Chiến lược theo dõi đường trung bình động phá vỡ xu hướng

Tổng quan

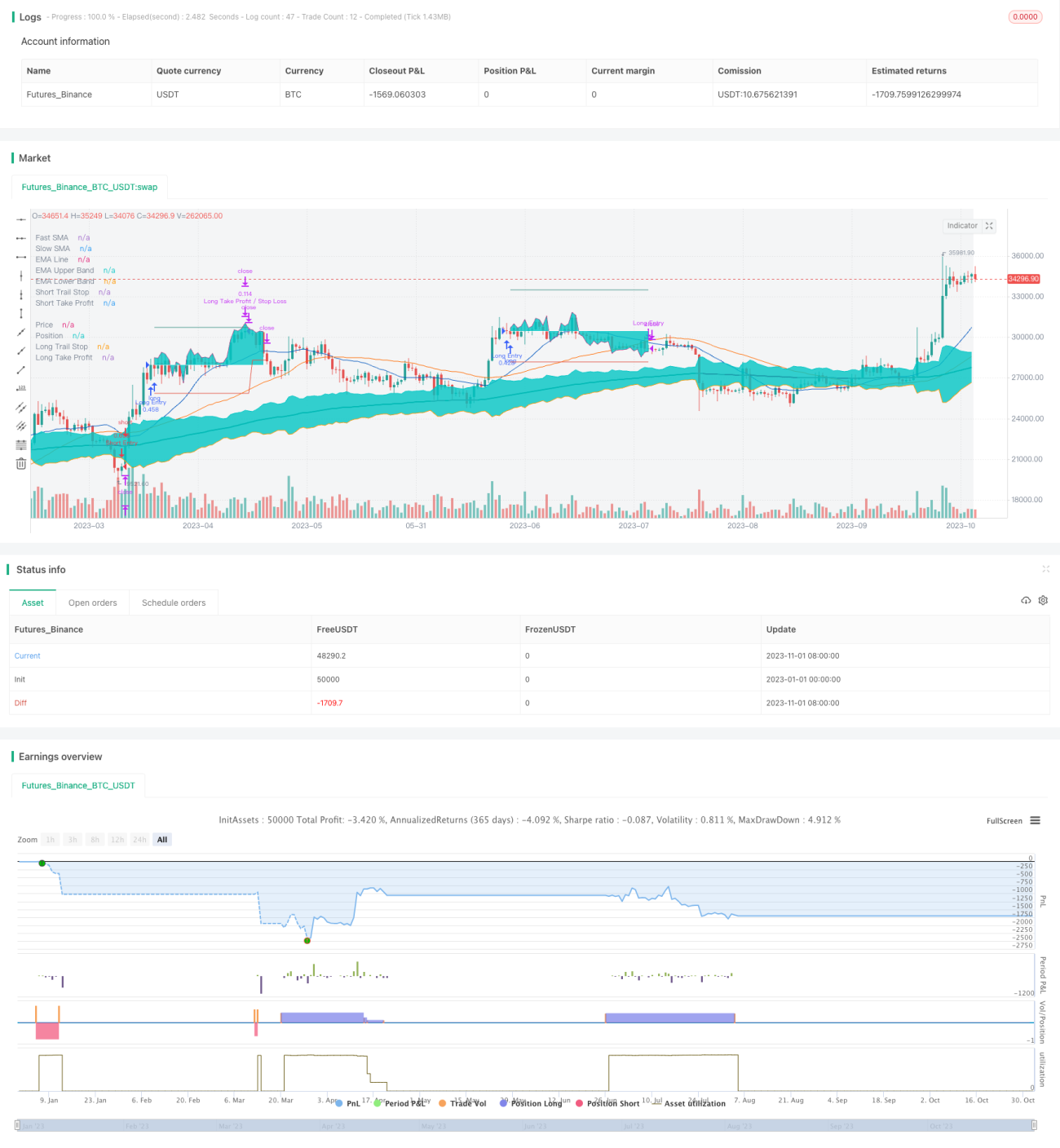

Chiến lược này sử dụng giao cắt vàng và giao cắt tử thần của đường trung bình động đơn giản (SMA) để xác định hướng xu hướng, vào lệnh mua/bán toàn bộ vốn khi xu hướng bắt đầu, đồng thời thiết lập lệnh dừng lỗ và chốt lời để kiểm soát rủi ro. Sau khi vào lệnh, chiến lược sẽ sử dụng đường trung bình động để theo dõi xu hướng liên tục, và cắt lỗ kịp thời khi xu hướng đảo chiều. Chiến lược này cũng có các mô-đun cấu hình cho dừng lỗ, chốt lời và quản lý vị thế, cho phép linh hoạt điều chỉnh các tham số, phù hợp với nhiều loại tài sản khác nhau.

