Chiến lược định lượng theo xu hướng dựa trên SAR

Tổng quan

Chiến lược Khoảng cách đầu cơ là một chiến lược giao dịch định lượng theo xu hướng, sử dụng đường cong SAR trơn tru làm tín hiệu giao dịch chính, kết hợp với các bộ lọc phụ trợ như EMA, Động lượng nén và Dao động biến động để nhận diện điểm đảo chiều xu hướng thông qua việc cấu hình tham số SAR, thực hiện theo dõi xu hướng với rủi ro thấp. Đây là chiến lược rất phù hợp cho đầu tư trung và dài hạn.

Nguyên lý chiến lược

Chiến lược sử dụng Parabolic SAR làm chỉ báo tín hiệu giao dịch chính. SAR có thể đánh giá hiệu quả điểm đảo chiều của xu hướng giá; khi dấu hiệu SAR thay đổi, điều đó có nghĩa là xu hướng đã xoay chiều. Chiến lược này thường phát tín hiệu mua hoặc bán khi SAR đảo chiều.

Ngoài ra, chiến lược còn cung cấp tùy chọn Phá vỡ SAR. Tức là khi giá đã phá vỡ giá trị SAR cuối cùng trước khi SAR hoàn toàn đảo chiều, tín hiệu sẽ được tạo ra. Điều này có thể nâng cao độ nhạy của chiến lược.

Để lọc các tín hiệu giả, chiến lược còn giới thiệu ba bộ lọc phụ trợ: EMA, Động lượng nén và Dao động biến động, có thể sử dụng riêng lẻ hoặc kết hợp để xác nhận độ tin cậy của xu hướng giá và tín hiệu giao dịch.

Cuối cùng, chiến lược cung cấp ba phương thức dừng lỗ/chốt lời: dừng lỗ cố định, chốt lời cố định và dừng lỗ theo tỷ lệ rủi ro/lợi nhuận. Điều này cho phép chiến lược linh hoạt thích ứng với đặc điểm của các loại giao dịch khác nhau.

Phân tích ưu điểm

-

SAR có thể xác định chính xác sự đảo chiều của xu hướng giá và kịp thời nắm bắt xu hướng giá mới, phù hợp để theo dõi xu hướng trung và dài hạn.

-

Nhiều bộ lọc giúp giảm xác suất phá vỡ giả, nâng cao độ tin cậy của tín hiệu.

-

Cấu hình đơn giản và linh hoạt, có thể tùy chỉnh tham số để phù hợp với các loại giao dịch khác nhau.

-

Cung cấp nhiều phương thức chốt lời/dừng lỗ, có thể theo đuổi sự cân bằng giữa rủi ro và lợi nhuận.

-

Có thể kết nối trực tiếp với bot giao dịch, thực hiện giao dịch tự động.

Phân tích rủi ro

-

Trong thị trường không có xu hướng, có thể xuất hiện nhiều tín hiệu giả và giao dịch không hiệu quả.

-

Tham số SAR không phù hợp cũng sẽ ảnh hưởng đến độ chính xác của việc đánh giá tín hiệu.

-

Là chiến lược theo xu hướng, dễ dàng chạm mức dừng lỗ trong thị trường biến động mạnh.

Để đối phó với các rủi ro trên, có thể điều chỉnh tham số SAR hoặc tham số bộ lọc một cách phù hợp để giảm xác suất giao dịch không hiệu quả. Cũng có thể nới lỏng giới hạn dừng lỗ để chịu đựng biến động giá lớn hơn.

Hướng tối ưu hóa

-

Tối ưu hóa tham số SAR. Có thể tối ưu hóa tham số bước và gia số của SAR thông qua dữ liệu backtest lịch sử để có được chiến lược giao dịch ổn định và hiệu quả hơn.

-

Đưa vào các chỉ báo đánh giá xu hướng. Thêm các chỉ báo phụ trợ như MACD, DMI vào chiến lược để nâng cao khả năng đánh giá xu hướng.

-

Tối ưu hóa tỷ lệ rủi ro/lợi nhuận. Điều chỉnh tỷ lệ phần trăm chốt lời/dừng lỗ cố định và tỷ lệ rủi ro/lợi nhuận, chấp nhận rủi ro cao hơn một cách phù hợp để đạt được lợi nhuận cao hơn.

-

Thêm các loại ngoại hối. Hiện tại chiến lược chỉ hỗ trợ giao dịch tiền điện tử, có thể mở rộng hỗ trợ các loại ngoại hối, hàng hóa và thị trường chứng khoán.

