Kuberan-Strategie: Die Konvergenzstrategie der Marktbeherrschung

Strategieüberblick

Die Kuberan-Strategie ist eine leistungsstarke Handelsstrategie, die von Kathir entwickelt wurde. Sie vereint verschiedene Analysetechniken zu einem einzigartigen und wirkungsvollen Handelsansatz. Benannt nach dem Gott des Reichtums Kuberan, symbolisiert die Strategie ihr Ziel, die Portfolios der Trader zu bereichern.

Kuberan ist nicht nur eine Strategie, sondern ein umfassendes Handelssystem. Es kombiniert Trendanalyse, Momentum-Indikatoren und Volumenindikatoren, um Handelsmöglichkeiten mit hoher Wahrscheinlichkeit zu identifizieren. Durch die Nutzung der Synergien dieser Elemente liefert Kuberan klare Einstiegs- und Ausstiegssignale, die für Trader aller Erfahrungsstufen geeignet sind.

Funktionsweise der Strategie

Das Herzstück der Kuberan-Strategie ist das Prinzip der mehrfachen Indikatorkonvergenz. Sie nutzt eine einzigartige Kombination von Indikatoren, die zusammenarbeiten, um Rauschen und Fehlsignale zu reduzieren. Konkret verwendet die Strategie die folgenden Schlüsselkomponenten:

- Trendrichtungsbestimmung: Durch den Vergleich des aktuellen Kurses mit Unterstützungs- und Widerstandsniveaus wird die aktuelle Trendrichtung bestimmt.

- Unterstützungs- und Widerstandsniveaus: Mithilfe des Zigzag-Indikators und Pivot-Punkten werden wichtige Unterstützungs- und Widerstandsniveaus identifiziert.

- Divergenz-Erkennung: Durch den Vergleich der Kursentwicklung mit dem Momentum-Indikator wird festgestellt, ob eine Divergenz vorliegt, die auf eine mögliche Trendumkehr hindeutet.

- Volatilitätsanpassung: Der ATR-Indikator wird verwendet, um den Stop-Loss dynamisch an die aktuelle Marktvolatilität anzupassen.

- Kerzenformationen: Bestimmte Candlestick-Muster bestätigen Trend- und Umkehrsignale.

Durch die ganzheitliche Berücksichtigung dieser Faktoren kann sich die Kuberan-Strategie in verschiedenen Marktumgebungen selbst anpassen und Handelsmöglichkeiten mit hoher Wahrscheinlichkeit erfassen.

Strategievorteile

- Mehrfache Indikatorkonvergenz: Die Kuberan-Strategie nutzt die Synergien mehrerer Indikatoren, was die Zuverlässigkeit der Signale erheblich erhöht und Rauschen reduziert.

- Hohe Anpassungsfähigkeit: Durch die dynamische Anpassung der Parameter kann sich die Strategie an wechselnde Marktbedingungen anpassen und bleibt länger effektiv.

- Klare Signale: Kuberan liefert eindeutige Ein- und Ausstiegssignale und vereinfacht den Handelsentscheidungsprozess.

