Chiến lược ngắn hạn giao cắt DEMA và EMA kết hợp với độ biến động ATR

I. Tổng quan chiến lược

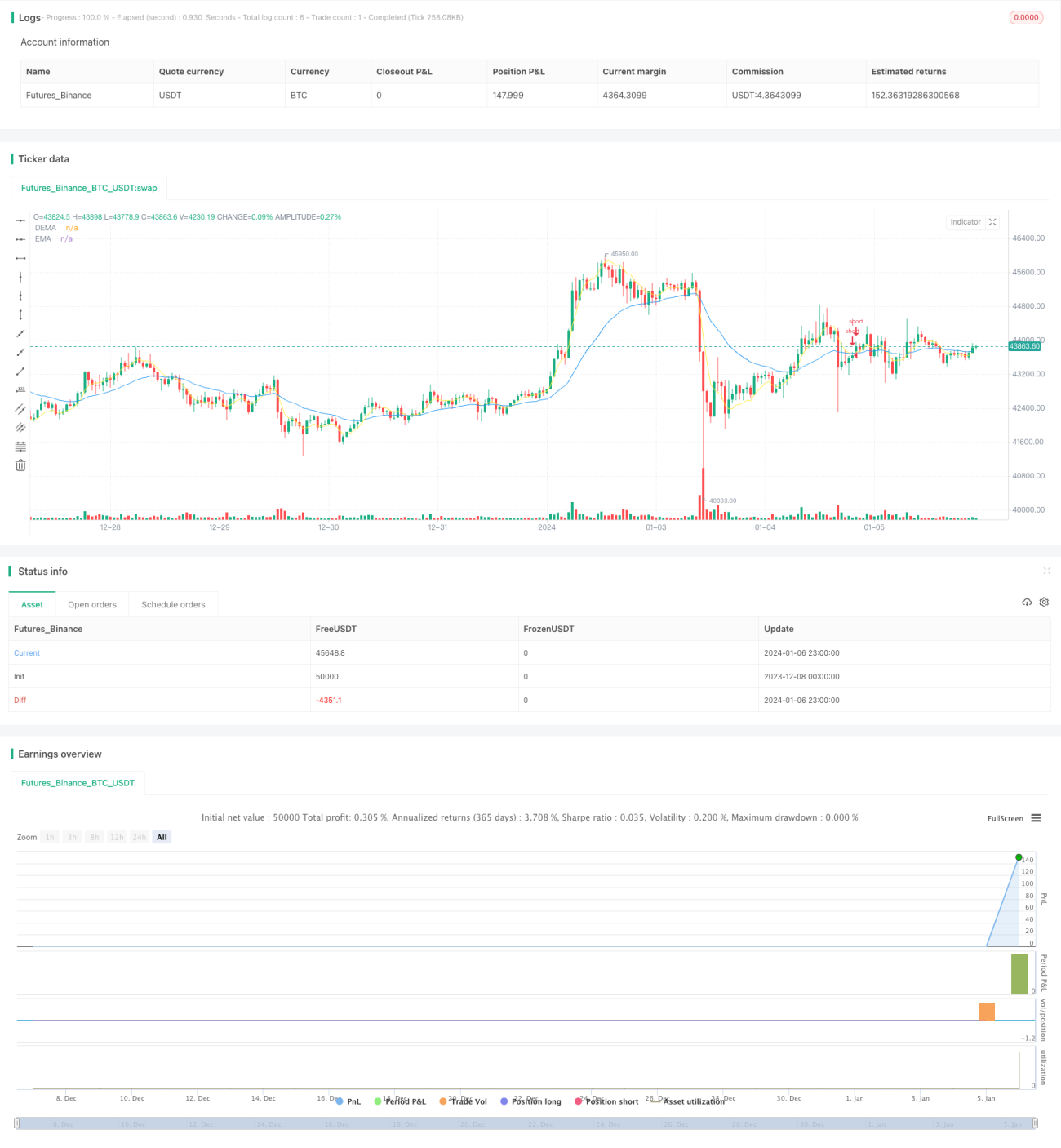

Chiến lược này có tên là "Chiến lược kết hợp giao cắt ngắn hạn DEMA và EMA với biến động ATR". Chiến lược sử dụng tín hiệu giao cắt giữa DEMA và EMA, kết hợp chỉ báo biến động ATR, để thực hiện chiến lược giao dịch ngắn hạn hiệu quả. Khi DEMA cắt xuống dưới EMA và biến động ATR tăng lên, sẽ mở vị thế bán khống; khi DEMA lại cắt lên trên EMA, sẽ đóng vị thế.

II. Nguyên lý chiến lược

-

Tính chỉ báo DEMA. DEMA là đường trung bình động kép EMA, bằng cách tính toán hai EMA trong một khoảng thời gian nhất định, có thể lọc hiệu quả nhiễu thị trường ngắn hạn, nâng cao độ chính xác của tín hiệu.

-

Tính chỉ báo EMA. EMA là đường trung bình động hàm mũ, có thể phản ứng nhanh hơn với sự thay đổi giá.

-

Tính biến động ATR. ATR là chỉ báo về phạm vi dao động thực, phản ánh mức độ biến động và rủi ro của thị trường. Khi ATR tăng, thị trường biến động mạnh hơn, dễ hình thành điều chỉnh ngắn hạn.

-

Khi DEMA cắt xuống dưới EMA và biến động ATR lớn hơn tham số đã đặt, cho thấy giá cổ phiếu bắt đầu giảm, thị trường risk off, lúc này thực hiện bán khống.

-

Khi DEMA lại cắt lên trên EMA, cho thấy giá hình thành hỗ trợ và bắt đầu bật tăng, lúc này đóng vị thế.

III. Lợi thế của chiến lược

-

Kết hợp hai đường EMA với EMA giúp nâng cao độ chính xác của tín hiệu.

