Chiến lược xu hướng siêu Ichimoku

Tổng quan

Chiến lược Super Ichimoku là một chiến lược giao dịch xu hướng dựa trên chỉ báo Super Ichimoku để đưa ra quyết định giao dịch. Chiến lược này sử dụng mối quan hệ giữa đường chuyển đổi (Tenkan-sen), đường cơ sở (Kijun-sen) và đám mây (Kumo) của chỉ báo Super Ichimoku để xác định hướng xu hướng hiện tại, kết hợp với sự điều chỉnh giá để vào lệnh.

Chiến lược Super Ichimoku chủ yếu phù hợp cho giao dịch xu hướng trung và dài hạn, có thể thu lợi nhuận trong các xu hướng lớn. Chiến lược này cũng có khả năng nhận diện xu hướng mạnh mẽ.

Nguyên lý chiến lược

Chiến lược Super Ichimoku chủ yếu đánh giá các yếu tố sau để quyết định hướng giao dịch:

-

Mối quan hệ giữa đường chuyển đổi và đường cơ sở: Khi đường chuyển đổi ở trên thì xem xét tăng, ở dưới thì xem xét giảm.

-

Màu sắc của đám mây: Khi đám mây có màu xanh lá thì xem xét tăng, màu đỏ thì xem xét giảm.

-

Sự điều chỉnh giá: Cần giá quay trở lại bên ngoài đường chuyển đổi và đường cơ sở mới có thể vào lệnh.

Cụ thể, tín hiệu giao dịch của chiến lược như sau:

Tín hiệu mua (Long):

- Đường chuyển đổi cao hơn đường cơ sở

- Giá cao hơn đường chuyển đổi và đường cơ sở

- Đường chuyển đổi và đường cơ sở cao hơn đám mây

- Giá quay trở lại dưới đường chuyển đổi và đường cơ sở

Tín hiệu bán (Short):

- Đường chuyển đổi thấp hơn đường cơ sở

- Giá thấp hơn đường chuyển đổi và đường cơ sở

- Đường chuyển đổi và đường cơ sở thấp hơn đám mây

- Giá quay trở lại trên đường chuyển đổi và đường cơ sở

Khi đồng thời thỏa mãn tín hiệu mua/bán, sẽ thực hiện mở vị thế tùy theo tình trạng vị thế hiện tại.

Phân tích ưu điểm

Chiến lược Super Ichimoku có những ưu điểm sau:

-

Sử dụng tổ hợp chỉ báo Super Ichimoku để xác định hướng xu hướng, độ chính xác cao.

-

Đường chuyển đổi và đường cơ sở có thể xác định rõ ràng xu hướng ngắn và trung hạn, đám mây xác định xu hướng dài hạn.

-

Yêu cầu giá quay lại đường chuyển đổi, tránh được thua lỗ do phá vỡ giả.

-

Kiểm soát rủi ro bằng cách đặt stop loss dựa trên mức giá cao nhất và thấp nhất trong khoảng thời gian gần nhất, có thể kiểm soát hiệu quả tổn thất từng lệnh.

-

Tỷ lệ lợi nhuận/rủi ro hợp lý, hướng tới lợi nhuận ổn định.

-

Có thể áp dụng trên nhiều khung thời gian khác nhau, phù hợp với giao dịch xu hướng trung và dài hạn.

-

Tư duy chiến lược rõ ràng dễ hiểu, không gian tối ưu hóa tham số lớn.

-

Có thể hoạt động hiệu quả trong nhiều môi trường thị trường khác nhau.

Phân tích rủi ro

Chiến lược Super Ichimoku cũng tồn tại các rủi ro sau:

-

Trong thị trường đi ngang (sideway), stop loss có thể bị kích hoạt thường xuyên, ảnh hưởng đến hiệu quả lợi nhuận.

-

Khi xu hướng thay đổi nhanh chóng, không thể đảo chiều vị thế kịp thời, có thể dẫn đến thua lỗ.

-

Tỷ lệ lợi nhuận/rủi ro đặt ra không phù hợp với tất cả các sản phẩm, cần điều chỉnh tham số cho từng mục tiêu khác nhau.

-

Khi không gian tăng sau khi phá vỡ đám mây có hạn, lợi nhuận có thể bị hạn chế.

-

Các tham số chỉ báo cần được kiểm tra và tối ưu hóa nhiều lần, không phù hợp với các sản phẩm thường xuyên điều chỉnh tham số.

Có thể giảm rủi ro thông qua các phương pháp sau:

-

Tối ưu hóa tham số để phù hợp hơn với đặc điểm của các khung thời gian và sản phẩm khác nhau.

-

Kết hợp với các chỉ báo khác để lọc tín hiệu vào lệnh, tránh phá vỡ giả trong thị trường đi ngang.

-

Điều chỉnh vị trí stop loss một cách linh hoạt, giảm xác suất bị kích hoạt stop loss.

-

Kiểm tra các cài đặt tỷ lệ lợi nhuận/rủi ro khác nhau.

-

Sử dụng các phương pháp như mô hình biểu đồ để xác định mức độ mạnh yếu của tín hiệu xu hướng.

Hướng tối ưu hóa

Chiến lược Super Ichimoku có thể được tối ưu hóa từ các khía cạnh sau:

-

Tối ưu hóa tham số của đường chuyển đổi và đường cơ sở để phù hợp hơn với đặc tính của sản phẩm đang giao dịch.

-

Tối ưu hóa tham số của đám mây để đám mây xác định xu hướng dài hạn chính xác hơn.

