Optimierungsstrategie für Multi-Zeitrahmen-Kreuzungen gleitender Durchschnitte

1

Follow

1802

Followers

Übersicht

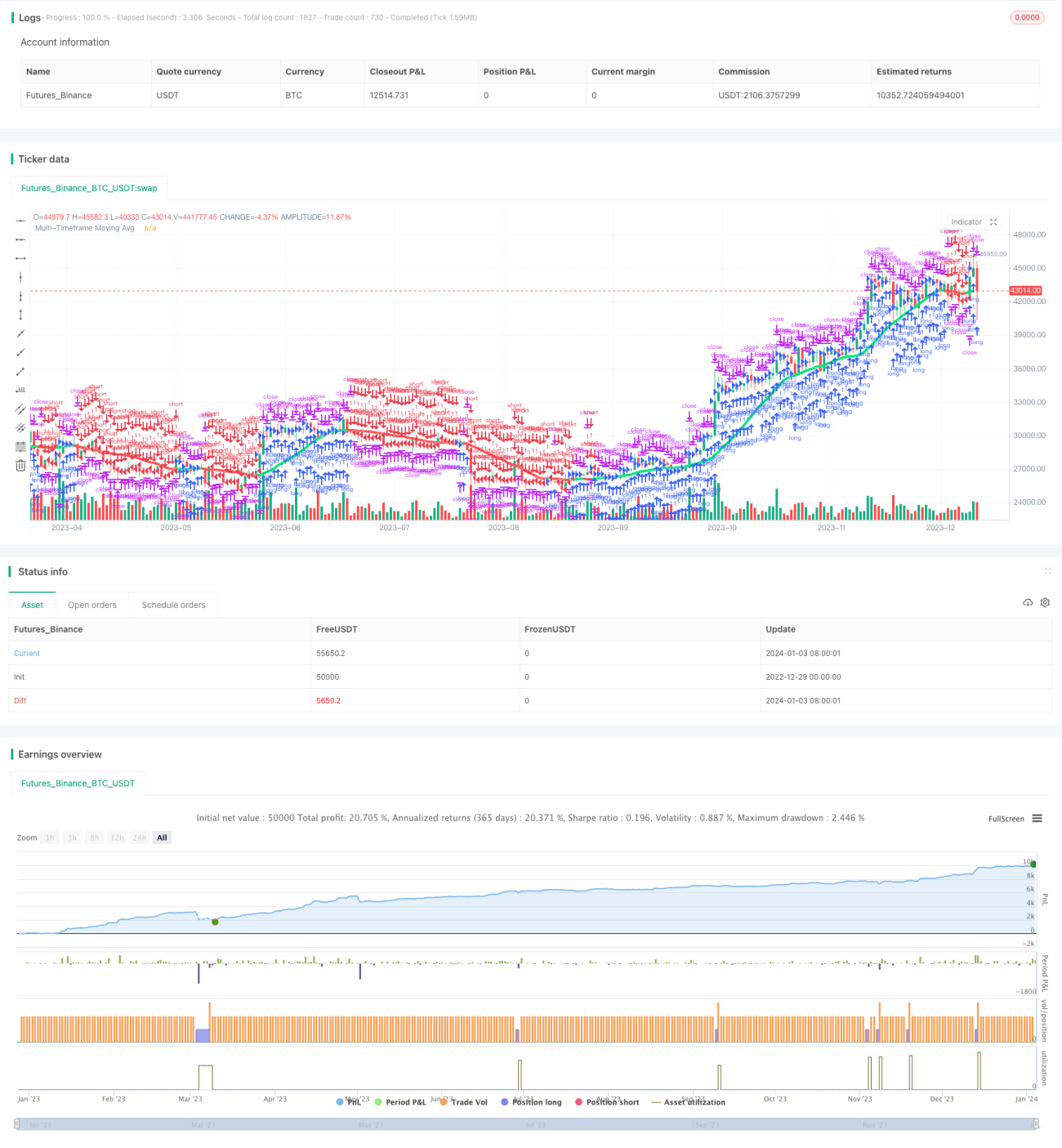

Diese Strategie basiert auf dem bekannten Indikator CM_Ultimate_MA_MTF und zeichnet gleitende Durchschnitte auf mehreren Zeitebenen, um Kreuzungen von MA über verschiedene Zeiträume zu realisieren. Die Strategie verfügt zudem über eine Trailing-Stop-Funktion.

Strategieprinzip

- Je nach Benutzerauswahl werden MA-Linien auf dem Hauptchart-Zeitraum und höheren Zeiträumen mittels verschiedener MA-Typen gezeichnet.

- Wenn die schnellere MA-Linie die langsamere MA-Linie von unten nach oben kreuzt, wird eine Long-Position eröffnet; bei einem Kreuzen von oben nach unten wird eine Short-Position eröffnet.

- Ein Trailing-Stop-Mechanismus wird hinzugefügt, um das Risiko weiter zu kontrollieren.

Vorteilsanalyse

- MA-Kreuzungen auf mehreren Zeitebenen können die Signalqualität verbessern und Fehlsignale reduzieren.

- Die Kombination verschiedener MA-Typen kann die Stärken der jeweiligen Indikatoren nutzen und die Stabilität erhöhen.

- Ein Trailing-Stop hilft, rechtzeitig Verluste zu begrenzen und die Wahrscheinlichkeit großer Verluste zu verringern.

Risikoanalyse

- MA-Indikatoren sind nachlaufend, was dazu führen kann, dass kurzfristige Handelsmöglichkeiten verpasst werden.

- Die MA-Parameter müssen angemessen optimiert werden, da sonst zu viele Fehlsignale entstehen können.

- Eine ungeeignete Festlegung des Stop-Loss kann zu unnötigen Stopps führen.

Optimierungsansätze

- Verschiedene Parameterkombinationen der MA können getestet werden, um die optimalen Parameter zu finden.

- Weitere Indikatoren können zur Filterung hinzugefügt werden, um die Signalqualität zu verbessern.

- Die Stop-Loss-Strategie kann optimiert werden, um sie besser an die Marktgegebenheiten anzupassen.

Zusammenfassung

Diese Strategie integriert die Multi-Timeframe-Analyse gleitender Durchschnitte und eine Trailing-Stop-Methode, um die Signalqualität zu verbessern und das Risikoniveau zu kontrollieren. Durch Parameteroptimierung und Hinzufügen weiterer Indikatoren kann die Effektivität der Strategie weiter gesteigert werden.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1