-

Chỉ báo biến động ATR có thể loại bỏ các tín hiệu whipsaw rủi ro thấp.

-

Giao dịch ngắn hạn, phù hợp cho việc bám đuổi ngắn hạn, tránh phải phòng ngừa dài hạn.

-

Logic giao dịch đơn giản, rõ ràng, dễ hiểu và dễ thực hiện.

IV. Rủi ro của chiến lược

-

Cài đặt tham số ATR không phù hợp có thể bỏ lỡ cơ hội giao dịch.

-

Cần theo dõi đồng thời tín hiệu cả hai phía, mức độ khó khi thao tác cao hơn.

-

Bị ảnh hưởng bởi biến động thị trường ngắn hạn.

Cách khắc phục: Kiểm tra tối ưu hóa tham số, điều chỉnh tham số; đơn giản hóa logic giao dịch, chỉ tập trung vào tín hiệu một phía; nới lỏng phạm vi dừng lỗ phù hợp.

V. Hướng tối ưu hóa chiến lược

-

Tối ưu hóa tham số của DEMA và EMA, tìm tổ hợp tham số tốt nhất.

-

Tối ưu hóa tham số chu kỳ của ATR, xác định chỉ báo đo lường biến động thị trường tối ưu.

-

Thêm các chỉ báo phụ trợ khác, như kênh BOLL, để nâng cao độ chính xác tín hiệu.

-

Bổ sung quy tắc dừng lỗ và chốt lời, khóa lợi nhuận ổn định hơn.

VI. Tổng kết

Chiến lược này, thông qua giao cắt DEMA, EMA và chỉ báo biến động ATR, xây dựng một chiến lược giao dịch ngắn hạn đơn giản và hiệu quả. Logic giao dịch của chiến lược rõ ràng, dễ thao tác, có thể thích ứng với giao dịch ngắn hạn tần suất cao. Bước tiếp theo, thông qua tối ưu hóa tham số và tối ưu hóa quy tắc, có thể đạt được lợi nhuận vượt trội ổn định hơn.

- 1