Chiến lược giao dịch đảo chiều Bollinger Bands + RSI + ADX + ATR

Tổng quan

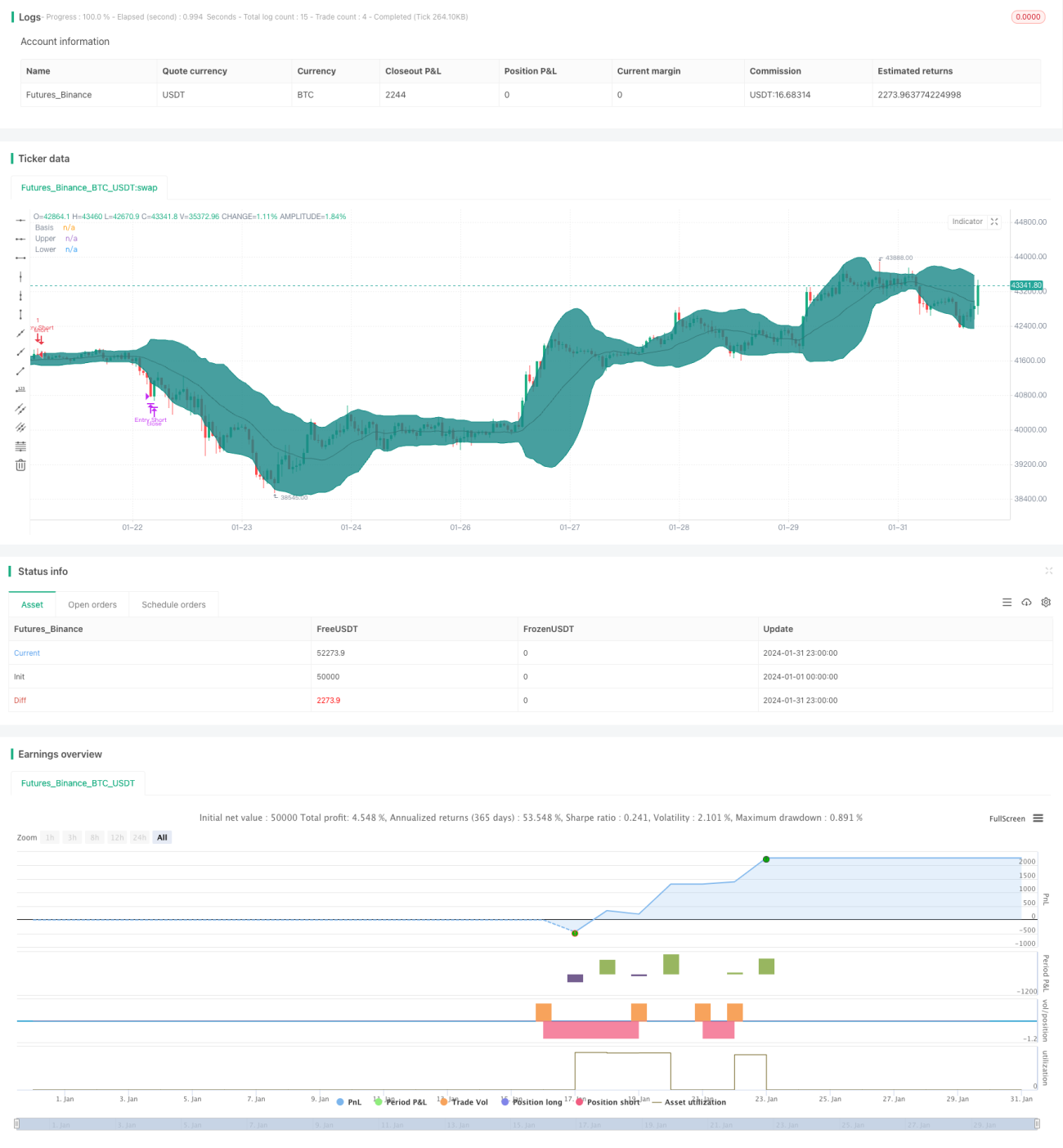

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật, khi chỉ báo Bollinger Band phát ra tín hiệu đảo chiều giá, kết hợp với các chỉ báo RSI, ADX và ATR để đánh giá cấu trúc thị trường, tìm kiếm cơ hội giao dịch đảo chiều có xác suất cao.

Nguyên lý chiến lược

-

Sử dụng Bollinger Band chu kỳ 20, khi giá chạm dải trên hoặc dải dưới, chờ tín hiệu mua/bán từ nến đảo chiều.

-

Chỉ báo RSI đánh giá thị trường có đang dao động hay không, RSI trên 60 là vùng tăng giá, dưới 40 là vùng giảm giá.

-

ADX dưới 20 cho thấy thị trường đang dao động, trên 20 cho thấy thị trường đang có xu hướng.

-

Cài đặt stop loss bằng ATR và trailing stop.

-

Kết hợp đường EMA để lọc tín hiệu.

Ưu điểm của chiến lược

-

Kết hợp nhiều chỉ báo, tạo tín hiệu giao dịch có xác suất cao.

-

Các tham số có thể tùy chỉnh, thích ứng với các điều kiện thị trường khác nhau.

-

Quy tắc stop loss chặt chẽ, kiểm soát rủi ro hiệu quả.

Rủi ro của chiến lược

-

Cài đặt tham số không phù hợp có thể dẫn đến giao dịch quá thường xuyên.

-

Xác suất đảo chiều thất bại vẫn tồn tại.

-

Trailing stop có thể không hiệu quả trong một số thị trường cụ thể.

Hướng tối ưu hóa

-

Kiểm tra thêm nhiều tổ hợp chỉ báo để tìm cấu hình tham số phù hợp hơn.

-

Nhận biết kịp thời cơ hội đảo chiều tiếp theo sau khi phá vỡ thất bại.

-

Thử nghiệm các phương pháp stop loss khác nhau để stop loss thông minh hơn.

Tổng kết

Chiến lược này sử dụng Bollinger Band làm tín hiệu giao dịch cơ bản, đồng thời kết hợp nhiều chỉ báo phụ trợ tạo thành hệ thống lọc có xác suất cao, quy tắc stop loss cũng khá đầy đủ. Thông qua điều chỉnh tham số và tối ưu hóa chỉ báo, vẫn có thể nâng cao hiệu suất của chiến lược. Nhìn chung, chiến lược này hình thành một hệ thống giao dịch đảo chiều đáng tin cậy.

- 1