Dreifach-Gleitender-Durchschnitt-Kanal-Trendfolgestrategie

Übersicht

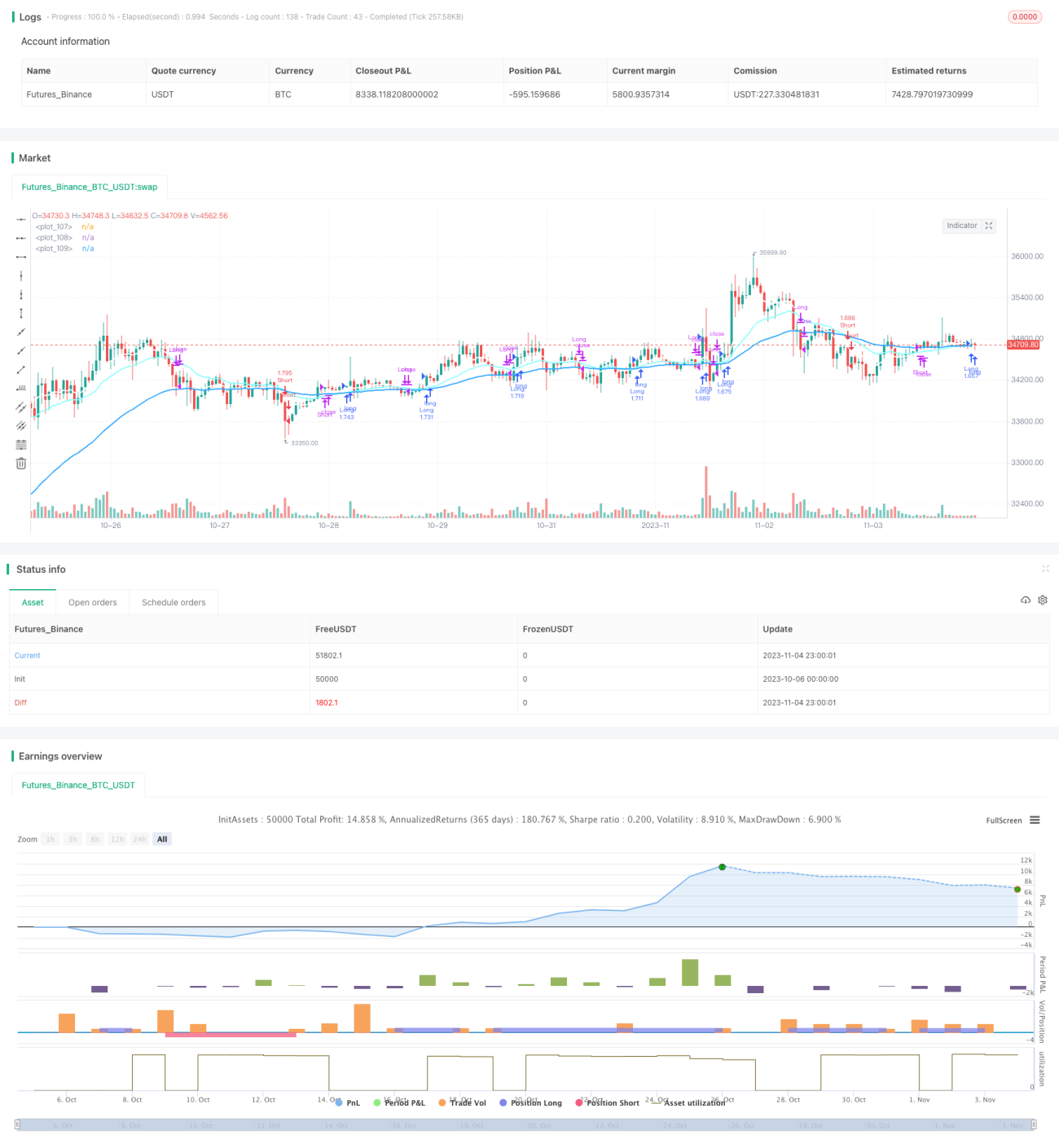

Die Strategie verwendet eine Kombination aus drei gleitenden Durchschnitten, um basierend auf der Reihenfolge der gleitenden Durchschnitte die Trendrichtung zu bestimmen und dem Trend zu folgen. Wenn der schnelle gleitende Durchschnitt, der mittlere gleitende Durchschnitt und der langsame gleitende Durchschnitt in dieser Reihenfolge angeordnet sind, wird eine Long-Position eröffnet. Wenn der langsame gleitende Durchschnitt, der mittlere gleitende Durchschnitt und der schnelle gleitende Durchschnitt in dieser Reihenfolge angeordnet sind, wird eine Short-Position eröffnet.

