Niedrigpunkt-Pyramiden-Niedrigrisiko-Tracking-Strategie

Diese Strategie identifiziert potenzielle Tiefpunkte in der Preisbewegung durch die Kombination verschiedener Indikatoren und reduziert das Risiko durch einen pyramidenartigen Nachverfolgungsansatz beim schrittweisen Aufbau von Positionen. Gleichzeitig integriert die Strategie Funktionen wie Stop-Loss, Take-Profit und Trailing-Stop-Loss, um das Risiko effektiv zu kontrollieren.

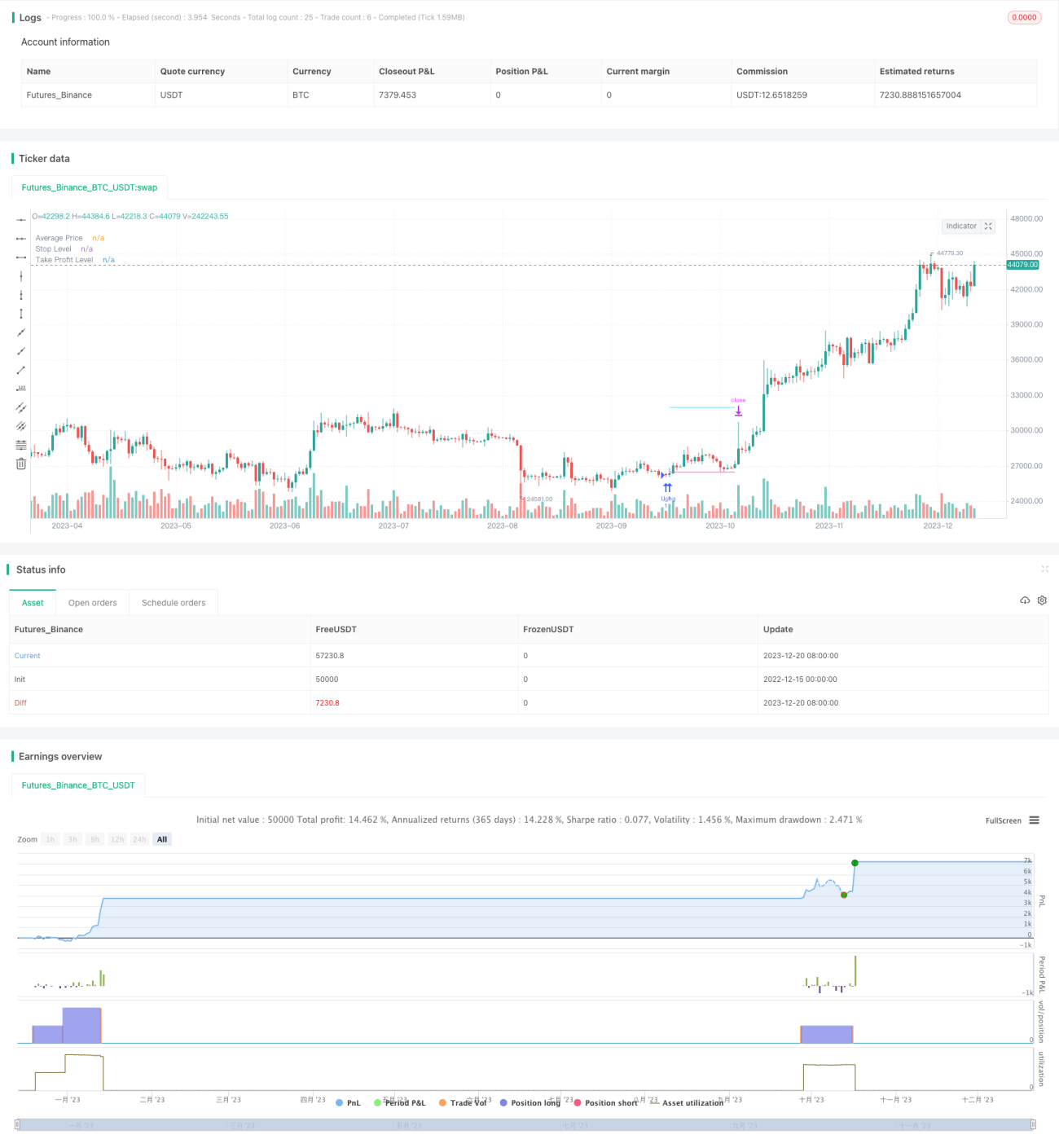

Strategieübersicht

Die Strategie verwendet zunächst die Differenz zwischen RSI und EMA RSI, um potenzielle Tiefpunkte im Kurs zu identifizieren. Um Fehlsignale zu filtern, werden zusätzlich ein gleitender Durchschnitt und ein Multi-Timeframe-Stochastik-Indikator zur Bestätigung herangezogen. Sobald ein Tiefpunktsignal bestätigt wurde, werden schrittweise Long-Positionen geringfügig unterhalb dieses Punktes aufgebaut – dies ist der Kern der verfolgenden Pyramide. Die Strategie erlaubt die Eröffnung von bis zu 12 Folgeaufträgen, wobei die Anzahl der Kontrakte pro Auftrag aufsteigend ist, was das Risiko effektiv streut. Alle Aufträge folgen einem gemeinsamen Stop-Loss zum Ausstieg, und zusätzlich kann für jeden Auftrag ein separater Take-Profit gesetzt werden. Zur weiteren Risikokontrolle implementiert die Strategie einen globalen Stop-Loss basierend auf einem prozentualen Anteil des Kontosaldos.

