Chiến lược bám xu hướng với chênh lệch đa cấp trên đường trung bình động

Tổng quan

Chiến lược này dựa trên độ lệch đa khung thời gian của đường trung bình động, theo dõi xu hướng trung và dài hạn, áp dụng mô hình truy đuổi theo cấp độ vị thế, nhằm đạt được sự tăng trưởng theo cấp số nhân của vốn. Ưu điểm lớn nhất của chiến lược là có thể nắm bắt xu hướng trung và dài hạn, thực hiện truy đuổi theo từng đợt và từng giai đoạn, từ đó thu được lợi nhuận vượt trội.

Nguyên lý chiến lược

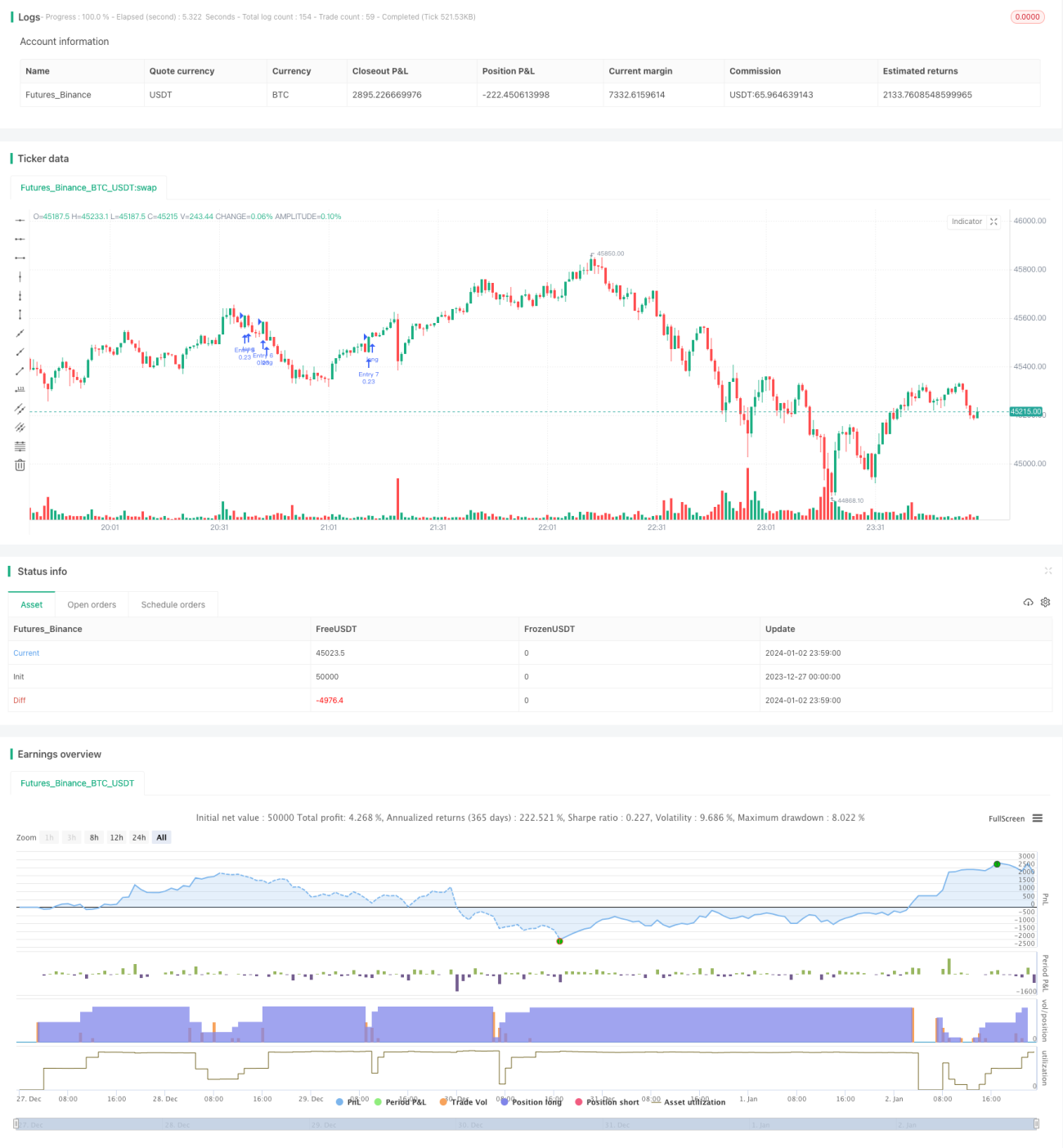

- Xây dựng khung thời gian đa tầng dựa trên đường trung bình động 9 ngày, 100 ngày và 200 ngày.

