Adaptive Take-Profit- und Stop-Loss-Strategie basierend auf dualem Zeitrahmen und Momentum-Indikator

Überblick

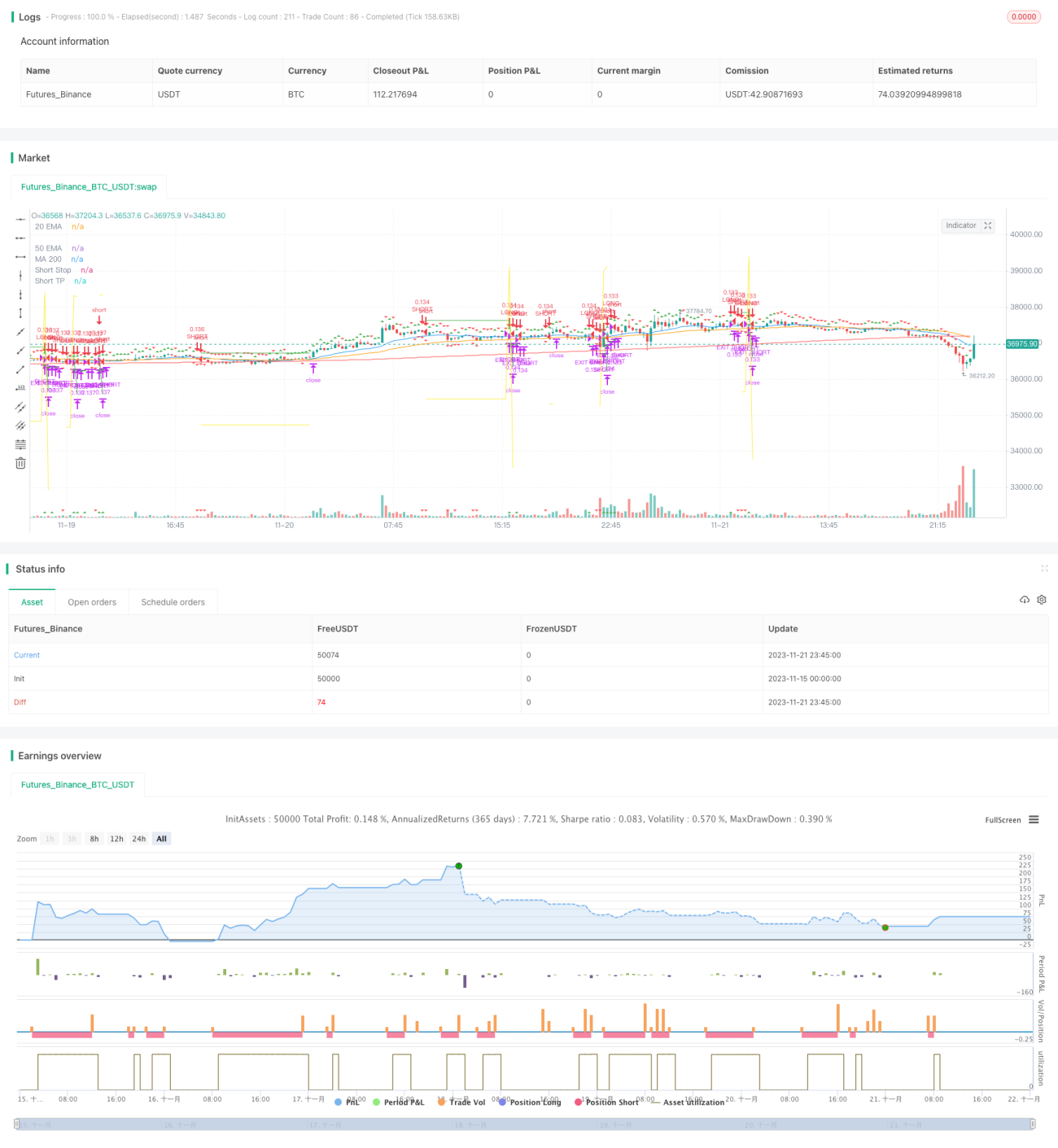

Diese Strategie nutzt eine Kombination aus zwei Zeitrahmen und Momentum-Indikatoren, um adaptive Stop-Loss- und Take-Profit-Niveaus zu realisieren. Der primäre Zeitrahmen überwacht die Trendrichtung, während der sekundäre Zeitrahmen zur Signalbekräftigung dient. Wenn beide in die gleiche Richtung weisen, wird ein Handelssignal generiert. Nach dem Einstieg werden die Take-Profit- und Stop-Loss-Niveaus durch eine progressive Anpassung aktualisiert.

Strategieprinzip

-

Der primäre Zeitrahmen verwendet den linearen Regressionsindikator Sqqueeze Momentum (SQM) zur Trendbestimmung, der sekundäre Zeitrahmen nutzt eine EMA-Kombination des SQM-Indikators, um Falschsignale zu filtern.

-

Wenn der SQM im Hauptchart nach oben ausbricht und der SQM im Nebenchart ebenfalls nach oben zeigt, wird eine Long-Position eröffnet; wenn der SQM im Hauptchart nach unten ausbricht und der SQM im Nebenchart ebenfalls nach unten zeigt, wird eine Short-Position eröffnet.

-

Nach dem Einstieg werden basierend auf den eingegebenen Parametern initiale Take-Profit- und Stop-Loss-Niveaus festgelegt. Wenn der Kurs das Take-Profit-Niveau erreicht, werden Take-Profit- und Stop-Loss-Niveaus aktualisiert. Dabei wird das Take-Profit-Niveau schrittweise um einen bestimmten Prozentsatz erhöht und das Stop-Loss-Niveau schrittweise reduziert, um eine progressive Gewinnsicherung zu erreichen.

Strategievorteile

-

Die doppelte Zeitrahmenfilterung eliminiert Falschsignale und gewährleistet die Signalgenauigkeit.

-

Der SQM-Indikator bestimmt die Trendrichtung und vermeidet Störungen durch Marktrauschen.

-

Die adaptive Stop-Loss- und Take-Profit-Mechanik sichert Gewinne maximal ab und kontrolliert das Risiko effektiv.

Risikoanalyse

-

Eine falsche Parametereinstellung des SQM-Indikators kann dazu führen, dass Trendwenden verpasst werden, was zu Verlusten führt.

-

Eine ungeeignete Auswahl des Zeitrahmens für den Nebenchart kann Rauschen nicht effektiv filtern und Fehltrades verursachen.

-

Eine zu großzügige Stop-Loss-Spanne kann zu erheblichen Einzelverlusten führen.

Optimierungsmöglichkeiten

-

Die Parameter des SQM-Indikators müssen je nach Markt angepasst werden, um seine Empfindlichkeit zu gewährleisten.

-

Auch der Zeitrahmen des Nebencharts sollte mit verschiedenen Perioden getestet werden, um den effektivsten Filter zu finden.

-

Der Stop-Loss-Bereich kann als Schwankungsband statt als fester Wert definiert werden, um sich an die Marktvolatilität anzupassen.

Zusammenfassung

Insgesamt ist diese Strategie sehr praktisch. Die Kombination aus zwei Zeitrahmen und Momentum-Indikatoren bestimmt den Trend, und die adaptive Stop-Loss- und Take-Profit-Methode ermöglicht stabile Gewinne. Durch die Optimierung der SQM-Parameter, des Nebenchart-Zeitrahmens und der Stop-Loss-Spanne kann die Strategie noch effektiver gestaltet werden und ist es wert, im Live-Handel angewendet und weiterentwickelt zu werden.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1