ব্রেকআউট-ভিত্তিক ঊর্ধ্বমুখী প্রবণতা রেফারেন্স কৌশল

সারসংক্ষেপ

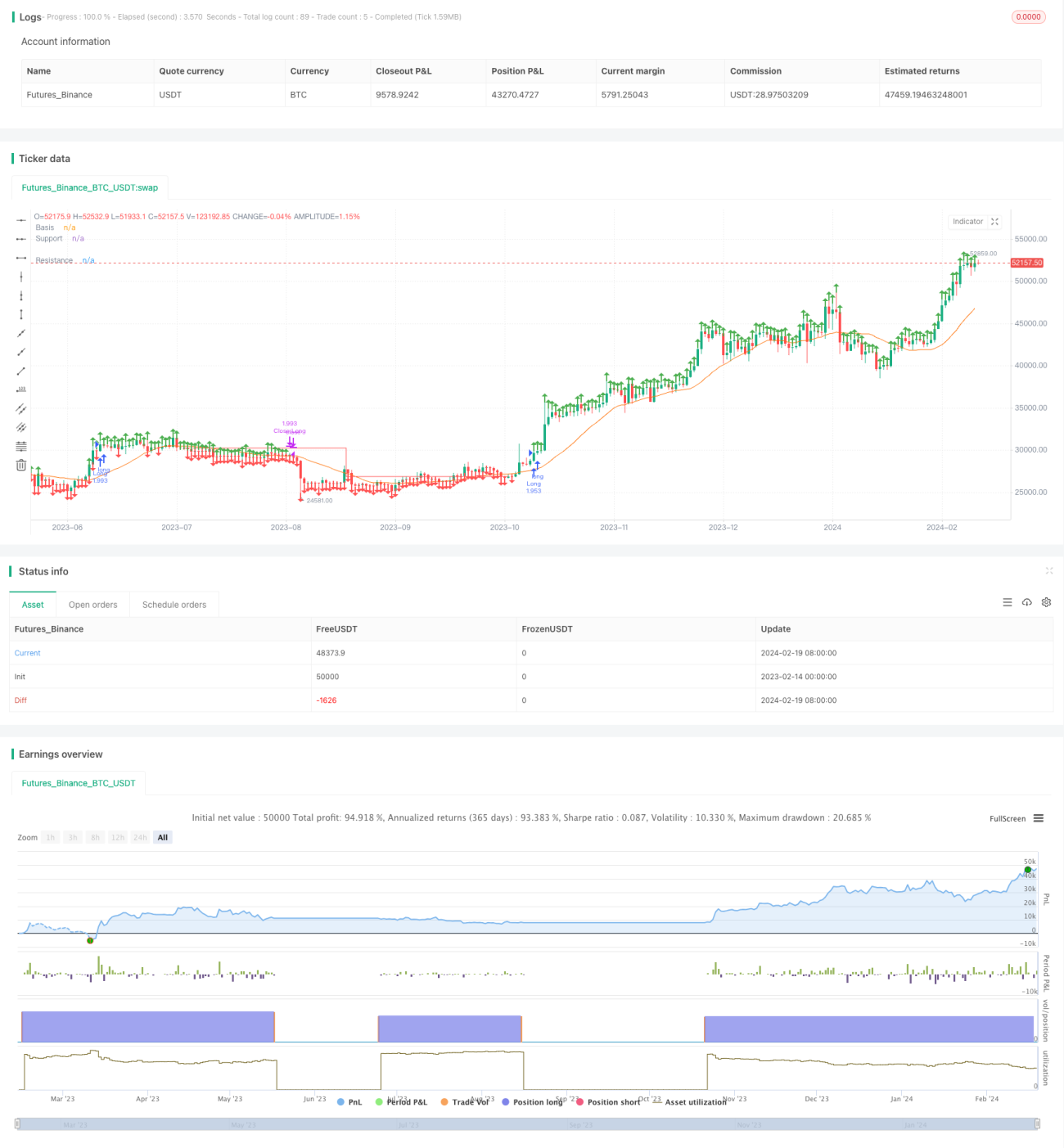

এই কৌশলটি একটি সরল মুভিং এভারেজের ভিত্তিতে প্রবণতার দিক নির্ধারণ করে, প্রতিরোধ ও সমর্থন রেখার মাধ্যমে ব্রেকআউট সংকেত তৈরি করে দীর্ঘমেয়াদী পজিশন ধারণের একটি কৌশল। দামের পিভট উচ্চ এবং পিভট নিম্ন গণনা করে প্রতিরোধ রেখা ও সমর্থন রেখা অঙ্কন করা হয়। যখন দাম প্রতিরোধ রেখা ভেঙে উপরে যায়, তখন লং পজিশন নেওয়া হয়, এবং যখন দাম সমর্থন রেখা ভেঙে নিচে যায়, তখন পজিশন বন্ধ করা হয়। এই কৌশলটি স্পষ্ট প্রবণতাযুক্ত শেয়ারের জন্য উপযুক্ত, যা ভালো রিস্ক-রিওয়ার্ড রেশিও প্রদান করতে পারে।

