Chiến lược giao dịch ADX hai chiều

Tổng quan

Chiến lược giao dịch ADX hai chiều là một chiến lược định lượng sử dụng chỉ số Định hướng Trung bình (ADX) để thực hiện giao dịch hai chiều. Chiến lược này tính toán chênh lệch giữa chỉ số ADX và chỉ số DIPlus và DIMinus, thiết lập ngưỡng để xác định xem có tín hiệu giao dịch hay không, thực hiện giao dịch mua và bán để tạo lợi nhuận.

Nguyên lý chiến lược

- Tính phạm vi biến động thực (True Range)

- Tính chuyển động hướng lên (Directional Movement Plus) và chuyển động hướng xuống (Directional Movement Minus)

- Tính phạm vi biến động thực được làm mịn (Smoothed True Range)

- Tính chuyển động hướng lên được làm mịn (Smoothed Directional Movement Plus) và chuyển động hướng xuống được làm mịn (Smoothed Directional Movement Minus)

- Tính các chỉ số DIPlus, DIMinus và ADX

- Tính chênh lệch giữa DIPlus và ADX, DIMinus và ADX

- Thiết lập ngưỡng chênh lệch cho giao dịch mua và bán

- Khi chênh lệch lớn hơn ngưỡng, xác định tín hiệu giao dịch được tạo ra

- Tạo lệnh mua và lệnh bán

Cốt lõi của chiến lược này là sử dụng các chỉ số động lượng như ADX để đánh giá hướng và cường độ xu hướng, kết hợp với quy tắc xác định chênh lệch để thiết lập ngưỡng và thực hiện giao dịch tự động.

Phân tích ưu điểm

- Sử dụng ADX để xác định hướng xu hướng, có thể bắt kịp xu hướng thị trường một cách chính xác

- Áp dụng quy tắc xác định chênh lệch, có thể lọc hiệu quả các tín hiệu giả

- Giao dịch hai chiều, có thể tận dụng tối đa cơ hội mua và bán

- Giao dịch hoàn toàn tự động, không cần can thiệp thủ công

- Logic chiến lược rõ ràng, dễ hiểu và dễ sửa đổi

Phân tích rủi ro

- Chỉ số ADX có độ trễ, có thể bỏ lỡ các điểm đảo chiều xu hướng

- Rủi ro giao dịch hai chiều tăng lên, thua lỗ có thể mở rộng

- Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá mức

- Dữ liệu backtest không thể đại diện cho thị trường thực, rủi ro thực tế vẫn tồn tại

Giải pháp:

- Kết hợp các chỉ báo khác để xác nhận tín hiệu giao dịch

- Tối ưu hóa tham số, kiểm soát tần suất giao dịch

- Quản lý khối lượng vị thế (Position Sizing) một cách chặt chẽ

Hướng tối ưu hóa

- Tối ưu hóa tham số ADX, cải thiện độ nhạy của nó

- Thêm các chỉ báo khác để lọc tín hiệu

- Áp dụng thuật toán học máy để tối ưu hóa tham số

- Sử dụng chiến lược dừng lỗ nâng cao để kiểm soát rủi ro thua lỗ

- Kết hợp dự đoán mô hình để có được tín hiệu giao dịch chính xác hơn

Tổng kết

Chiến lược giao dịch ADX hai chiều nhìn chung là một chiến lược định lượng rất thực tế. Nó sử dụng chỉ số ADX để đánh giá xu hướng và bắt cơ hội giao dịch hai chiều. Đồng thời áp dụng quy tắc xác định chênh lệch để đảm bảo hiệu lực của tín hiệu. Chiến lược này có logic rõ ràng, đơn giản, dễ sửa đổi và tối ưu hóa, là một chiến lược giao dịch theo xu hướng hai chiều. Thông qua tối ưu hóa tham số hợp lý, áp dụng chiến lược dừng lỗ và lọc tín hiệu, có thể tăng cường thêm tính ổn định và khả năng sinh lời của chiến lược.

