Chiến lược giao dịch thuật toán theo dõi hai đường

Tổng quan

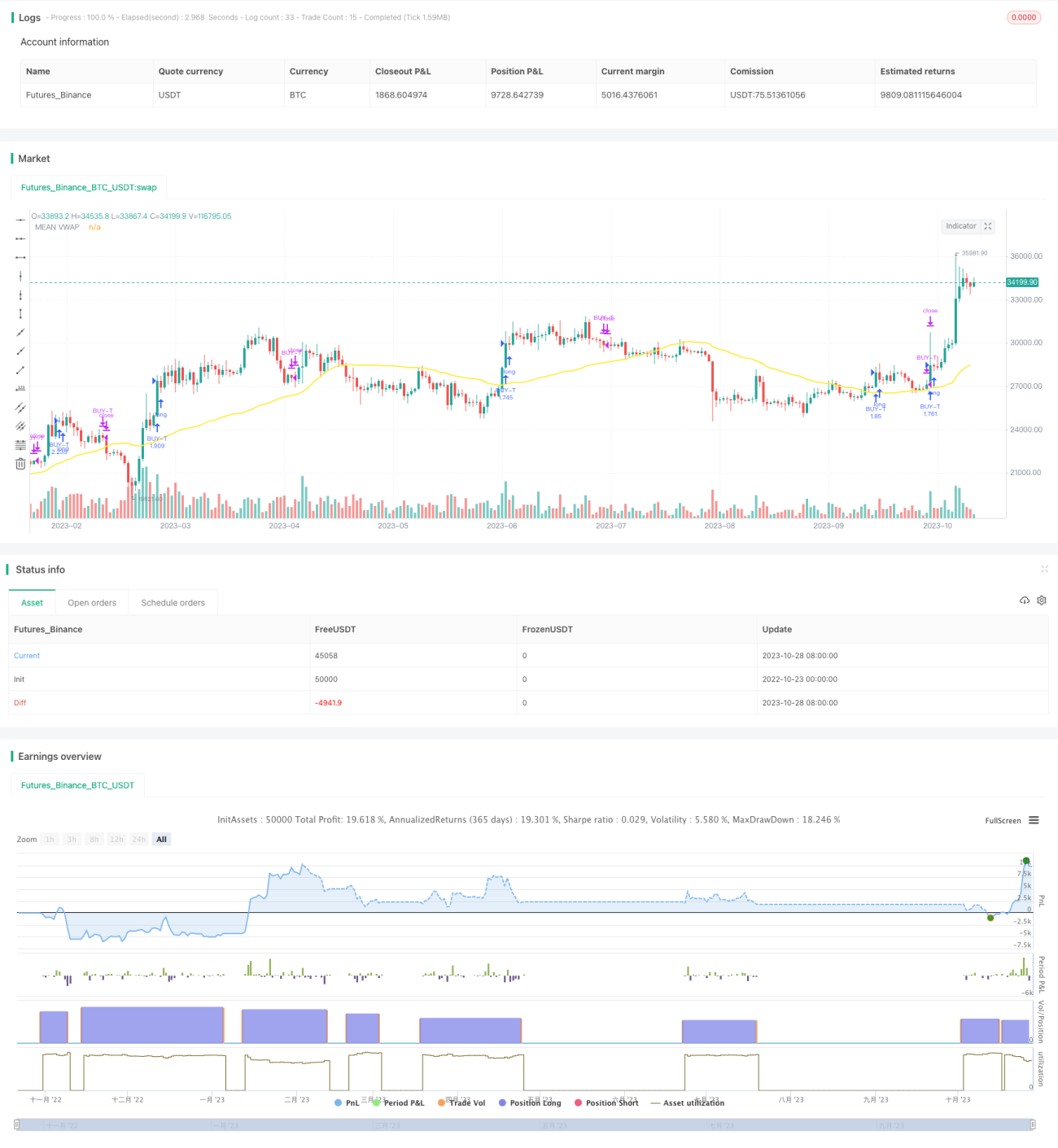

Chiến lược này chủ yếu sử dụng nguyên lý giao nhau của đường trung bình động, kết hợp với tín hiệu đảo chiều của chỉ báo RSI, cùng với thuật toán theo dõi hai đường tự động để thực hiện giao dịch theo dấu hiệu giao nhau của đường trung bình. Chiến lược theo dõi sự giao nhau của hai đường trung bình động với các chu kỳ khác nhau: một đường trung bình nhanh theo dõi xu hướng ngắn hạn, một đường trung bình chậm theo dõi xu hướng dài hạn. Khi đường trung bình nhanh cắt lên trên đường trung bình chậm, cho thấy xu hướng ngắn hạn đi lên, có thể mua vào; khi đường trung bình nhanh cắt xuống dưới đường trung bình chậm, cho thấy xu hướng ngắn hạn kết thúc, nên đóng vị thế.

