Chiến lược giao dịch đa khung thời gian với đường trung bình động kép

Tổng quan

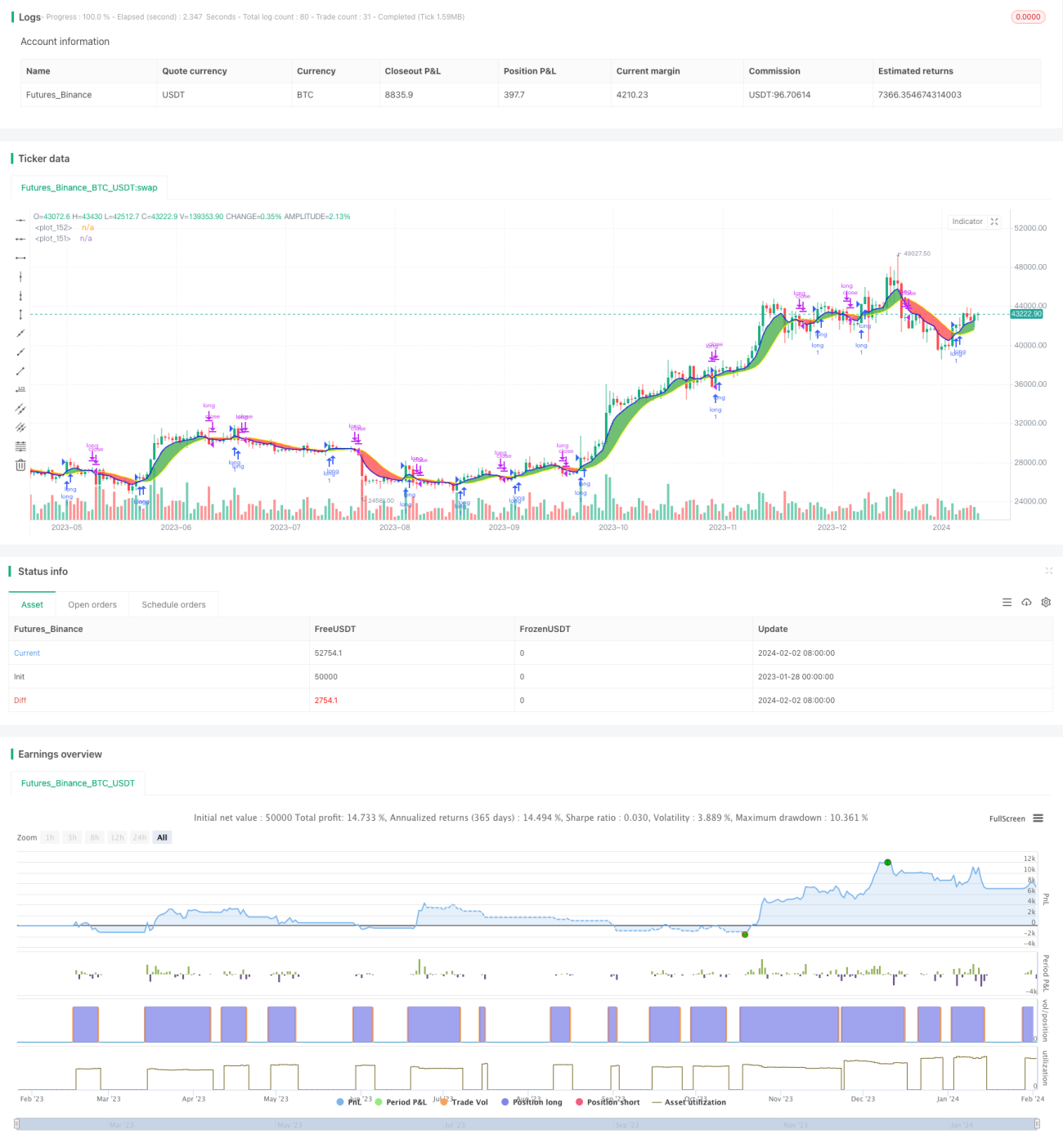

Chiến lược này tạo ra tín hiệu mua và bán trên hai khung thời gian khác nhau bằng cách tính toán hai đường trung bình động thuộc các loại khác nhau. Đây là một chiến lược sandbox rất tốt để thử nghiệm các loại đường trung bình động khác nhau cũng như các kết hợp khung thời gian khác nhau.

Nguyên lý chiến lược

Chiến lược này sử dụng hai đường trung bình động: một đường trung bình động nhanh và một đường trung bình động chậm. Khung thời gian của đường trung bình động nhanh phải lớn hơn hoặc bằng khung thời gian của biểu đồ. Khi đường trung bình động nhanh vượt lên trên đường trung bình động chậm, tín hiệu mua được tạo ra; khi đường trung bình động nhanh cắt xuống dưới đường trung bình động chậm, tín hiệu bán được tạo ra.

Người dùng có thể chọn nhiều loại đường trung bình động khác nhau như SMA, EMA, KAMA, v.v., và khung thời gian có thể khác nhau, nhờ đó có thể thử nghiệm các kết hợp để tìm ra tham số tối ưu.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là có thể dễ dàng điều chỉnh tham số và thử nghiệm các kết hợp khác nhau để tìm ra cài đặt tham số tối ưu.

Người dùng có thể tự do lựa chọn loại, độ dài thời gian và khung thời gian của hai đường trung bình động; hệ thống sẽ tính toán và hiển thị kết quả theo thời gian thực. Điều này dễ dàng hơn nhiều so với việc kiểm tra từng kết hợp tham số riêng lẻ.

Hơn nữa, chiến lược đã tích hợp sẵn chức năng cắt lỗ và chốt lời, giúp giảm rủi ro và tăng xác suất sinh lời.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này là việc cài đặt tham số không phù hợp có thể dẫn đến quá nhiều tín hiệu giao dịch, từ đó làm tăng chi phí giao dịch và tổn thất do trượt giá.

Ngoài ra, bản thân hai đường trung bình động dễ tạo ra tín hiệu giả; nếu tham số chọn không đúng, tín hiệu mua bán có thể không đáng tin cậy.

Những rủi ro này có thể được giảm nhẹ bằng cách tối ưu hóa tham số và kết hợp các chỉ báo khác.

Hướng tối ưu hóa

Có thể cân nhắc thêm các chỉ báo khác vào nền tảng hai đường trung bình động để lọc tín hiệu, ví dụ như chỉ báo RSI để xác nhận tín hiệu mua bán, từ đó giảm tín hiệu giả.

Ngoài ra, có thể thử nghiệm huấn luyện và tối ưu hóa tham số của đường trung bình động để tìm ra bộ tham số tốt nhất. Cũng có thể xem xét sử dụng phương pháp học máy để tối ưu hóa tham số một cách linh hoạt.

Tổng kết

Chiến lược này là một sandbox thử nghiệm hai đường trung bình động rất tốt. Ưu điểm của nó nằm ở khả năng lặp lại nhanh chóng các kết hợp tham số khác nhau để tìm ra chiến lược giao dịch tối ưu. Tất nhiên, cũng tồn tại một số rủi ro do cài đặt tham số không phù hợp, cần phải giảm thiểu bằng cách thêm các chỉ báo khác để lọc. Nếu tiếp tục tối ưu hóa chiến lược này, rất có thể sẽ đạt được hiệu quả giao dịch tốt hơn.

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.- 1