Estrategia de trading bidireccional de cruce de medias móviles

Resumen

Esta estrategia calcula medias móviles de diferentes períodos y genera señales de trading cuando la media móvil de período más corto cruza por encima de la de período más largo. Es una estrategia típica de cruce de medias móviles. La estrategia admite tanto posiciones largas como cortas, permitiendo operar en ambas direcciones.

Principio de la Estrategia

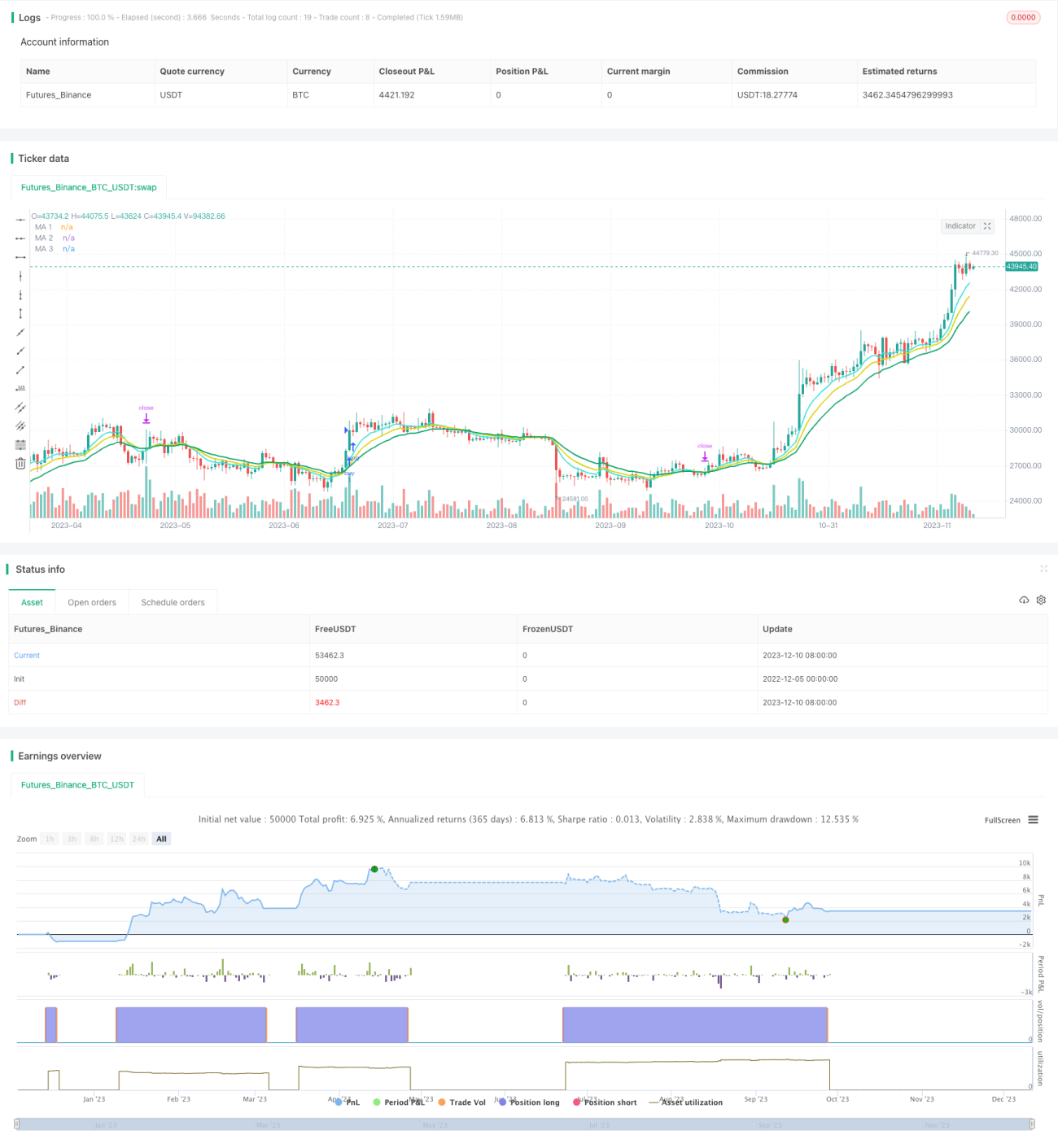

La estrategia se basa en los cruces entre medias móviles de diferentes períodos para determinar la tendencia del mercado y generar señales de trading. Utiliza tres medias móviles de 8, 13 y 21 períodos, donde la de 8 períodos es la de ciclo más corto y la de 21 períodos la de ciclo más largo. Cuando la media de 8 períodos cruza por encima de la de 21 períodos, se genera una señal de largo; cuando cruza por debajo, se genera una señal de corto.

En la ejecución concreta de las operaciones, la estrategia añade una condición de filtro para evitar quedar atrapado en mercados laterales. Solo se realiza la orden cuando el precio de cierre de la vela es superior (para señal larga) o inferior (para señal corta) al punto de cruce. Esto ayuda a filtrar señales falsas en parte.

Ventajas de la Estrategia

- Aplica el principio de cruce de medias móviles, lo que permite seguir eficazmente la tendencia del mercado.

- Incluye una condición de filtro que reduce señales falsas y evita quedar atrapado.

- Admite operaciones en ambas direcciones, pudiendo obtener ganancias tanto en mercados alcistas como bajistas.

- Utiliza cruces entre medias móviles de diferentes ciclos, capturando giros en marcos temporales mayores.

- La lógica de la estrategia es simple y clara, fácil de entender, modificar y optimizar.

Riesgos de la Estrategia

- En mercados muy volátiles y laterales puede fallar y generar muchas señales falsas.

- No puede tomar decisiones cuando el precio se mueve lateralmente, perdiendo algunas oportunidades.

- Los cruces entre diferentes ciclos presentan cierto retraso, lo que puede impedir capturar giros de tendencia a corto plazo.

- No considera la volatilidad del precio, por lo que los parámetros pueden necesitar ajustes según la volatilidad.

- No cuenta con stop loss ni take profit, lo que implica riesgo de pérdidas ilimitadas.

Soluciones a los Riesgos

- Combinar con otros indicadores para identificar el tipo de mercado y evitar el impacto de los movimientos laterales.

- Reducir los períodos de las medias móviles para aumentar la sensibilidad de las señales.

- Incorporar mecanismos de stop loss y take profit para controlar estrictamente el riesgo y la reducción de beneficios.

Direcciones de Optimización

- Combinar con otros indicadores técnicos como MACD, KDJ, etc., para mejorar la efectividad.

- Probar diferentes configuraciones de parámetros para evaluar su impacto en el rendimiento global de la estrategia.

- Adaptar los parámetros de forma dinámica según el tipo de mercado y la volatilidad.

- Optimizar el cálculo de las medias móviles utilizando indicadores como DEMA, ZLEMA, etc.

- Añadir lógica de stop loss y take profit.

- Realizar optimización cuantitativa de las métricas de backtesting para determinar los parámetros óptimos.

Resumen

La estrategia tiene un planteamiento claro: determina la relación de tendencia entre ciclos cortos y largos mediante el cruce simple y efectivo de medias móviles, capturando oportunidades de rotación. Permite operar en ambas direcciones, y es fácil de entender y optimizar. Sin embargo, presenta algunos riesgos que requieren mejoras, como la incapacidad de manejar eficazmente ciertos tipos de mercado y la falta de stop loss/take profit para controlar el riesgo. Mediante la combinación futura con otros indicadores técnicos y la optimización de parámetros, se puede mejorar aún más la estabilidad y rentabilidad de la estrategia.

- 1