Tổng kết

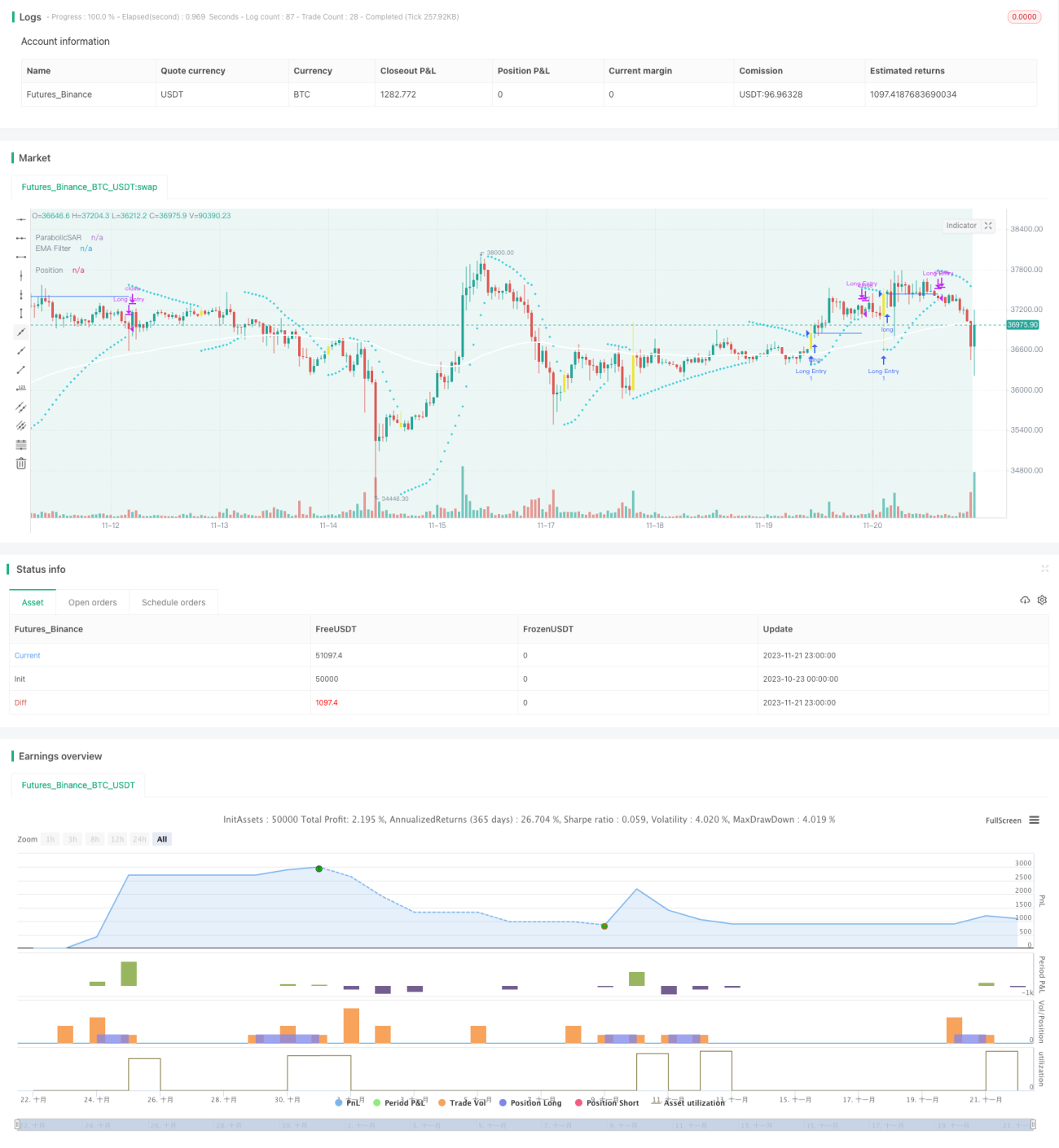

Khoảng cách đầu cơ là một chiến lược định lượng theo xu hướng rất thực tế. Nó phản ứng nhạy bén, tín hiệu đánh giá đáng tin cậy, thông qua quản lý chốt lời/dừng lỗ có thể đạt được lợi nhuận ổn định trong dài hạn. Việc tối ưu hóa tham số và quy tắc phù hợp có thể nâng cao hơn nữa hiệu quả của chiến lược. Đây là một chiến lược định lượng hiệu quả đáng sử dụng lâu dài.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1