Strategieprinzip

Die Strategie besteht aus drei Hauptmodulen: dem Tiefpunkterkennungsmodul, dem Pyramiden-Nachverfolgungsmodul und dem Risikokontrollmodul.

Tiefpunkterkennungsmodul verwendet die Differenz zwischen dem RSI-Indikator und seinem EMA, um potenzielle Tiefpunkte zu identifizieren. Zur Verbesserung der Genauigkeit werden zusätzlich ein gleitender Durchschnitt und ein Multi-Timeframe-Stochastik-Indikator zur Signalfilterung eingesetzt. Das Tiefpunktsignal wird nur dann als gültig bestätigt, wenn der Kurs unter dem gleitenden Durchschnitt liegt und die Stochastik-K-Linie unter 30 fällt.

Pyramiden-Nachverfolgungsmodul ist der Kern dieser Strategie. Sobald ein Tiefpunktsignal bestätigt wurde, wird der erste Auftrag bei einem Kurs eröffnet, der 0,1 % unter diesem Tiefpunkt liegt. Falls der Kurs weiter fällt und einen bestimmten Prozentsatz unter dem durchschnittlichen Einstiegspreis liegt, werden weitere Long-Aufträge hinzugefügt. Die Anzahl der neuen Aufträge steigt sukzessive an; zum Beispiel ist der dritte Auftrag dreimal so groß wie der erste. Diese pyramidenartige Nachverfolgung mittelt das Risiko. Die Strategie erlaubt maximal 12 Folgeaufträge.

Risikokontrollmodul umfasst drei Aspekte. Erstens der globale Stop-Loss, der auf dem höchsten Kurs eines bestimmten Zeitraums basiert. Alle Aufträge folgen diesem Stop-Loss gleichzeitig. Zweitens ein unabhängiger Take-Profit für jeden Auftrag, der als Prozentsatz des Einstiegskurses festgelegt werden kann. Drittens ein globaler Stop-Loss basierend auf dem Kontoeigenkapital – dies ist die stärkste Risikokontrollmaßnahme.

Strategievorteile

- Reduziert das Risiko einzelner Aufträge durch pyramidenartige Nachverfolgung und streut gleichzeitig das Gesamtrisiko

- Kombination mehrerer Indikatoren verbessert die Genauigkeit der Tiefpunkterkennung

- Globale Stop-Loss-, Take-Profit- und Trailing-Stop-Loss-Funktionen kontrollieren das Risiko effektiv

- Der prozentuale Stop-Loss auf das Eigenkapital schützt das Konto vor großen Verlusten

- Durch Anpassung der Parameter kann ein Gleichgewicht zwischen Risiko und Ertrag gefunden werden

Strategierisiken

- Die Genauigkeit der Tiefpunkterkennung ist begrenzt; möglicherweise werden optimale Einstiegspunkte verpasst oder Fehlsignale erfasst

- Beim Hinzufügen von Aufträgen kann es zu ungünstigen Kursbewegungen kommen, die Verluste vergrößern

- Es wird ein längerer Handelszeitraum benötigt, um die Vorteile der Strategie zu zeigen

- Falsche Parametereinstellungen können zu unzureichender Risikokontrolle führen

Zur Reduzierung der genannten Risiken können folgende Optimierungen vorgenommen werden:

- Austausch oder Hinzufügen von Indikatoren zur Verbesserung der Tiefpunkterkennungsgenauigkeit

- Optimierung von Parametern wie Auftragsanzahl, Abstand und Take-Profit-Spanne, um das Risiko pro Auftrag zu verringern

- Verkürzung der Stop-Loss-Spanne, um Gewinne zu schützen

- Testen verschiedener Instrumente; Bevorzugung liquider und volatiler Instrumente

Optimierungsmöglichkeiten

Diese Strategie bietet weiteres Optimierungspotenzial:

- Einführung fortschrittlicherer Techniken wie maschinelles Lernen zur Identifizierung von Tiefpunkten

- Dynamische Anpassung von Parametern wie Auftragsanzahl und Stop-Loss-Spanne basierend auf dem Marktzustand

- Hinzufügen einer Box-Stop-Loss-Strategie, um Verluste zu begrenzen

- Implementierung eines Wiedereinstiegsmechanismus

- Optimierung der Strategieparameter für Aktien und Kryptowährungen

Zusammenfassung

Diese Strategie reduziert effektiv das Risiko einzelner Aufträge durch den pyramidenartigen Nachverfolgungsansatz. Die Funktionen wie globaler Stop-Loss, Take-Profit und Trailing-Stop-Loss spielen eine gute Rolle bei der Risikokontrolle. Allerdings gibt es noch Optimierungsspielraum bei der Tiefpunkterkennung. Wenn fortschrittlichere Techniken eingeführt werden, eine dynamische Parameteranpassung hinzugefügt wird und die Parameter optimiert werden, kann das Risiko-Ertrags-Verhältnis dieser Strategie erheblich verbessert werden.

- 1