Chiến lược giao dịch định lượng kết hợp xu hướng và dao động

Tổng quan

Chiến lược dao động hai xu hướng là một chiến lược giao dịch định lượng kết hợp giữa xu hướng và dao động. Nó sử dụng sự kết hợp của hai chỉ báo để xác định hướng và sức mạnh của xu hướng, đồng thời tìm kiếm thời điểm vào lệnh tốt hơn khi thị trường dao động.

Nguyên lý chiến lược

Chiến lược này chủ yếu sử dụng hai chỉ báo công khai: Trend Surfers và Mawreez's Trend Oscillator.

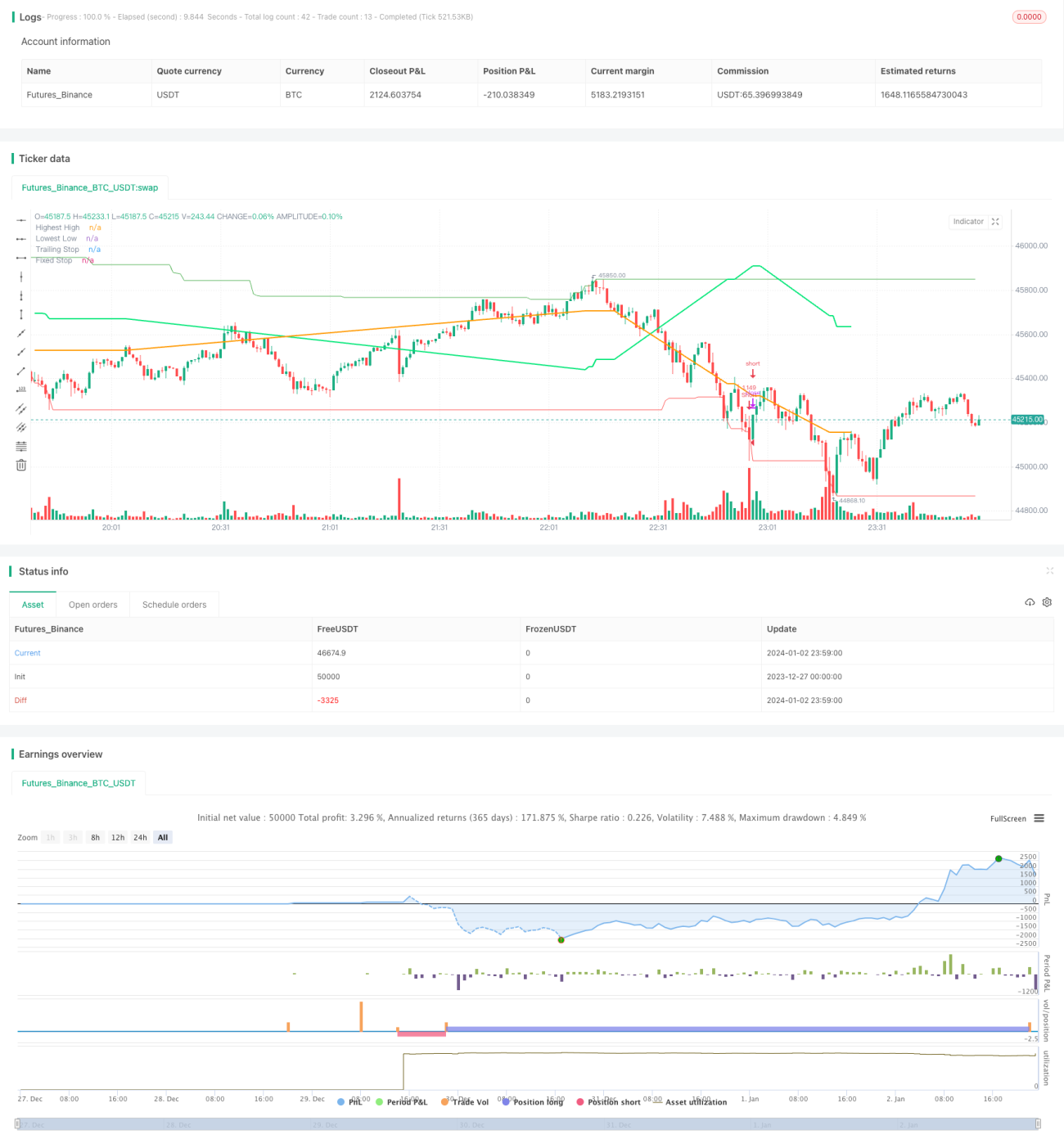

Trend Surfers là một chỉ báo dừng lỗ theo xu hướng. Nó tính toán giá cao nhất và thấp nhất trong một khoảng thời gian nhất định để đánh giá biến động giá và đưa ra vị trí dừng lỗ được đề xuất. Ví dụ, khi giá phá vỡ mức cao nhất của 168 nến gần nhất, đó là tín hiệu tăng giá; khi giá phá vỡ mức thấp nhất của 168 nến gần nhất, đó là tín hiệu giảm giá.

Mawreez's Trend Oscillator là một chỉ báo dao động hai đường. Nó tương tự MACD, sử dụng chênh lệch DI để xác định hướng và sức mạnh của xu hướng. Đường chỉ báo này ở trên mức 0 là tín hiệu tăng giá, dưới mức 0 là tín hiệu giảm giá.

Quy tắc giao dịch của chiến lược là:

Vào lệnh mua: Khi Trend Surfers phá vỡ đường cao nhất và chỉ báo Mawreez's Trend Oscillator là tín hiệu tăng giá.

Vào lệnh bán: Khi Trend Surfers phá vỡ đường thấp nhất và chỉ báo Mawreez's Trend Oscillator là tín hiệu giảm giá.

Phương pháp dừng lỗ là kết hợp dừng lỗ theo xu hướng và dừng lỗ cố định.

Phân tích ưu điểm