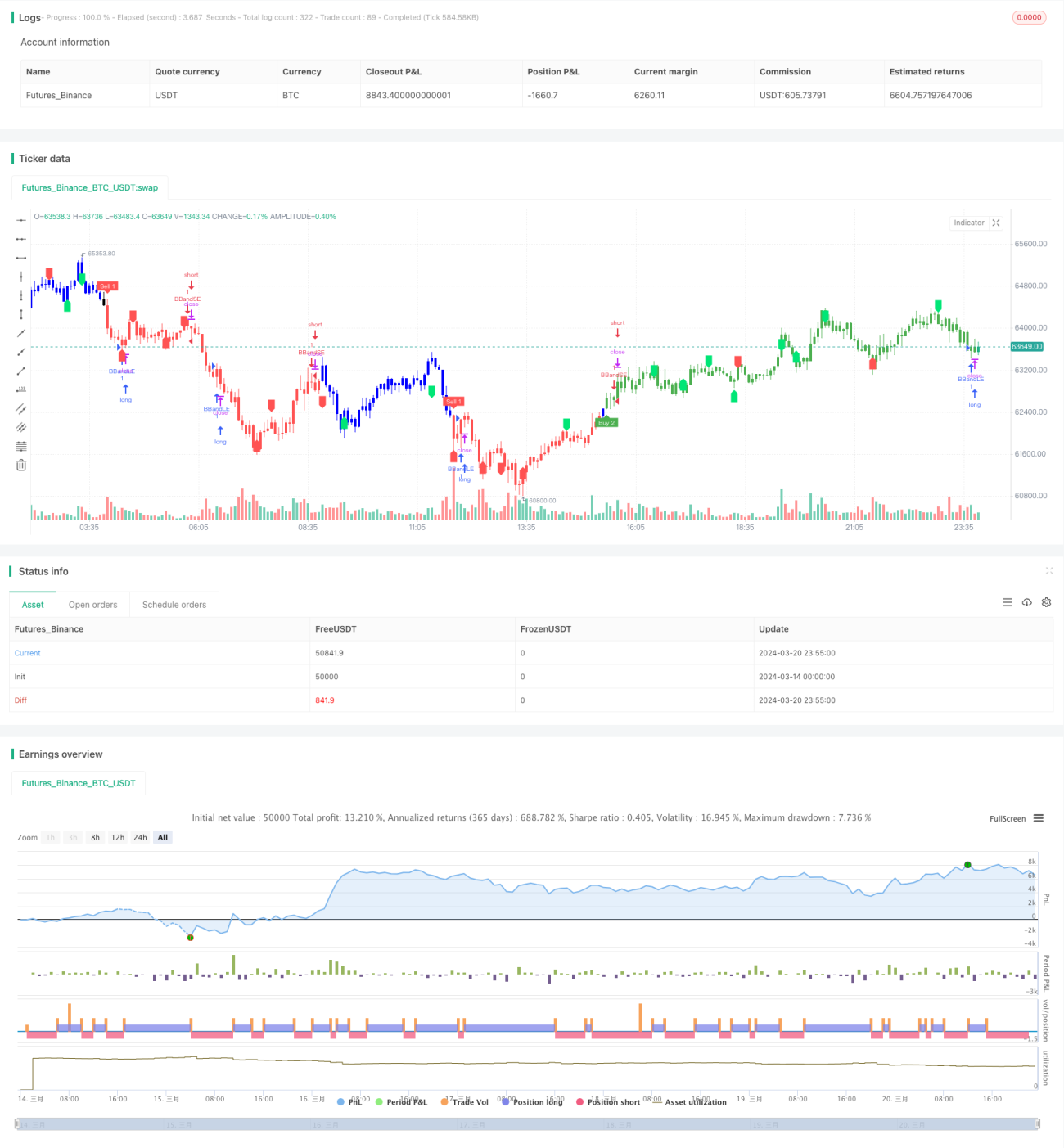

- Robuste Backtests: Die Strategie wurde strengen historischen Backtests unterzogen und zeigt in verschiedenen Marktphasen eine stabile Performance.

- Breite Anwendbarkeit: Kuberan eignet sich für viele Märkte und Instrumente und ist nicht auf bestimmte Handelsobjekte beschränkt.

Strategierisiken

- Parameterempfindlichkeit: Die Performance der Kuberan-Strategie reagiert empfindlich auf die Parameterwahl; ungeeignete Parameter können zu einer schlechteren Performance führen.

- Unerwartete Ereignisse: Die Strategie basiert hauptsächlich auf technischen Signalen und kann nur begrenzt auf fundamentale Ad-hoc-Ereignisse reagieren.

- Überanpassungsrisiko: Wenn bei der Parameteroptimierung zu viele historische Daten berücksichtigt werden, kann die Strategie zu stark an die Vergangenheit angepasst sein und sich an zukünftige Marktbewegungen schlechter anpassen.

- Hebelrisiko: Bei übermäßigem Hebeleinsatz besteht bei größeren Drawdowns die Gefahr der Liquidation.

Gegen diese Risiken können geeignete Kontrollmaßnahmen ergriffen werden, z. B. regelmäßige Parameteranpassung, angemessene Stop-Loss-Setzung, moderater Hebeleinsatz und Beachtung fundamentaler Veränderungen.

Optimierungsrichtungen

- Maschinelles Lernen: Durch die Einführung von ML-Algorithmen können die Strategieparameter dynamisch optimiert und die Anpassungsfähigkeit erhöht werden.

- Einbeziehung fundamentaler Faktoren: Die Integration der Fundamentalanalyse in Handelsentscheidungen kann Situationen abdecken, in denen technische Signale versagen.

- Portfoliomanagement: Auf der Ebene des Geldmanagements kann die Kuberan-Strategie in ein Portfolio eingebunden werden, um eine effektive Absicherung mit anderen Strategien zu erreichen.

- Marktsegmentoptimierung: Anpassung und Optimierung der Strategieparameter spezifisch für die Eigenschaften verschiedener Marktinstrumente.

- Hochfrequenz-Umbau: Umbau der Strategie zu einer Hochfrequenzhandelsversion, um mehr kurzfristige Handelsmöglichkeiten zu erfassen.

Fazit

Kuberan ist eine leistungsstarke, sichere und zuverlässige Handelsstrategie. Sie vereint geschickt mehrere technische Analysemethoden und zeichnet sich durch das Prinzip der Indikatorkonvergenz sowohl bei der Trendidentifikation als auch bei der Erkennung von Wendepunkten aus. Obwohl jede Strategie unvermeidlich Risiken birgt, hat Kuberan in Backtests seine Robustheit bewiesen. Durch angemessene Risikokontrolle und Optimierungsmaßnahmen kann die Strategie Händlern helfen, im Marktwettbewerb die Oberhand zu gewinnen und das langfristige, stabile Wachstum des Portfolios voranzutreiben.

/*backtest

start: 2024-03-14 00:00:00

end: 2024-03-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue- 1