Strategieprinzip

Die Strategie verwendet drei gleitende Durchschnitte mit unterschiedlichen Perioden: einen schnellen gleitenden Durchschnitt, einen mittleren gleitenden Durchschnitt und einen langsamen gleitenden Durchschnitt.

Einstiegsbedingungen:

- Long: Wenn der schnelle gleitende Durchschnitt > der mittlere gleitende Durchschnitt > der langsame gleitende Durchschnitt, wird der Markt als im Aufwärtstrend befindlich angesehen und es wird eine Long-Position eröffnet.

- Short: Wenn der langsame gleitende Durchschnitt < der mittlere gleitende Durchschnitt < der schnelle gleitende Durchschnitt, wird der Markt als im Abwärtstrend befindlich angesehen und es wird eine Short-Position eröffnet.

Ausstiegsbedingungen:

- Ausstieg basierend auf gleitenden Durchschnitten: Wenn sich die Reihenfolge der drei gleitenden Durchschnitte umkehrt, wird die Position geschlossen.

- Ausstieg basierend auf Take-Profit und Stop-Loss: Es werden feste Take-Profit- und Stop-Loss-Punkte gesetzt, z. B. ein Take-Profit von 12 % und ein Stop-Loss von 1 %. Die Position wird geschlossen, wenn der Take-Profit- oder Stop-Loss-Preis erreicht wird.

Die Strategie ist einfach und direkt, nutzt drei gleitende Durchschnitte zur Bestimmung der Markttrendrichtung und ermöglicht Trendfolgehandel. Sie eignet sich für Märkte mit starken Trends.

Vorteilsanalyse

- Verwendung von drei gleitenden Durchschnitten zur Trendbestimmung, Filterung von Marktrauschen und Erkennung der Trendrichtung.

- Einsatz von gleitenden Durchschnitten mit unterschiedlichen Perioden zur genaueren Bestimmung von Trendwendepunkten.

- Kombination des gleitenden Durchschnittsindikators mit festen Take-Profit- und Stop-Loss-Punkten zur Risikosteuerung des Kapitals.

- Die Strategie ist einfach und intuitiv, leicht zu verstehen und umzusetzen.

- Die Parameter der gleitenden Durchschnitte können einfach optimiert werden, um sich an verschiedene Zeitrahmen anzupassen.

Risiken und Verbesserungen

- In großen Zeitrahmen können gleitende Durchschnitte zu vielen Fehlsignalen führen, was unnötige Verluste verursacht.

- Es könnten weitere Indikatoren oder Filterbedingungen hinzugefügt werden, um die Gewinnrate zu erhöhen.

- Die Parameterkombinationen der gleitenden Durchschnitte könnten optimiert werden, um sich an breitere Marktbedingungen anzupassen.

- Es könnten Trendstärkeindikatoren integriert werden, um ein Kaufen am Hoch oder Verkaufen am Tief zu vermeiden.

- Ein automatischer Stop-Loss könnte eingebaut werden, um Verluste zu begrenzen.

Zusammenfassung

Die Drei-gleitende-Durchschnitte-Trendfolgestrategie ist insgesamt klar und verständlich. Sie nutzt gleitende Durchschnitte zur Bestimmung der Trendrichtung und ermöglicht einen einfachen Trendfolgehandel. Der Vorteil der Strategie liegt in ihrer einfachen Umsetzbarkeit; durch Anpassung der Periodenparameter der gleitenden Durchschnitte kann sie an verschiedene Zeitrahmen angepasst werden. Allerdings besteht auch ein gewisses Risiko von Fehlsignalen. Dies kann durch Hinzufügen weiterer Indikatoren oder Bedingungen optimiert werden, um unnötige Verluste zu reduzieren und die Gewinnrate der Strategie zu erhöhen. Insgesamt eignet sich die Strategie für Anfänger, die sich für Trendhandel interessieren, zum Lernen und Üben.

- 1