কৌশলের নীতি

- 20 দিনের সরল মুভিং এভারেজ গণনা করে প্রবণতা নির্ধারণের জন্য ভিত্তি রেখা তৈরি করা হয়।

- ব্যবহারকারীর ইনপুট প্যারামিটার অনুযায়ী পিভট উচ্চ এবং পিভট নিম্ন গণনা করা হয়।

- পিভট উচ্চ এবং পিভট নিম্নের ভিত্তিতে প্রতিরোধ রেখা ও সমর্থন রেখা অঙ্কন করা হয়।

- যখন ক্লোজিং প্রাইস প্রতিরোধ রেখার উপরে যায়, তখন লং এন্ট্রি নেওয়া হয়।

- যখন সমর্থন রেখা প্রতিরোধ রেখাকে নিচের দিকে ক্রস করে, তখন পজিশন বন্ধ করা হয়।

এই কৌশলটি সরল মুভিং এভারেজ ব্যবহার করে সামগ্রিক প্রবণতার দিক নির্ধারণ করে, তারপর কী পয়েন্ট ব্রেকআউটের মাধ্যমে ট্রেডিং সিগন্যাল তৈরি করে। এটি একটি সাধারণ ব্রেকআউট-টাইপ কৌশল। কী পয়েন্ট এবং প্রবণতা বিচারের মাধ্যমে, এটি ভুয়া ব্রেকআউট ফিল্টার করতে কার্যকর।

সুবিধার বিশ্লেষণ

- কৌশলটিতে পর্যাপ্ত সুযোগ রয়েছে, যা উচ্চ অস্থিরতাযুক্ত শেয়ারের জন্য উপযুক্ত এবং প্রবণতা ধরতে সহায়তা করে।

- ঝুঁকি নিয়ন্ত্রণ ভালো, রিস্ক-রিওয়ার্ড রেশিও উচ্চ।

- ব্রেকআউট সিগন্যাল ব্যবহার করে ভুয়া ব্রেকআউটের ঝুঁকি এড়ানো যায়।

- প্যারামিটার কাস্টমাইজ করা যায়, যা অভিযোজন ক্ষমতা বাড়ায়।

ঝুঁকি বিশ্লেষণ

- প্যারামিটার অপ্টিমাইজেশনের উপর নির্ভরশীল; অনুপযুক্ত প্যারামিটার ভুয়া ব্রেকআউটের সম্ভাবনা বাড়ায়।

- ব্রেকআউট সিগন্যালে বিলম্ব হতে পারে, ফলে কিছু সুযোগ হাতছাড়া হতে পারে।

- রেঞ্জবাউন্ড মার্কেটে সহজেই স্টপ লস হতে পারে।

- সমর্থন রেখার সময়মতো সমন্বয় না হলে লোকসান হতে পারে।

লাইভ ট্রেডিংয়ে প্যারামিটার অপ্টিমাইজ করে এবং স্টপ লস/টার্গেট প্রফিট কৌশল যুক্ত করে ঝুঁকি কমানো যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

- মুভিং এভারেজের সময়কালের প্যারামিটার অপ্টিমাইজ করা।

- প্রতিরোধ ও সমর্থন রেখার প্যারামিটার অপ্টিমাইজ করা।

- স্টপ লস ও টার্গেট প্রফিট কৌশল যুক্ত করা।

- ব্রেকআউট নিশ্চিতকরণ প্রক্রিয়া যোগ করা।

- ট্রেডিং ভলিউমের মতো অন্যান্য ইন্ডিকেটরের সাথে সংকেত ফিল্টার করা।

উপসংহার

এই কৌশলটি সামগ্রিকভাবে একটি সাধারণ ব্রেকআউট-টাইপ কৌশল, যা প্যারামিটার অপ্টিমাইজেশন ও লিকুইডিটির উপর নির্ভরশীল এবং প্রবণতা অনুসরণকারী ট্রেডারদের জন্য উপযুক্ত। এটি একটি রেফারেন্স ফ্রেমওয়ার্ক হিসেবে ব্যবহার করে প্রয়োজন অনুযায়ী মডিউল সম্প্রসারণ করা যেতে পারে, এবং স্টপ লস/টার্গেট প্রফিট ও সিগন্যাল ফিল্টারের মতো প্রক্রিয়ার মাধ্যমে ঝুঁকি কমানো ও স্থিতিশীলতা বাড়ানো যায়।

- 1