Chiến lược kim tự tháp hai chiều giao dịch cổ phiếu dựa trên chỉ báo RSI

Tổng quan

Bài viết này chủ yếu giới thiệu một chiến lược giao dịch kim tự tháp hai chiều dựa trên chỉ số sức mạnh tương đối (RSI). Chiến lược này sử dụng chỉ số RSI để xác định vùng quá mua/quá bán của cổ phiếu, kết hợp với nguyên lý gia tăng vị thế kim tự tháp để đạt được lợi nhuận.

Nguyên lý chiến lược

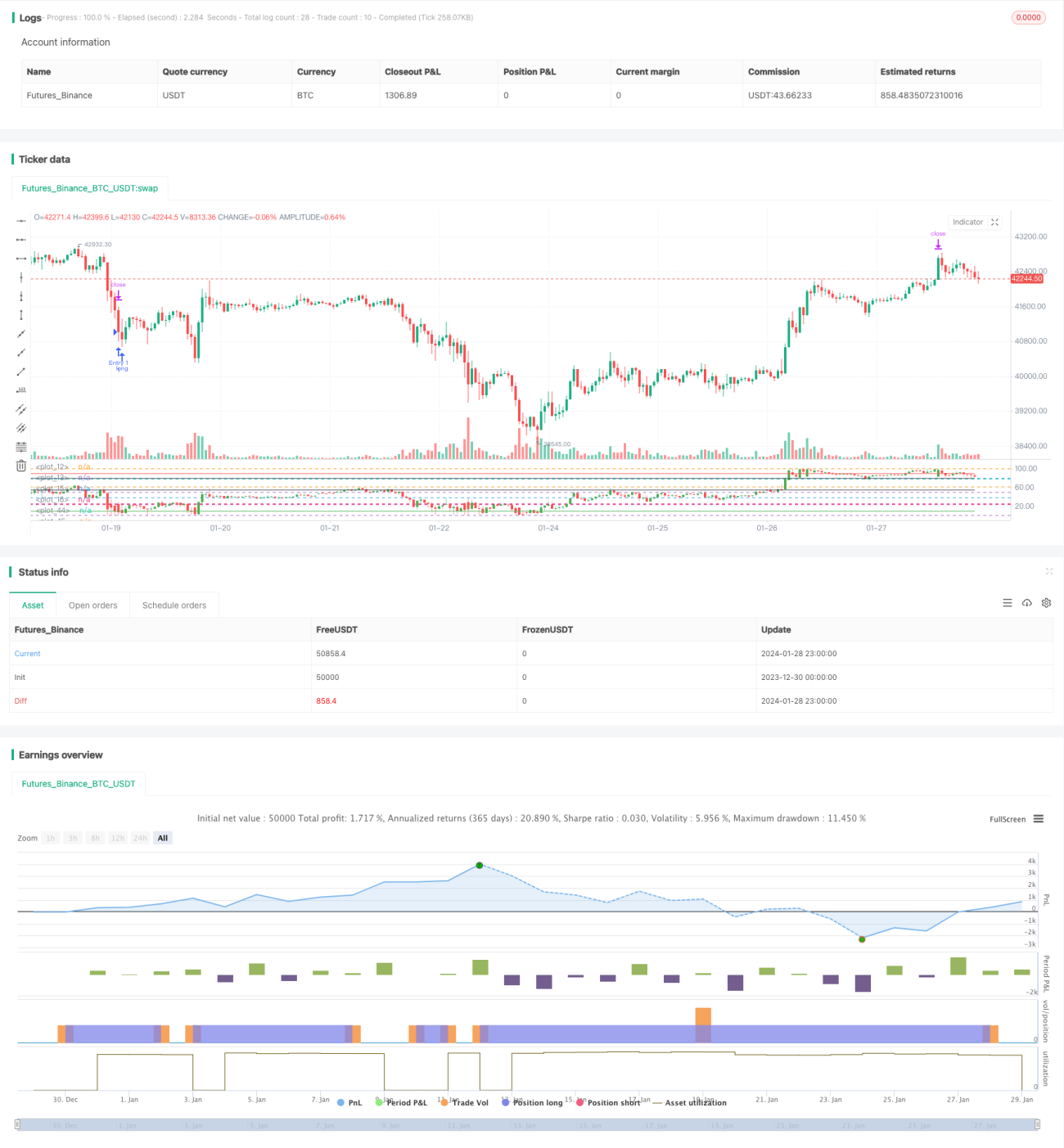

- Sử dụng chỉ số RSI để xác định xem cổ phiếu có đi vào vùng quá mua/quá bán hay không. Khi RSI dưới 25 là quá bán, trên 80 là quá mua.

- Khi RSI đi vào vùng quá bán, bắt đầu vào lệnh mua (long). Khi RSI đi vào vùng quá mua, bắt đầu vào lệnh bán (short).

- Áp dụng phương pháp gia tăng vị thế kim tự tháp, tối đa 7 lần. Sau mỗi lần gia tăng, thiết lập điểm chốt lời và cắt lỗ.

Phân tích ưu điểm

- Sử dụng chỉ số RSI để xác định vùng quá mua/quá bán, có thể nắm bắt các cơ hội đảo chiều giá lớn.

- Phương pháp gia tăng vị thế kim tự tháp có thể đạt được tỷ suất lợi nhuận tốt hơn khi xu hướng đúng.

- Thiết lập điểm chốt lời và cắt lỗ sau mỗi lần gia tăng giúp kiểm soát rủi ro.

Phân tích rủi ro

- Hiệu quả xác định quá mua/quá bán của chỉ số RSI không ổn định, có thể xuất hiện tín hiệu sai.

- Cần thiết lập số lần gia tăng hợp lý, gia tăng quá nhiều sẽ làm tăng rủi ro.

- Việc thiết lập điểm cắt lỗ cần xem xét biến động, không thể đặt quá nhỏ.

Hướng tối ưu

- Có thể xem xét kết hợp các chỉ số khác để lọc tín hiệu RSI, nâng cao độ chính xác trong việc xác định quá mua/quá bán, ví dụ như phối hợp với KDJ, BOLL, v.v.

- Có thể thiết lập cắt lỗ thả nổi để theo dõi giá, điều chỉnh linh hoạt dựa trên biến động và yêu cầu kiểm soát rủi ro.

- Có thể xem xét sử dụng tham số thích ứng dựa trên tình trạng thị trường (thị trường bò, thị trường gấu, v.v.).

Tổng kết

Chiến lược này kết hợp chỉ số RSI với chiến lược gia tăng vị thế kim tự tháp, vừa xác định quá mua/quá bán vừa có thể thu được nhiều lợi nhuận hơn thông qua việc gia tăng vị thế. Mặc dù độ chính xác của việc xác định RSI cần được cải thiện, nhưng thông qua tối ưu hóa tham số hợp lý và kết hợp với các chỉ số khác, có thể hình thành một chiến lược giao dịch hiệu quả ổn định. Chiến lược này có tính phổ quát nhất định, là một phương pháp giao dịch định lượng tương đối đơn giản và trực tiếp.

- 1