Gleitender-Durchschnitts-Crossover-Strategie

Überblick

Diese Strategie nutzt verschiedene technische Indikatoren wie gleitende Durchschnitte und Oszillatoren in Kombination mit Kreuzungsmustern gleitender Durchschnitte, um Kurstrends und Wendepunkte von Aktien zu identifizieren und Kauf- und Verkaufsentscheidungen zu treffen.

Prinzip

Die Strategie gliedert sich hauptsächlich in folgende Teile:

- Auswahl des Zeitrahmens: Festlegung des Minutenintervalls für den Kerzenchart, z. B. 1 Minute, 5 Minuten usw.

- Auswahl der gleitenden Durchschnitte: Konfiguration der Parameter gängiger gleitender Durchschnitte wie EMA, SMA, z. B. 10-Tage-Linie, 20-Tage-Linie usw.

- Auswahl der Oszillatoren: Konfiguration der Parameter von Oszillatoren wie RSI, MACD, Williams %R usw.

- Berechnung von Kauf- und Verkaufssignalen: Durch benutzerdefinierte Funktionen werden die Werte der gleitenden Durchschnitte und Oszillatoren berechnet. Ein Kaufsignal entsteht, wenn der kurzfristige gleitende Durchschnitt den langfristigen von unten kreuzt; ein Verkaufssignal, wenn der kurzfristige den langfristigen von oben kreuzt. Gleichzeitig werden überkaufte/überverkaufte Indikatoren zur Identifizierung von Extrempunkten herangezogen.

- Bewertungssystem: Die Kauf- und Verkaufssignale der einzelnen Indikatoren werden numerisch bewertet und gemittelt, um einen Gesamtbewertungsindex zu erhalten. Ein Index über 0 gilt als Kaufsignal, unter 0 als Verkaufssignal.

- Handelssignale: Basierend darauf, ob der Bewertungsindex größer oder kleiner als 0 ist, werden endgültige Handelssignale generiert und Kauf- oder Verkaufsaktionen ausgeführt.

Die Strategie kombiniert mehrere Indikatoren, um Kurstrends und Wendepunkte effektiv zu erkennen und die Zuverlässigkeit der Signale zu erhöhen. Die Kreuzung gleitender Durchschnitte ist ein bewährtes Trendfolge-Signal, das in Kombination mit Oszillatoren hilft, Fehlsignale zu vermeiden. Das Bewertungssystem sorgt zudem für klarere Handelssignale.

Vorteile

- Kombination von gleitenden Durchschnitten und mehreren Oszillatoren führt zu zuverlässigeren Handelssignalen und vermeidet Fehlsignale

- Das Bewertungssystem macht Kauf- und Verkaufssignale klarer

- Modulare Programmierung mit benutzerdefinierten Funktionen, klare Code-Struktur

- Mehrere Zeitrahmen für eine kombinierte Analyse erhöhen die Genauigkeit

- Optimierte Parametereinstellungen wie RSI-Länge, MACD-schnelle/langsame Perioden usw.

- Flexibilität durch anpassbare Parameter für Indikatoren und gleitende Durchschnitte

Bestehende Risiken

- Unterschiede in der Aktienperformance unter übergeordneten Markttrends

- Möglicherweise hohe Handelsfrequenz, was zu höheren Transaktionskosten und Slippage-Risiko führt

- Erfordert wiederholtes Testen und Optimieren der Parameter, um sie an unterschiedliche Aktieneigenschaften anzupassen

- Es besteht ein gewisses Drawdown- und Verlustrisiko

Die folgenden Maßnahmen können diese Risiken verringern:

- Aktienauswahl unter Berücksichtigung des Markttrends

- Anpassung der Haltedauer zur Reduzierung der Handelsfrequenz

- Optimierung der Parameter für individuelle Aktieneigenschaften

- Einsatz einer Stop-Loss-Strategie zur Begrenzung von Verlusten

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Hinzufügen weiterer Indikatoren wie Volatilitätsindikatoren zur Signalverstärkung

- Kombination mit maschinellen Lernmethoden zur automatischen Parameteroptimierung

- Integration eines Moduls zur Aktien- und Branchenauswahl

- Einbindung quantitativer Aktienauswahlmethoden

- Verwendung adaptiver Stop-Loss- und Trailing-Stop-Methoden

- Berücksichtigung der Marktlage zur Vermeidung unsicherer Umgebungen

- Analyse der Live-Handelsergebnisse zur Anpassung der Bewertungsgewichte

Zusammenfassend integriert die Strategie Durchbruchsmuster gleitender Durchschnitte und mehrere Indikatoren, um Kursbewegungen effektiv zu erkennen. Es bedarf jedoch kontinuierlicher Tests und Optimierungen, um das Risiko zu kontrollieren. Zukünftige Verbesserungen können in den Bereichen Aktienauswahl, Parameteroptimierung und Stop-Loss vorgenommen werden.