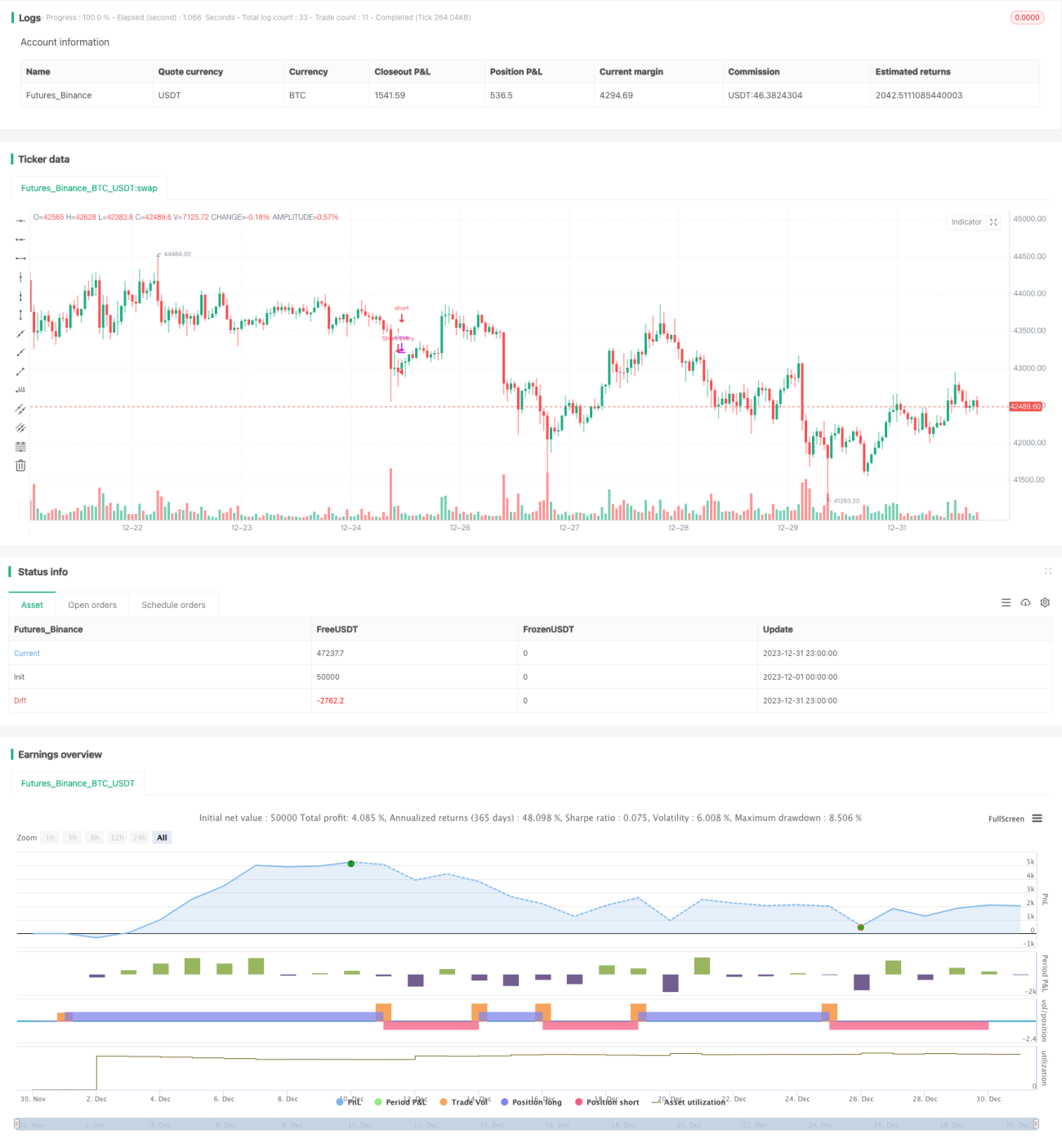

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1