-

Tối ưu hóa thuật toán stop loss, chẳng hạn như đặt stop loss dựa trên ATR hoặc stop loss động.

-

Kết hợp với các chỉ báo khác để lọc tín hiệu, thiết lập thêm nhiều điều kiện lọc, giảm xác suất vào lệnh sai.

-

Tối ưu hóa cài đặt tỷ lệ lợi nhuận/rủi ro để thích ứng với đặc điểm của chiến lược trên các sản phẩm và khung thời gian khác nhau.

-

Sử dụng phương pháp Martingale để quản lý vị thế, thích ứng với tần suất biến động thị trường khác nhau.

-

Sử dụng phương pháp học máy để tối ưu hóa tham số, đạt được độ ổn định cao hơn.

-

Thiết lập các khung thời gian giao dịch khác nhau, điều chỉnh theo đặc điểm của phiên đêm và phiên ngày.

Tổng kết

Nhìn chung, chiến lược Super Ichimoku là một chiến lược rất phù hợp cho giao dịch xu hướng trung và dài hạn. Nó có lợi thế rõ rệt trong việc sử dụng chỉ báo Super Ichimoku để xác định hướng xu hướng, đồng thời kết hợp với sự điều chỉnh giá để vào lệnh có thể tránh hiệu quả việc vào lệnh sai. Bằng cách tối ưu hóa cài đặt tham số, chiến lược có thể đạt được lợi nhuận ổn định trên nhiều sản phẩm và nhiều khung thời gian hơn. Chiến lược này vừa dễ hiểu, vừa có không gian tối ưu hóa lớn, phù hợp để sử dụng làm một trong những chiến lược cơ bản cho nghiên cứu và học tập chiến lược.

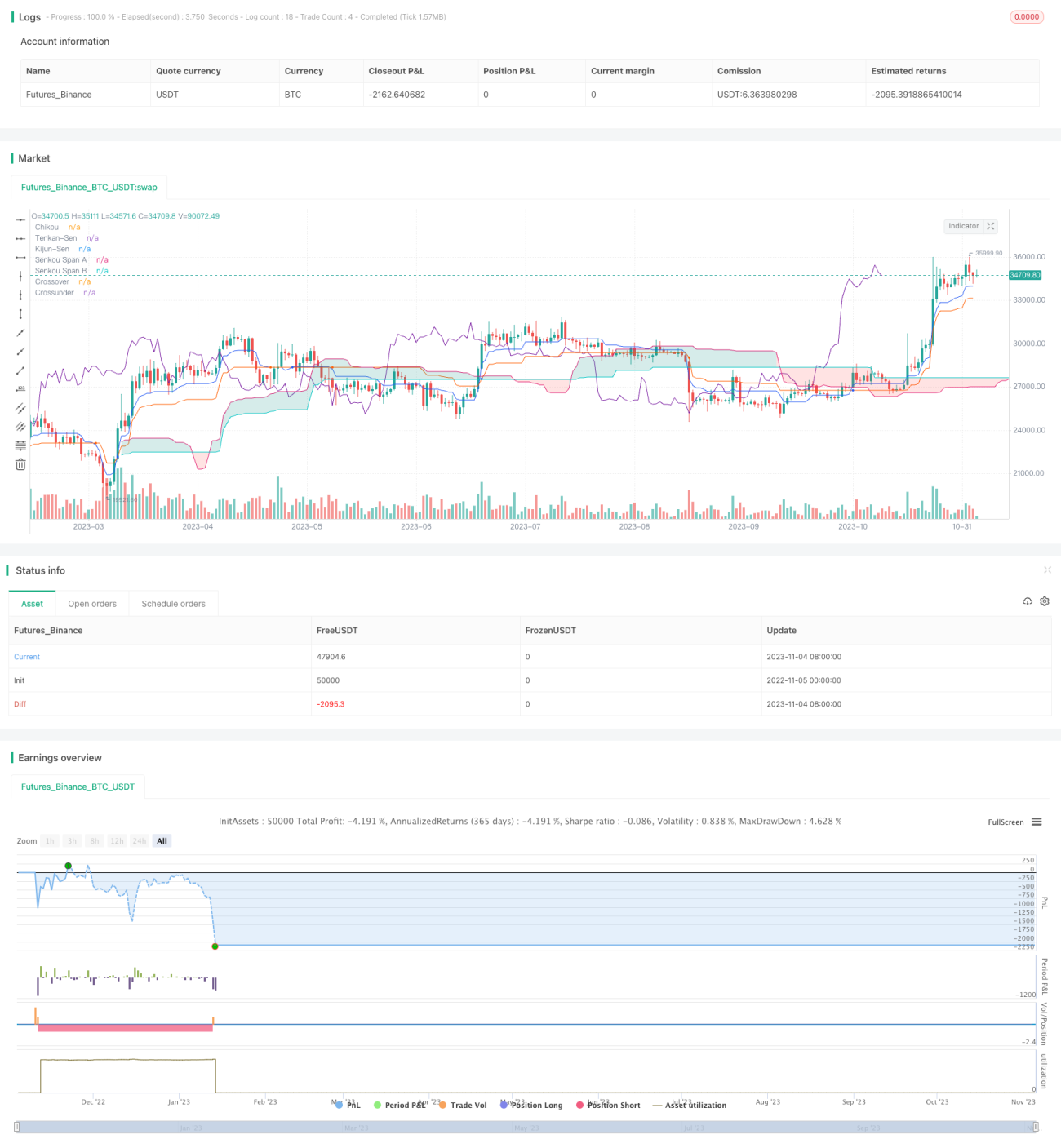

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1