Multi-Timeframe-Handelsstrategie basierend auf dem Kompressionsindikator

Überblick

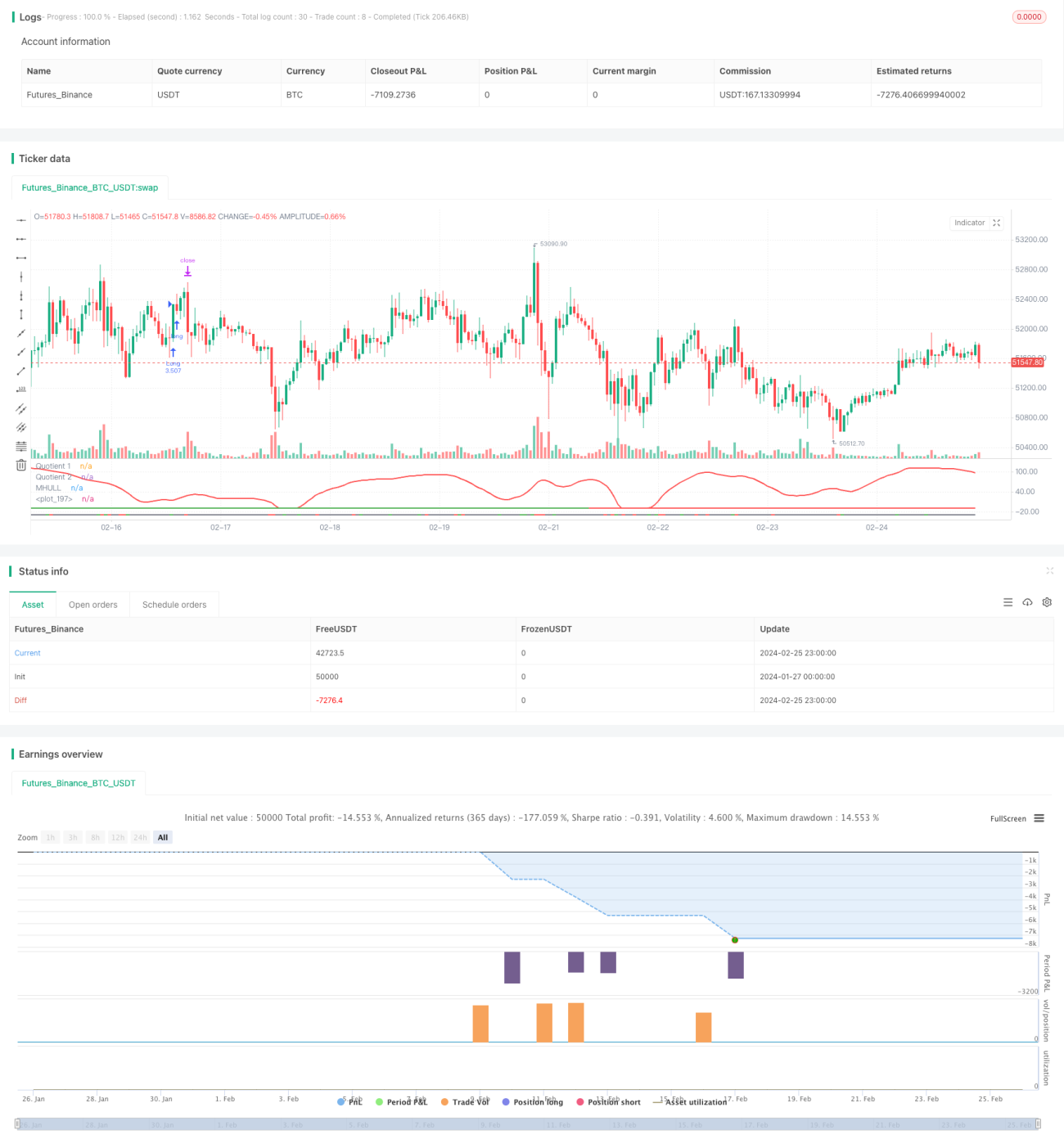

Diese Strategie kombiniert die drei Indikatoren Boom Hunter, Hull Suite und Volatility Oscillator, um eine quantitative Strategie für Trendfolge und Ausbruchshandel in mehreren Zeitrahmen umzusetzen. Die Strategie eignet sich für digitale Vermögenswerte wie Bitcoin, die durch hohe Volatilität und plötzliche Kursbewegungen gekennzeichnet sind.