Chiến lược này kết hợp các chỉ báo xu hướng và dao động, vừa có thể bắt được xu hướng, vừa có thể tìm kiếm mức giá tốt hơn khi dao động, mang lại những ưu điểm sau:

- Bộ lọc kép chỉ báo, có thể tránh hiệu quả các phá vỡ giả.

- Kết hợp xu hướng và dao động, dễ nắm bắt cơ hội tích lũy ở vùng thấp trong biên độ dao động hoặc nhẹ nhàng tham gia ở vùng cao.

- Sử dụng nhiều phương pháp dừng lỗ, có thể kiểm soát rủi ro tốt.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Kết hợp hai chỉ báo dễ bỏ sót tín hiệu.

- Chỉ báo xu hướng và chỉ báo dao động có thể phát ra tín hiệu mâu thuẫn.

- Dừng lỗ cố định có thể dừng lỗ quá sớm.

Để đối phó với những rủi ro này, có thể áp dụng các biện pháp sau:

- Nới lỏng tham số chỉ báo một cách phù hợp, giảm tỷ lệ lọc.

- Thêm quy tắc xác định xu hướng, tránh xung đột chỉ báo.

- Điều chỉnh vị trí dừng lỗ linh hoạt.

Hướng tối ưu hóa

Chiến lược này còn có không gian tối ưu hóa thêm:

- Thử nghiệm các tổ hợp tham số và tham số chu kỳ khác nhau để tìm tham số tối ưu.

- Thêm các quy tắc hỗ trợ như biến động, khối lượng giao dịch, v.v.

- Sử dụng kỹ thuật học máy để tối ưu hóa động các chỉ báo và tham số.

Tổng kết

Chiến lược dao động hai xu hướng kết hợp ưu điểm của chỉ báo theo dõi xu hướng và dao động, vừa có thể nhận diện hướng xu hướng, vừa có thể nắm bắt cơ hội dao động. Thông qua tối ưu hóa tham số và quy tắc, có thể nâng cao hơn nữa khả năng sinh lời của chiến lược. Chiến lược này có triển vọng phát triển tốt.

- 1