Nguyên lý chiến lược

-

Tính toán hai bộ đường trung bình VWAP với các tham số khác nhau, đại diện cho xu hướng dài hạn và ngắn hạn

- Đường màn trời chậm và đường cơ sở tính toán xu hướng dài hạn

- Đường màn trời nhanh và đường cơ sở tính toán xu hướng ngắn hạn

-

Lấy giá trị trung bình của hai bộ đường màn trời và đường cơ sở làm đường trung bình chậm và đường trung bình nhanh

-

Tính toán chỉ báo Bollinger Bands để xác định vùng tích lũy và đột phá

- Đường giữa là giá trị trung bình của đường trung bình nhanh và đường trung bình chậm

- Dải trên và dải dưới của Bollinger Bands dùng để xác định đột phá

-

Tính toán chỉ báo TSV để đánh giá năng lượng khối lượng giao dịch

- TSV lớn hơn 0 cho thấy lực tăng lớn hơn lực giảm

- TSV lớn hơn đường EMA của nó cho thấy lực đang mạnh lên

-

Tính toán chỉ báo RSI để xác định vùng quá mua/quá bán

- RSI dưới 30 là vùng quá bán, có thể mua vào

- RSI trên 70 là vùng quá mua, nên bán ra

-

Điều kiện vào lệnh:

- Đường trung bình nhanh cắt lên trên đường trung bình chậm

- Giá đóng cửa cắt lên trên dải trên của Bollinger Bands

- TSV lớn hơn 0 và lớn hơn đường EMA của nó

- RSI dưới 30

-

Điều kiện thoát lệnh:

- Đường trung bình nhanh cắt xuống dưới đường trung bình chậm

- RSI trên 70

Phân tích ưu điểm

-

Sử dụng hệ thống hai đường trung bình, có thể đồng thời nắm bắt xu hướng ngắn hạn và dài hạn

-

Chỉ báo RSI tránh mua vào vùng quá mua, bán ra vùng quá bán

-

Chỉ báo TSV đảm bảo có đủ khối lượng giao dịch hỗ trợ xu hướng

-

Tận dụng Bollinger Bands để xác định các điểm đột phá quan trọng

-

Kết hợp nhiều chỉ báo, có thể lọc hiệu quả các tín hiệu đột phá giả

Phân tích rủi ro

-

Hệ thống đường trung bình dễ tạo ra tín hiệu sai, cần chỉ báo phụ trợ để lọc

-

Tham số của chỉ báo RSI cần tối ưu, nếu không có thể bỏ lỡ điểm mua/bán

-

Chỉ báo TSV cũng nhạy cảm với tham số, cần kiểm tra kỹ lưỡng

-

Đột phá dải trên của Bollinger Bands có thể là đột phá giả, cần xác nhận

-

Kết hợp nhiều chỉ báo, khó tối ưu tham số, dễ dẫn đến overfitting

-

Dữ liệu huấn luyện và kiểm tra không đầy đủ có thể dẫn đến đường cong phù hợp

Hướng tối ưu hóa

-

Kiểm tra thêm nhiều tham số chu kỳ, tìm tổ hợp tham số tối ưu

-

Thử nghiệm các chỉ báo khác như MACD, KD thay thế hoặc kết hợp với RSI

-

Tối ưu tham số cần tận dụng phân tích walk forward

-

Thêm chiến lược cắt lỗ để kiểm soát thua lỗ từng lệnh

-

Cân nhắc thêm mô hình học máy hỗ trợ nhận định tín hiệu

-

Điều chỉnh tham số cho từng thị trường khác nhau, không phụ thuộc quá nhiều vào một tổ hợp tham số duy nhất

Tổng kết

Chiến lược này thông qua hệ thống hai đường trung bình nắm bắt xu hướng ngắn hạn và dài hạn, đồng thời sử dụng nhiều chỉ báo như RSI, TSV, Bollinger Bands để lọc tín hiệu. Ưu điểm của chiến lược là có thể đi theo xu hướng, nắm bắt các đợt sóng tăng dài hạn. Tuy nhiên, cũng tồn tại một số rủi ro về tín hiệu giả, cần tối ưu hóa tham số và kiểm soát cắt lỗ để giảm rủi ro. Nhìn chung, chiến lược kết hợp theo dõi xu hướng và chỉ báo đảo chiều, hiệu quả tốt trong thị trường tăng dài hạn, nhưng cần điều chỉnh getParameter cho từng thị trường khác nhau.

- 1