Chiến lược cân bằng kiểm soát tâm lý giao dịch

Tổng quan

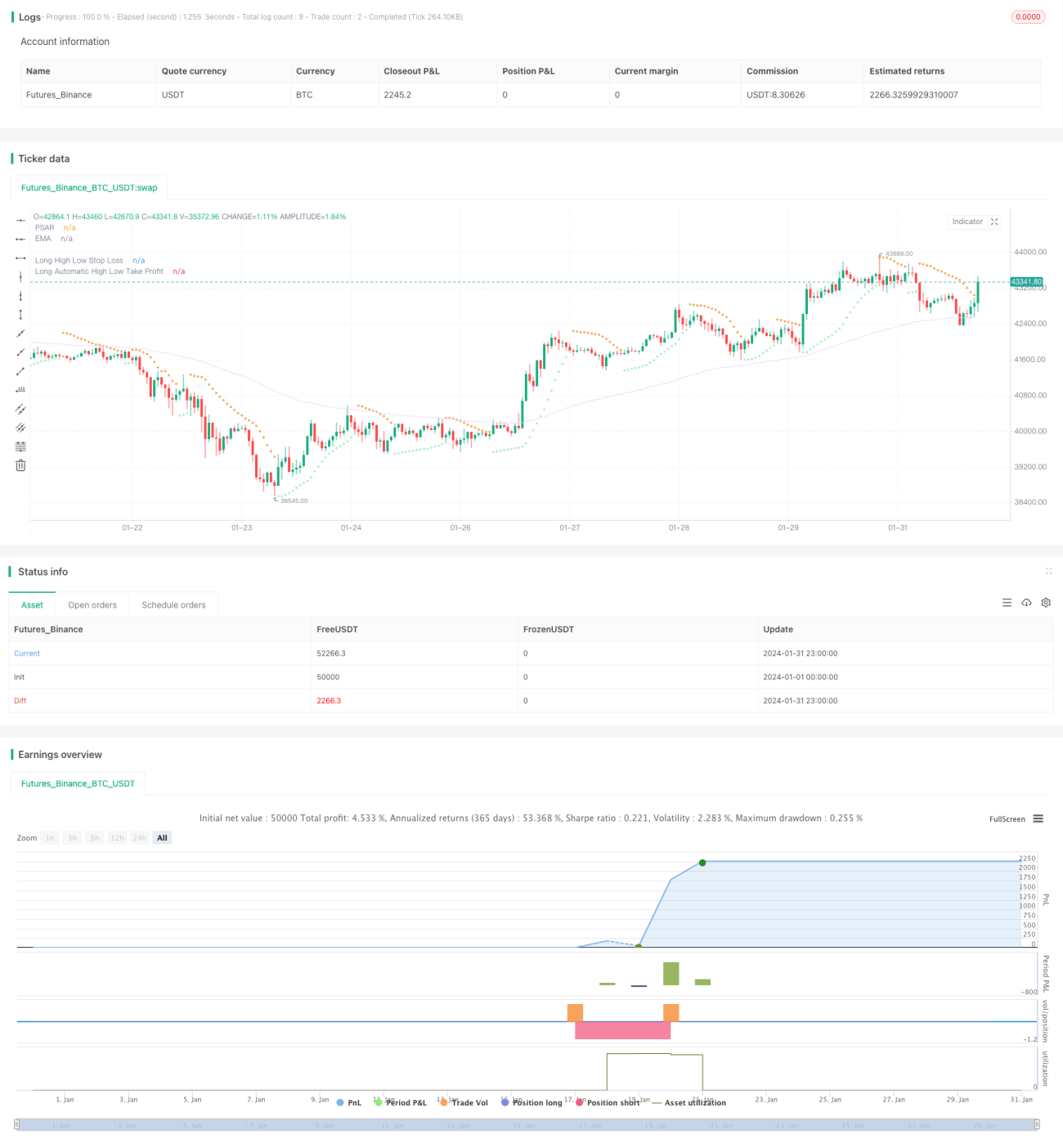

Mục đích của chiến lược này là cân bằng tâm lý giao dịch và hiệu suất giao dịch thông qua việc thiết lập các tham số khác nhau, nhằm đạt được lợi nhuận ổn định hơn. Chiến lược sử dụng các chỉ báo như đường trung bình động (MA), Bollinger Bands, Kênh Keltner để xác định xu hướng thị trường và biến động, kết hợp chỉ báo PSAR để xác định tín hiệu đảo chiều, và chỉ báo TTM Squeeze để đánh giá động lượng. Tín hiệu giao dịch được tạo ra từ sự kết hợp của các chỉ báo này. Đồng thời, chiến lược quản lý rủi ro bằng cách sử dụng phương pháp cắt lỗ dựa trên mức cao/thấp và chốt lời theo tỷ lệ rủi ro-lợi nhuận.

Nguyên lý chiến lược

Logic chính của chiến lược này như sau:

- Xác định xu hướng: Sử dụng đường EMA để đánh giá hướng xu hướng giá. Giá nằm trên EMA là xu hướng tăng, dưới EMA là xu hướng giảm.