Nguyên lý chiến lược

Chiến lược này chủ yếu xác định điểm bắt đầu và kết thúc của xu hướng dựa trên giao cắt vàng và giao cắt tử thần của đường trung bình động đơn giản. Đầu tiên, chiến lược xác định hướng xu hướng dựa trên mối quan hệ giữa SMA nhanh (ví dụ: đường 21 kỳ) và SMA chậm (ví dụ: đường 49 kỳ). Khi đường nhanh cắt lên trên đường chậm, cho rằng thị trường đang bước vào xu hướng tăng và sẽ mở lệnh mua tại thời điểm đó; khi đường nhanh cắt xuống dưới đường chậm, cho rằng thị trường đang bước vào xu hướng giảm và sẽ mở lệnh bán tại thời điểm đó.

Sau khi vào lệnh, chiến lược sẽ theo dõi mối quan hệ giữa giá và SMA theo thời gian thực. Khi giá phá vỡ xuống dưới SMA từ phía trên, cho rằng xu hướng tăng kết thúc và sẽ đóng lệnh mua; khi giá phá vỡ lên trên SMA từ phía dưới, cho rằng xu hướng giảm kết thúc và sẽ đóng lệnh bán.

Để kiểm soát rủi ro, chiến lược sẽ đồng thời đặt lệnh dừng lỗ và chốt lời khi mở vị thế. Khoảng cách dừng lỗ được thiết lập dựa trên ATR, trong khi khoảng cách chốt lời có thể được chọn theo phần trăm hoặc theo ATR. Sau khi mở vị thế, lệnh dừng lỗ sẽ theo dõi giá theo thời gian thực, tạo hiệu ứng trailing stop. Khi lệnh chốt lời được kích hoạt, một phần vị thế sẽ được thoát ra, phần còn lại tiếp tục theo dõi cho đến khi thoát hoàn toàn.

Chiến lược này còn có mô-đun quản lý vị thế, có thể giới hạn tỷ lệ sử dụng vốn cho mỗi giao dịch, từ đó kiểm soát rủi ro cho từng lệnh. Đồng thời, cài đặt mức drawdown tối đa có thể kiểm soát rủi ro tổng thể của chiến lược.

Ưu điểm của chiến lược

- Sử dụng đường trung bình động để so sánh và xác định hướng xu hướng, nguyên lý đơn giản dễ hiểu

- Sau khi vào lệnh, theo dõi dừng lỗ theo thời gian thực, có thể khóa phần lớn lợi nhuận

- Có thể cấu hình phương thức dừng lỗ và chốt lời, có thể điều chỉnh theo từng loại tài sản khác nhau

- Rủi ro từng lệnh được kiểm soát, không giao dịch toàn bộ vốn

- Cài đặt drawdown tối đa, có thể giới hạn tổng thua lỗ của chiến lược

Rủi ro và giải pháp

- Giao cắt hai đường trung bình động có độ trễ nhất định, có thể bỏ lỡ điểm vào lệnh tối ưu khi xu hướng bắt đầu

- Cần điều chỉnh tham số nhiều lần, thử nghiệm các tổ hợp chu kỳ đường trung bình động khác nhau

- Giao cắt đường trung bình động có tỷ lệ nhiễu nhất định, độ chính xác vào lệnh không thể đạt 100%

- Dừng lỗ theo dõi dễ bị phá vỡ, không thể khóa toàn bộ lợi nhuận

- Cần nới lỏng khoảng cách dừng lỗ phù hợp, để giá có không gian điều chỉnh

- Giới hạn drawdown tối đa có thể quá thận trọng, làm mất cơ hội tăng giá

- Có thể nới rộng tỷ lệ drawdown tối đa, cho chiến lược thêm không gian sai sót

Hướng tối ưu hóa

- Thử nghiệm các tổ hợp tham số khác nhau, chọn chu kỳ đường trung bình động tối ưu nhất

- Thêm các chỉ báo sức mạnh xu hướng, cải thiện độ chính xác khi vào lệnh

- Tối ưu hóa chiến lược dừng lỗ, cố gắng bám theo xu hướng khi giá tăng/giảm

- Thử nghiệm các chiến lược chốt lời khác nhau, chọn điểm chốt lời tối ưu

- Tối ưu hóa phương án quản lý vị thế, nâng cao hiệu quả sử dụng vốn

- Điều chỉnh cài đặt drawdown tối đa, cân bằng giữa lợi nhuận và rủi ro

Tổng kết

Nhìn chung, chiến lược này là một chiến lược nhập môn rất phù hợp cho người mới, nguyên lý đơn giản, dễ hiểu và dễ nắm bắt. Đồng thời, nó cũng có khả năng kiểm soát rủi ro thích hợp, giúp giảm xác suất thua lỗ lớn. Thông qua tối ưu hóa tham số, có thể đạt được hiệu quả khả quan. Tuy nhiên, các khiếm khuyết cố hữu của nó cũng quyết định rằng nó không thể thực hiện các thao tác có độ chính xác cao. Khuyến nghị có thể sử dụng làm chiến lược luyện tập cho người mới, nhưng không phù hợp với các nhà giao dịch theo đuổi hiệu suất cao và tỷ lệ thắng cao. Nếu muốn đạt được hiệu quả giao dịch tốt hơn, cần tìm kiếm các chiến lược có khả năng dự đoán mạnh hơn.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1