Estrategia de seguimiento de bajo riesgo con pirámide de puntos bajos

Esta estrategia identifica posibles puntos bajos en los movimientos de precios mediante la combinación de diferentes indicadores, y reduce el riesgo mediante la construcción gradual de posiciones con un sistema de pirámide de seguimiento. Además, integra funciones como stop loss, take profit y stop loss móvil, lo que permite un control eficaz del riesgo.

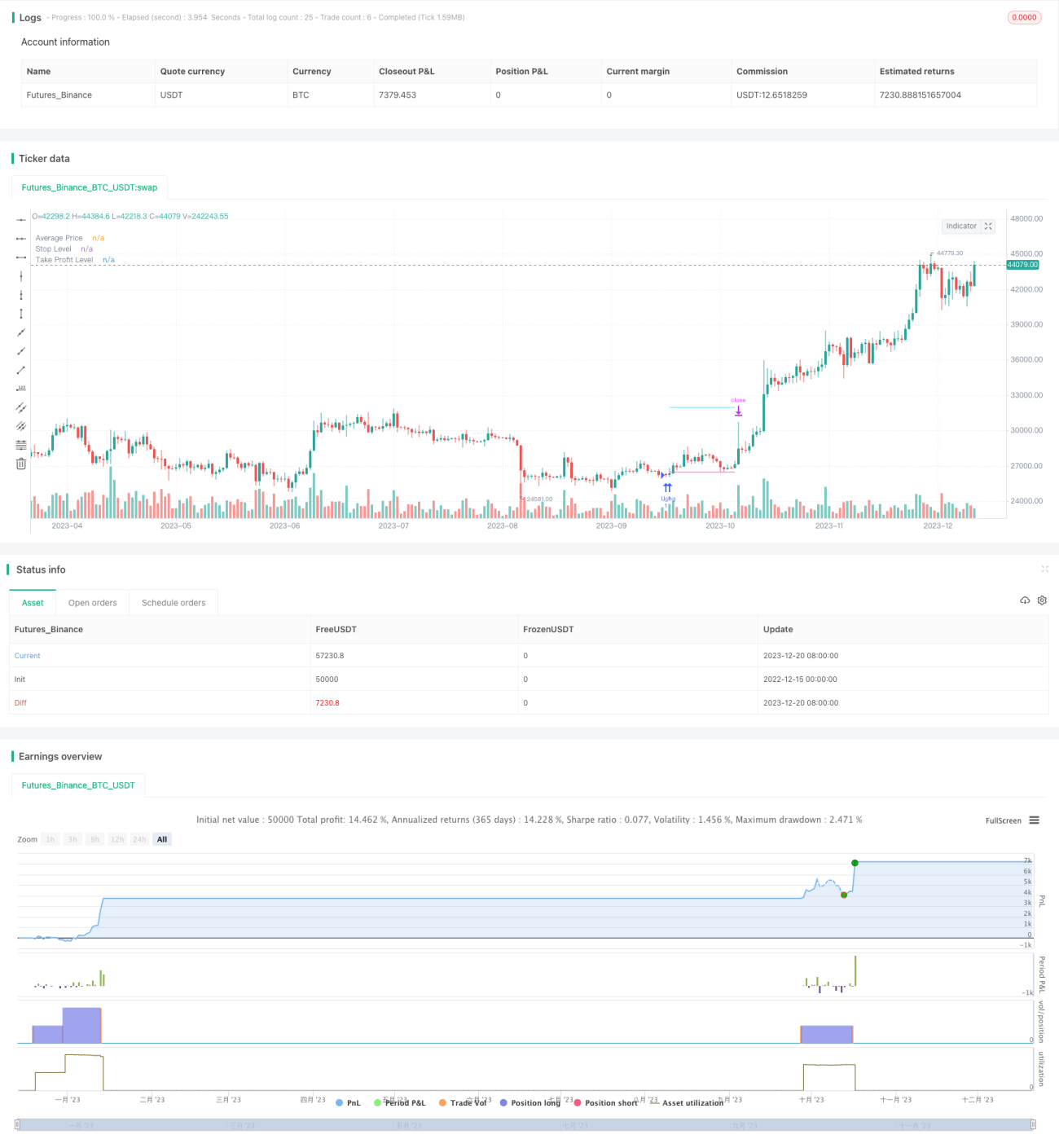

Resumen de la estrategia

La estrategia utiliza primero la diferencia entre el RSI y el EMA del RSI para identificar posibles puntos bajos en el precio. Para filtrar señales falsas, también combina medias móviles y un oscilador estocástico de múltiples marcos temporales como confirmación. Una vez confirmada la señal de punto bajo, se abren posiciones largas de forma gradual en un nivel ligeramente inferior a ese punto, lo que constituye el enfoque de la pirámide de seguimiento. La estrategia permite abrir hasta 12 órdenes de seguimiento, y la cantidad de cada orden aumenta de forma secuencial, lo que dispersa eficazmente el riesgo. Todas las órdenes siguen un stop loss general para cerrar posiciones, y también se permite establecer un take profit independiente para cada orden. Para un mayor control del riesgo, la estrategia incluye un stop loss general basado en un porcentaje del patrimonio de la cuenta.