Fazit

Die Strategie nutzt Kreuzungen gleitender Durchschnitte als primäres Handelssignal, ergänzt durch verschiedene Oszillatoren zur Bestätigung, und erzeugt mittels eines Bewertungssystems klare Kauf- und Verkaufssignale. Sie kann Kurstrends und Wendepunkte effektiv identifizieren, erfordert jedoch eine Kontrolle der Handelsfrequenz zur Reduzierung von Transaktionskosten und Risiken sowie eine kontinuierliche Parameteroptimierung. Sie besitzt einen gewissen praktischen Nutzen und bietet Raum für Verbesserungen.

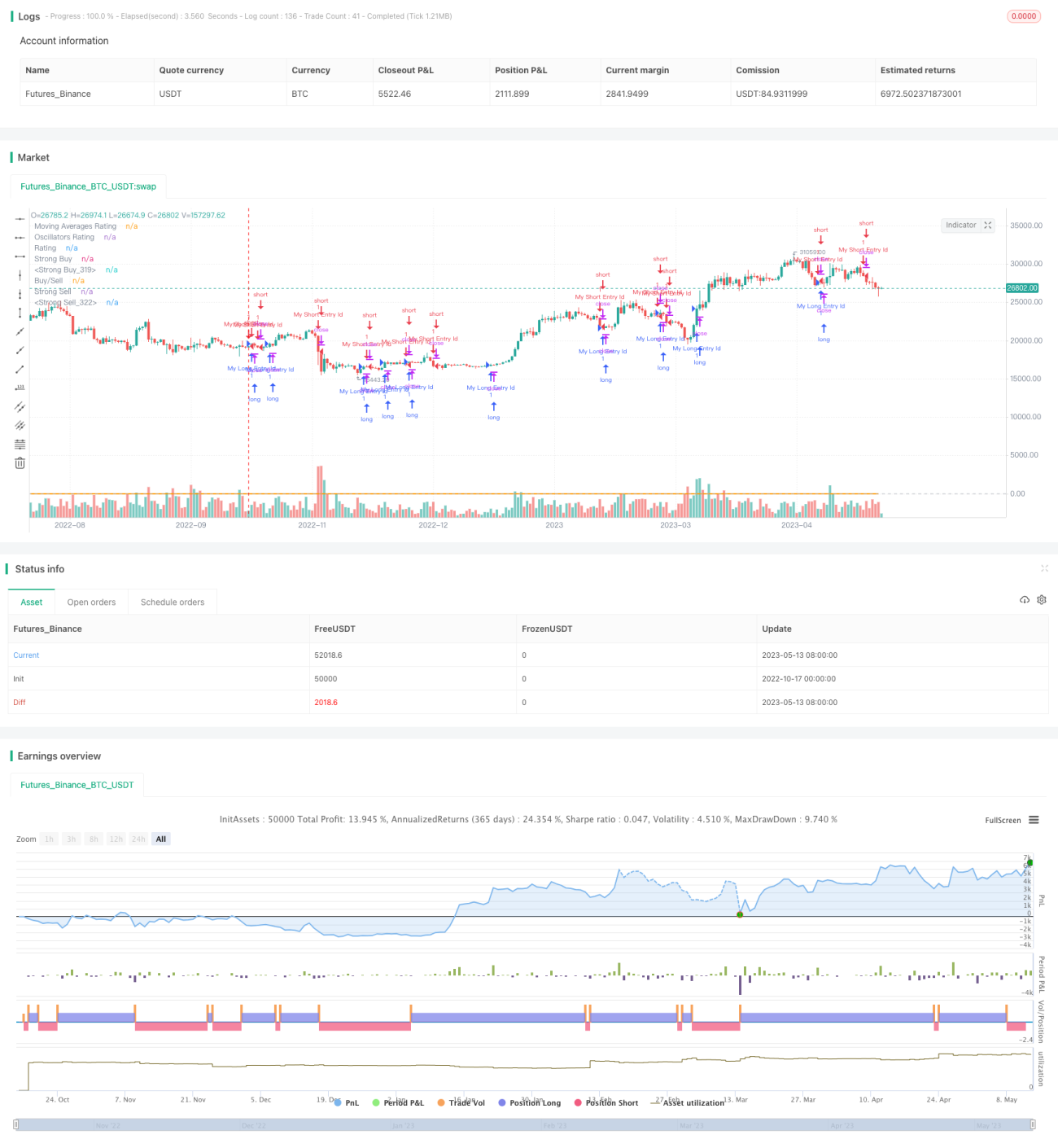

/*backtest

start: 2022-10-17 00:00:00

end: 2023-05-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("TV Signal", overlay=true, initial_capital = 500, currency = "USD")

// -------------------------------------- GLOBAL SELECTION --------------------------------------------- //- 1