- Khi đường trung bình động chu kỳ ngắn vượt lên trên đường trung bình động chu kỳ dài từ dưới lên, tín hiệu mua được phát sinh.

- Áp dụng mô hình truy đuổi theo 7 cấp độ vị thế, mỗi lần mở vị thế mới sẽ kiểm tra xem các vị thế trước đó đã đầy chưa, nếu đã có 6 vị thế thì không tăng thêm vị thế nữa.

- Mỗi vị thế đặt mức chốt lời và cắt lỗ cố định là 3%, để kiểm soát rủi ro.

Trên đây là logic giao dịch cơ bản của chiến lược này.

Ưu điểm của chiến lược

- Có thể nắm bắt hiệu quả xu hướng trung và dài hạn, tận hưởng tối đa sự tăng trưởng theo cấp số nhân của thị trường.

- Sử dụng đường trung bình động đa chu kỳ thời gian để tạo độ lệch, giúp tránh bị nhiễu bởi tiếng ồn thị trường ngắn hạn.

- Thiết lập điểm chốt lời và cắt lỗ cố định, kiểm soát hiệu quả rủi ro của từng vị thế.

- Áp dụng mô hình truy đuổi theo cấp độ, xây dựng vị thế theo từng đợt, có thể nắm bắt cơ hội xu hướng và đạt được lợi nhuận vượt trội.

Rủi ro của chiến lược và giải pháp

- Có rủi ro bị kết thúc. Nếu thị trường đảo chiều, không thể kịp thời cắt lỗ thoát ra, có thể đối mặt với thua lỗ lớn. Giải pháp là rút ngắn chu kỳ đường trung bình động, tăng tốc độ cắt lỗ.

- Có rủi ro về vị thế. Nếu sự kiện bất ngờ gây thua lỗ vượt quá phạm vi chịu đựng, sẽ đối mặt với rủi ro ký quỹ bổ sung hoặc cháy tài khoản. Giải pháp là giảm tỷ lệ vị thế ban đầu một cách thích hợp.

- Có rủi ro thua lỗ quá lớn. Nếu thị trường giảm mạnh, truy đuổi theo cấp độ chuyển sang xu hướng giảm, có thể thua lỗ lên tới hơn 700%. Giải pháp là tăng tỷ lệ cắt lỗ cố định, tăng tốc độ cắt lỗ.

Hướng tối ưu hóa chiến lược

- Có thể thử nghiệm các tổ hợp tham số đường trung bình động khác nhau để tìm ra tham số tối ưu hơn.

- Có thể tối ưu hóa số lượng vị thế xây dựng. Thử nghiệm các số lượng vị thế cấp độ khác nhau để tìm ra giải pháp tối ưu.

- Có thể thử nghiệm cài đặt cắt lỗ và chốt lời cố định. Mở rộng hợp lý phạm vi chốt lời để theo đuổi tỷ suất lợi nhuận cao hơn.

Tổng kết

Nhìn chung, chiến lược này rất phù hợp để bắt xu hướng trung và dài hạn của thị trường, sử dụng phương pháp truy đuổi theo từng đợt và từng giai đoạn, có thể đạt được lợi nhuận vượt trội với tỷ lệ lợi nhuận/rủi ro rất cao. Đồng thời cũng tồn tại một số rủi ro vận hành nhất định, cần được kiểm soát thông qua việc điều chỉnh các tham số và các phương pháp khác, tìm ra sự cân bằng giữa lợi nhuận và rủi ro. Nhìn chung, chiến lược này rất đáng để kiểm chứng thực tế, điều chỉnh và tối ưu hóa thêm dựa trên kết quả thực tế.

- 1