹt. Thiết lập chốt lời/cắt lỗ không phù hợp có thể dẫn đến cắt lỗ hoặc chốt lời quá sớm.

- Phụ thuộc vào chỉ báo kỹ thuật, có rủi ro tối ưu hóa tham số. Tham số chỉ báo không phù hợp sẽ ảnh hưởng đến hiệu quả chiến lược.

- Nhiều điều kiện kích hoạt đồng thời, có rủi ro bỏ sót lệnh.

- Hệ thống giao dịch tự động có rủi ro lỗi bất thường.

Để đối phó với các rủi ro trên, có thể tối ưu thiết lập tham số, điều chỉnh chiến lược chốt lời/cắt lỗ, thêm bộ lọc thanh khoản, tối ưu logic tạo tín hiệu, thêm giám sát lỗi bất thường, v.v.

Hướng tối ưu hóa chiến lược

- Kiểm tra tham số chu kỳ khác nhau để tối ưu tham số chỉ báo RSI.

- Kiểm tra các thiết lập tỷ lệ phần trăm chốt lời/cắt lỗ khác nhau.

- Thêm bộ lọc khối lượng giao dịch hoặc tỷ suất lợi nhuận để tránh thiếu thanh khoản.

- Tối ưu logic tạo tín hiệu, cải thiện cách giao cắt đường trung bình động.

- Thêm backtest nhiều khung thời gian để xác minh tính ổn định.

- Cân nhắc thêm các chỉ báo khác để tối ưu hiệu quả tín hiệu.

- Thêm chiến lược quản lý vị thế.

- Thêm giám sát lỗi bất thường.

- Tối ưu thuật toán cắt lỗ trượt tự động.

- Cân nhắc thêm học máy để cải thiện chiến lược.

Tổng kết

Chiến lược giao dịch hai chiều với dải dao động RSI kép đã đạt được giao dịch hai chiều tự động thông qua việc kết hợp nhiều kỹ thuật như chỉ báo RSI, nguyên lý thống kê mở vị thế và cắt lỗ. Chiến lược này có tính tùy chỉnh cao, người dùng có thể điều chỉnh tham số theo nhu cầu để thích ứng với các điều kiện thị trường khác nhau. Đồng thời, chiến lược cũng có một số không gian cải thiện, có thể tối ưu từ việc thiết lập tham số, chiến lược quản lý rủi ro, logic tạo tín hiệu, v.v., giúp chiến lược ổn định và đáng tin cậy hơn. Nhìn chung, chiến lược này cung cấp cho người dùng một giải pháp giao dịch định lượng tương đối hiệu quả.

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1