Prinzip

Die Kernlogik der Strategie basiert auf den folgenden drei Indikatoren:

-

Boom Hunter: Ein Oszillator, der die Indikatorkompressionstechnik nutzt. Er generiert Kauf- und Verkaufssignale durch die Kreuzung zweier Indikatoren (Quotient1 und Quotient2).

-

Hull Suite: Eine Gruppe von geglätteten gleitenden Durchschnitten, die die Trendrichtung anhand der Beziehung zwischen der Mittellinie sowie den oberen und unteren Bändern bestimmt.

-

Volatility Oscillator: Ein Oszillatorindikator, der die Volatilität der Kursbewegungen quantifiziert.

Die Einstiegslogik der Strategie besagt: Zum Zeitpunkt der Aufwärts- oder Abwärtskreuzung der beiden Quotienten-Indikatoren des Boom Hunters muss der Kurs die mittlere Hull-Linie durchbrechen und eine Divergenz zum oberen oder unteren Band aufweisen, während sich der Volatility-Oszillator im überkauften oder überverkauften Bereich befindet. Dadurch können falsche Ausbruchssignale herausgefiltert und die Einstiegsgenauigkeit erhöht werden.

Der Stop-Loss wird durch die Suche nach dem niedrigsten Tief oder höchsten Hoch innerhalb eines bestimmten Zeitraums (standardmäßig 20 Kerzen) festgelegt. Der Gewinn wird durch Multiplikation des Stop-Loss-Prozentsatzes mit dem konfigurierten Take-Profit-Verhältnis (standardmäßig das 3-fache) erzielt. Die Positionsgröße wird auf Basis eines Prozentsatzes des gesamten Kontokapitals (standardmäßig 3 %) und der spezifischen Stop-Loss-Spanne des Basiswerts berechnet.

Vorteile

- Extraktion der wichtigsten Handelssignale aus dem Kurs mithilfe der Kompressionstechnik, um die Gewinnwahrscheinlichkeit zu erhöhen

- Mehrfache Indikatorbestätigung zur Vermeidung von Fehlausbrüchen und präzisen Trendrichtungserkennung

- Dynamische Stop-Loss- und Take-Profit-Einstellungen für eine risikokontrollierte Trendfolge

- Volatilitätsindikator stellt sicher, dass Trades in Umgebungen mit hoher Volatilität ausgeführt werden

- Mehrere Zeitrahmen-Analyse zur Erhöhung der Stabilität der Strategie

Risiken

- Der Boom-Hunter-Indikator kann durch Kompressionsverzerrungen falsche Signale erzeugen

- Die Mittellinie des Hull-Suites kann zeitlich verzögert sein und Kursänderungen nicht rechtzeitig verfolgen

- Bei sinkender Volatilität können Handelsmöglichkeiten verpasst werden oder Verlustglattstellungen ausgelöst werden

Lösungsansätze:

- Anpassung der Parameter des Kompressionsindikators, um die Empfindlichkeit auszugleichen

- Verwendung exponentieller gleitender Durchschnitte (wie EHMA) als Ersatz für die Mittellinie

- Hinzufügen weiterer Bestätigungsindikatoren, um Fehlleitungen der Volatilität zu vermeiden

Optimierung

Die Strategie kann in folgenden Bereichen optimiert werden:

-

Parameteroptimierung: Durch Änderung der Indikatorparameter wie Periodenlängen, Kompressionskoeffizienten usw. die optimale Parameterkombination ermitteln

-

Zeitrahmenoptimierung: Testen verschiedener Zeitrahmen (1 Minute, 5 Minuten, 30 Minuten usw.), um den am besten geeigneten Handelszeitrahmen zu finden

-

Positionsgrößenoptimierung: Änderung der Positionsgröße und des Anteils pro Trade, um die optimale Kapitalnutzung zu erzielen

-

Stop-Loss-Optimierung: Anpassung der Stop-Loss-Positionen je nach Handelspaar, um das beste Risiko-Ertrags-Verhältnis zu erreichen

-

Bedingungsoptimierung: Hinzufügen oder Entfernen von Filterbedingungen, um einen präziseren Einstiegszeitpunkt zu erhalten

Zusammenfassung

Diese Strategie kombiniert die drei Indikatoren Boom Hunter, Hull Suite und Volatility Oscillator, um einen Trendfolgehandel über mehrere Zeitrahmen zu ermöglichen. Sie kann plötzliche Kursbewegungen effektiv erkennen und eignet sich für digitale Vermögenswerte mit hoher Volatilität. Die Strategie bietet eine kontrollierte Risikosteuerung und ist durch Optimierungen in den Bereichen Parameter, Filterbedingungen und Stop-Loss äußerst praxistauglich und erweiterbar.

- 1