Referenzstrategie für Aufwärtstrend-Ausbrüche

Überblick

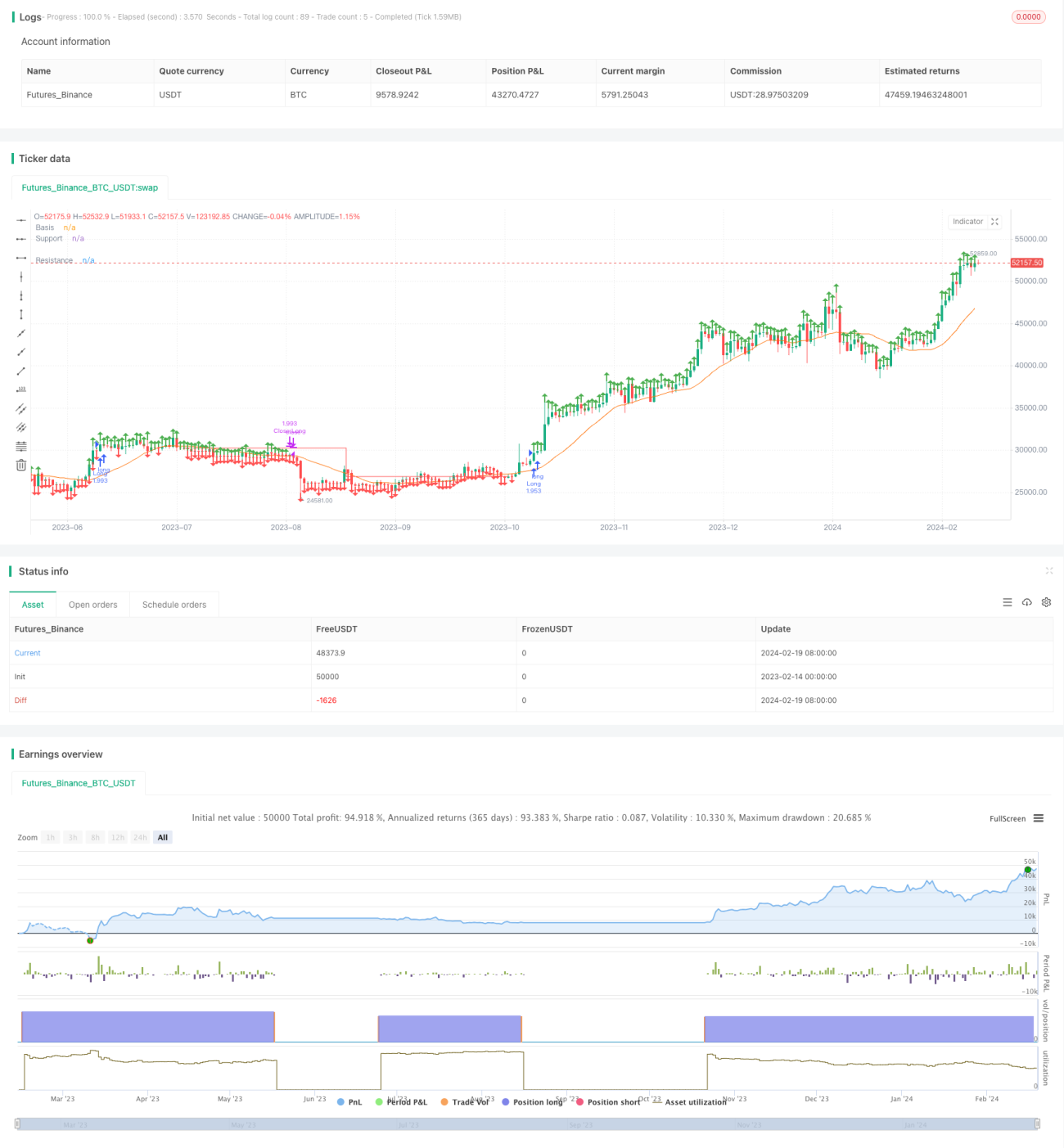

Bei dieser Strategie handelt es sich um eine langfristige Positionshandelsstrategie, die auf einem einfachen gleitenden Durchschnitt zur Bestimmung der Trendrichtung basiert und zusammen mit Widerstands- und Unterstützungslinien Einstiegssignale generiert. Durch die Berechnung der Pivot-Hochs und Pivot-Tiefs werden Widerstands- und Unterstützungslinien gezeichnet. Wenn der Preis die Widerstandslinie durchbricht, wird eine Long-Position eröffnet, und wenn der Preis die Unterstützungslinie durchbricht, wird die Position geschlossen. Diese Strategie eignet sich für Aktien mit einem klaren Trend und kann ein gutes Risiko-Rendite-Verhältnis erzielen.

Strategieprinzip

- Berechnung des 20-Tage-einfachen gleitenden Durchschnitts als Basislinie zur Trendbestimmung.

- Berechnung der Pivot-Hochs und Pivot-Tiefs basierend auf den Benutzereingabeparametern.

- Zeichnen der Widerstands- und Unterstützungslinien anhand der Pivot-Hochs und Pivot-Tiefs.

- Wenn der Schlusskurs über der Widerstandslinie liegt, wird eine Long-Position eröffnet.

- Wenn die Unterstützungslinie die Widerstandslinie nach unten durchbricht, wird die Position geschlossen.

Diese Strategie verwendet einen einfachen gleitenden Durchschnitt, um die allgemeine Trendrichtung zu bestimmen, und nutzt dann Ausbrüche von Schlüsselpunkten als Handelssignale. Es handelt sich um eine typische Ausbruchsstrategie. Durch die Kombination von Schlüsselpunkten und Trendbestimmung können Fehlausbrüche effektiv gefiltert werden.

Vorteile

- Ausreichende Handelsmöglichkeiten, geeignet für Aktien mit hoher Volatilität, die Trends leicht erfassen.

- Gutes Risikomanagement, hohes Risiko-Rendite-Verhältnis.

- Nutzung von Ausbruchssignalen zur Vermeidung von Fehlausbruchsrisiken.

- Anpassbare Parameter für hohe Flexibilität.

Risikoanalyse

- Abhängigkeit von der Parameteroptimierung; ungeeignete Parameter erhöhen die Wahrscheinlichkeit von Fehlausbrüchen.

- Verzögerung der Ausbruchssignale, möglicherweise Verpassen einiger Chancen.

- Leichter Stop-Loss in Seitwärtsmärkten.

- Unzeitgemäße Anpassung der Unterstützungslinien kann zu Verlusten führen.

Durch Optimierung der Parameter im Live-Handel und Kombination mit Stop-Loss- und Take-Profit-Strategien können Risiken reduziert werden.

Optimierungsrichtungen

- Optimierung der Periodenparameter des gleitenden Durchschnitts.

- Optimierung der Parameter für Unterstützungs- und Widerstandslinien.

- Hinzufügen von Stop-Loss- und Take-Profit-Strategien.

- Einführung eines Bestätigungsmechanismus für Ausbrüche.

- Kombination mit Indikatoren wie Handelsvolumen zur Signalfilterung.

Zusammenfassung

Die Strategie ist insgesamt eine typische Ausbruchsstrategie, die von Parameteroptimierung und Liquidität abhängt. Sie eignet sich für Trendfolgehändler. Als Referenzrahmen kann sie je nach Bedarf modular erweitert werden, um durch Mechanismen wie Stop-Loss, Take-Profit und Signalfilterung Risiken zu reduzieren und die Stabilität zu verbessern.

- 1