- Xác định đảo chiều: Sử dụng PSAR để xác định điểm đảo chiều giá. Khi điểm PSAR xuất hiện phía trên giá là tín hiệu tăng, khi xuất hiện phía dưới giá là tín hiệu giảm.

- Xác định động lượng: Sử dụng chỉ báo TTM Squeeze để đánh giá biến động và động lượng thị trường. Chỉ báo TTM Squeeze đo lường biến động bằng cách so sánh độ rộng của Bollinger Bands và Kênh Keltner. Squeeze (siết chặt) có nghĩa là biến động rất thấp. Khi Squeeze được giải phóng (squeeze release) cho thấy biến động tăng và giá sắp có sự dịch chuyển hướng mạnh.

- Tạo tín hiệu giao dịch: Khi giá cắt lên trên đường EMA và điểm PSAR, đồng thời chỉ báo TTM Squeeze giải phóng squeeze, tạo tín hiệu mua (bullish). Khi giá cắt xuống dưới đường EMA và điểm PSAR, đồng thời chỉ báo TTM Squeeze bước vào squeeze, tạo tín hiệu bán (bearish).

- Phương pháp cắt lỗ: Sử dụng cắt lỗ dựa trên mức cao/thấp. Lấy giá cao nhất hoặc thấp nhất trong một chu kỳ gần đây nhân với hệ số đã thiết lập làm điểm cắt lỗ.

- Phương pháp chốt lời: Sử dụng chốt lời tự động dựa trên tỷ lệ rủi ro-lợi nhuận. Tỷ lệ giữa điểm cắt lỗ và giá hiện tại nhân với tham số tỷ lệ rủi ro-lợi nhuận đã thiết lập để có điểm chốt lời.

Thông qua việc thiết lập tham số, có thể kiểm soát tần suất giao dịch, quản lý vị thế, điểm cắt lỗ và điểm chốt lời, cân bằng tâm lý giao dịch.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Sử dụng nhiều chỉ báo để đánh giá, tăng độ chính xác của tín hiệu.

- Chủ yếu dựa vào đảo chiều, kết hợp với xu hướng, nắm bắt điểm đảo chiều, giảm xác suất mua đỉnh bán đáy, bán thấp mua cao.

- Chỉ báo TTMSqueeze có thể xác định hiệu quả các giai đoạn điều chỉnh trong xu hướng, tránh các giao dịch không hiệu quả trong thời gian điều chỉnh.

- Phương pháp cắt lỗ dựa trên mức cao/thấp đơn giản và thực tế, có thể điều chỉnh khoảng cách cắt lỗ theo thị trường.

- Phương pháp chốt lời theo tỷ lệ rủi ro-lợi nhuận định lượng hóa quan hệ tỷ lệ lãi/lỗ, dễ dàng điều chỉnh.

- Các tham số đa dạng có thể được thiết lập linh hoạt, có thể tinh chỉnh theo khẩu vị rủi ro cá nhân.

Phân tích rủi ro

Chiến lược này cũng tồn tại những rủi ro sau:

- Kết hợp nhiều chỉ báo mặc dù tăng độ chính xác tín hiệu, nhưng cũng làm tăng khả năng bỏ lỡ điểm vào lệnh.

- Chiến lược chủ yếu dựa vào đảo chiều có thể hoạt động kém trong thị trường có xu hướng mạnh.

- Cắt lỗ dựa trên mức cao/thấp đôi khi có thể bị phá vỡ, không thể tránh hoàn toàn rủi ro.

- Chốt lời theo tỷ lệ rủi ro-lợi nhuận cũng có thể mất hiệu quả do giá nhảy gap hoặc điều chỉnh.

- Thiết lập tham số không phù hợp có thể dẫn đến thua lỗ hoặc dừng lỗ thường xuyên.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các khía cạnh sau:

- Thêm hoặc điều chỉnh trọng số chỉ báo để tín hiệu chính xác hơn.

- Tối ưu hóa tham số chỉ báo đảo chiều và xu hướng để tăng xác suất sinh lời.

- Tối ưu hóa tham số cắt lỗ dựa trên mức cao/thấp để cắt lỗ hợp lý hơn.

- Kiểm tra các tỷ lệ rủi ro-lợi nhuận khác nhau để đạt kết quả tối ưu.

- Điều chỉnh tham số số lượng vị thế để giảm tác động của một lệnh thua lỗ.

Tổng kết

Nhìn chung, chiến lược này thông qua sự kết hợp của nhiều chỉ báo và điều chỉnh tham số có thể cân bằng hiệu quả tâm lý giao dịch, đạt được lợi nhuận dương ổn định. Mặc dù vẫn còn một số không gian cải thiện, nhưng đã có giá trị ứng dụng thực tế. Thông qua phản hồi thị trường và tinh chỉnh tham số, chiến lược này có thể trở thành công cụ hữu hiệu để kiểm soát tâm lý giao dịch và đạt được lợi nhuận ổn định dài hạn.

- 1