Estrategia combinada de Bandas de Bollinger (contracción) y RSI

Resumen

Esta estrategia combina las Bandas de Bollinger y el Índice de Fuerza Relativa (RSI) para identificar oportunidades de contracción de las Bandas de Bollinger acompañadas de un aumento del RSI, utilizando un stop-loss de seguimiento de tendencia para controlar el riesgo.

Principio de la Estrategia

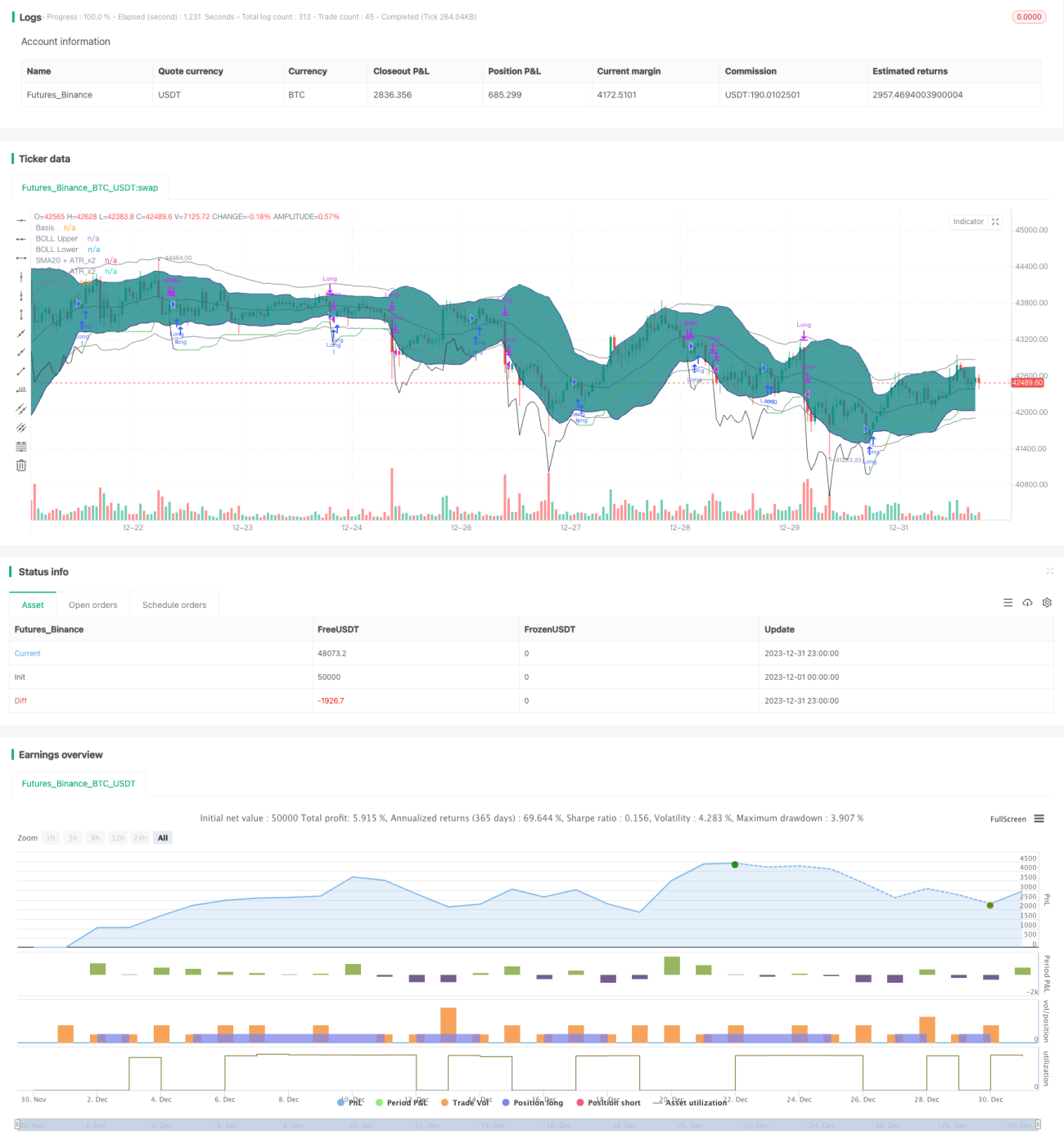

El núcleo de la lógica de trading de esta estrategia radica en identificar la contracción de las Bandas de Bollinger y, cuando el RSI muestra una tendencia alcista, determinar que la tendencia se encuentra en una fase temprana de subida. Específicamente, cuando la desviación estándar de la banda media de las Bandas de Bollinger de 20 días es menor que ATR * 2, consideramos que se ha producido una contracción. Al mismo tiempo, si tanto el RSI de 10 días como el de 14 días muestran una tendencia alcista, predecimos que el precio está a punto de superar la banda superior de Bollinger y adoptamos una estrategia larga.

Una vez dentro del mercado, utilizamos una distancia de seguridad basada en ATR más un stop-loss que se ajusta al alza con el precio para asegurar ganancias y controlar el riesgo. Cerramos la posición cuando el precio supera la línea de stop-loss o cuando el RSI está sobrecalentado (RSI de 14 días superior a 70, y RSI de 10 días superior al de 14 días).

Análisis de Ventajas

La mayor ventaja de esta estrategia es utilizar la contracción de las Bandas de Bollinger para identificar períodos de consolidación del mercado, combinada con el indicador RSI para predecir la dirección de la ruptura del precio. Además, se emplea un stop-loss adaptativo en lugar de fijo, que se ajusta de manera flexible según la volatilidad del mercado, logrando así mayores rendimientos bajo un control de riesgo garantizado.

Análisis de Riesgos

El principal riesgo de esta estrategia es que, al identificar la contracción de las Bandas de Bollinger y el aumento del RSI, la ruptura del precio podría ser una falsa ruptura. Además, en términos de stop-loss, si la volatilidad es demasiado alta, el stop-loss adaptativo podría no activarse a tiempo. Este riesgo se puede mitigar mejorando el método de stop-loss (por ejemplo, stop-loss curvilíneo).

Direcciones de Optimización

Esta estrategia se puede optimizar en los siguientes aspectos:

- Mejorar la configuración de los parámetros de las Bandas de Bollinger para optimizar el efecto de detección de contracción.

- Probar diferentes períodos del RSI.

- Evaluar el efecto de otros métodos de stop-loss (stop-loss curvilíneo, stop-loss retrospectivo, etc.).

- Ajustar los parámetros según las características de los diferentes instrumentos.

Resumen

Esta estrategia aprovecha la complementariedad de las Bandas de Bollinger y el RSI para obtener una buena relación entre drawdown y rendimiento bajo un control de riesgo. Posteriormente, se puede optimizar en aspectos como el método de stop-loss y la selección de parámetros para hacerla más adecuada para diferentes instrumentos de trading.

- 1