Principio de la estrategia

La estrategia se compone principalmente de tres módulos: el módulo de identificación de puntos bajos, el módulo de pirámide de seguimiento y el módulo de control de riesgo.

Módulo de identificación de puntos bajos: Utiliza la diferencia entre el RSI y su EMA para identificar posibles puntos bajos en el precio. Para mejorar la precisión, se introducen indicadores de media móvil y un oscilador estocástico de múltiples marcos temporales para filtrar señales. Solo cuando el precio está por debajo de la media móvil y la línea K del estocástico está por debajo de 30 se confirma la validez de la señal de punto bajo.

Módulo de pirámide de seguimiento: Es el núcleo de la estrategia. Una vez confirmada la señal de punto bajo, la estrategia abre la primera orden en un nivel 0,1% por debajo de ese punto bajo. Luego, si el precio continúa cayendo y está por debajo del precio de entrada promedio en un cierto porcentaje, se añaden más órdenes largas. La cantidad de nuevas órdenes aumenta secuencialmente; por ejemplo, la tercera orden tiene 3 veces la cantidad de la primera. Este enfoque de pirámide promedia el riesgo. La estrategia permite hasta 12 órdenes de seguimiento.

Módulo de control de riesgo: Incluye principalmente tres aspectos. Primero, el stop loss general, calculado en función del precio más alto de un período reciente determinado. Todas las órdenes siguen este stop loss para cerrar simultáneamente. Segundo, el take profit independiente para cada orden, permitiendo un cierre basado en un porcentaje del precio de entrada. Tercero, el stop loss general basado en un porcentaje del patrimonio de la cuenta, que es la medida de control de riesgo más fuerte.

Ventajas de la estrategia

- Reduce el riesgo de órdenes individuales mediante la pirámide de seguimiento, dispersando el riesgo general.

- La combinación de múltiples indicadores mejora la precisión en la identificación de puntos bajos.

- Las funciones de stop loss general, take profit y stop loss móvil controlan eficazmente el riesgo.

- El mecanismo de stop loss basado en el porcentaje del patrimonio protege la cuenta de pérdidas significativas.

- Permite ajustar parámetros para encontrar un equilibrio entre riesgo y rentabilidad.

Riesgos de la estrategia

- La precisión en la identificación de puntos bajos aún tiene limitaciones; puede perderse el mejor punto de entrada o caer en señales falsas.

- Al añadir órdenes, se puede enfrentar a movimientos adversos del mercado, agravando las pérdidas.

- Se necesita un período de operación más largo para que la estrategia muestre sus ventajas.

- Una configuración inadecuada de parámetros puede llevar a un control de riesgo insuficiente.

Para mitigar los riesgos anteriores, se pueden optimizar los siguientes aspectos:

- Cambiar o agregar indicadores para mejorar la precisión en la identificación de puntos bajos.

- Optimizar parámetros como la cantidad de órdenes, el intervalo y el porcentaje de take profit para reducir el riesgo de cada orden individual.

- Reducir adecuadamente el margen de stop loss para proteger las ganancias.

- Probar diferentes instrumentos, eligiendo aquellos con buena liquidez y alta volatilidad.

Direcciones de optimización de la estrategia

La estrategia aún tiene margen para una mayor optimización:

- Introducir técnicas más avanzadas, como el aprendizaje automático, para identificar puntos bajos.

- Ajustar dinámicamente la cantidad de órdenes, el margen de stop loss, etc., según las condiciones del mercado.

- Agregar una estrategia de stop loss dentro de la banda para evitar que las pérdidas se amplíen.

- Incorporar un mecanismo de reingreso.

- Optimizar los parámetros de la estrategia para acciones y criptomonedas.

Resumen

Esta estrategia reduce eficazmente el riesgo de las órdenes individuales mediante el enfoque de pirámide de seguimiento, y las funciones de stop loss general, take profit y stop loss móvil también proporcionan un buen control del riesgo. Sin embargo, todavía hay espacio para optimizar en aspectos como la identificación de puntos bajos. Si se introducen tecnologías más avanzadas, se añade la capacidad de ajuste dinámico de parámetros y se optimizan los parámetros, la relación rentabilidad-riesgo de esta estrategia mejorará significativamente.

- 1