Estrategia de referencia de tendencia alcista de ruptura

Resumen

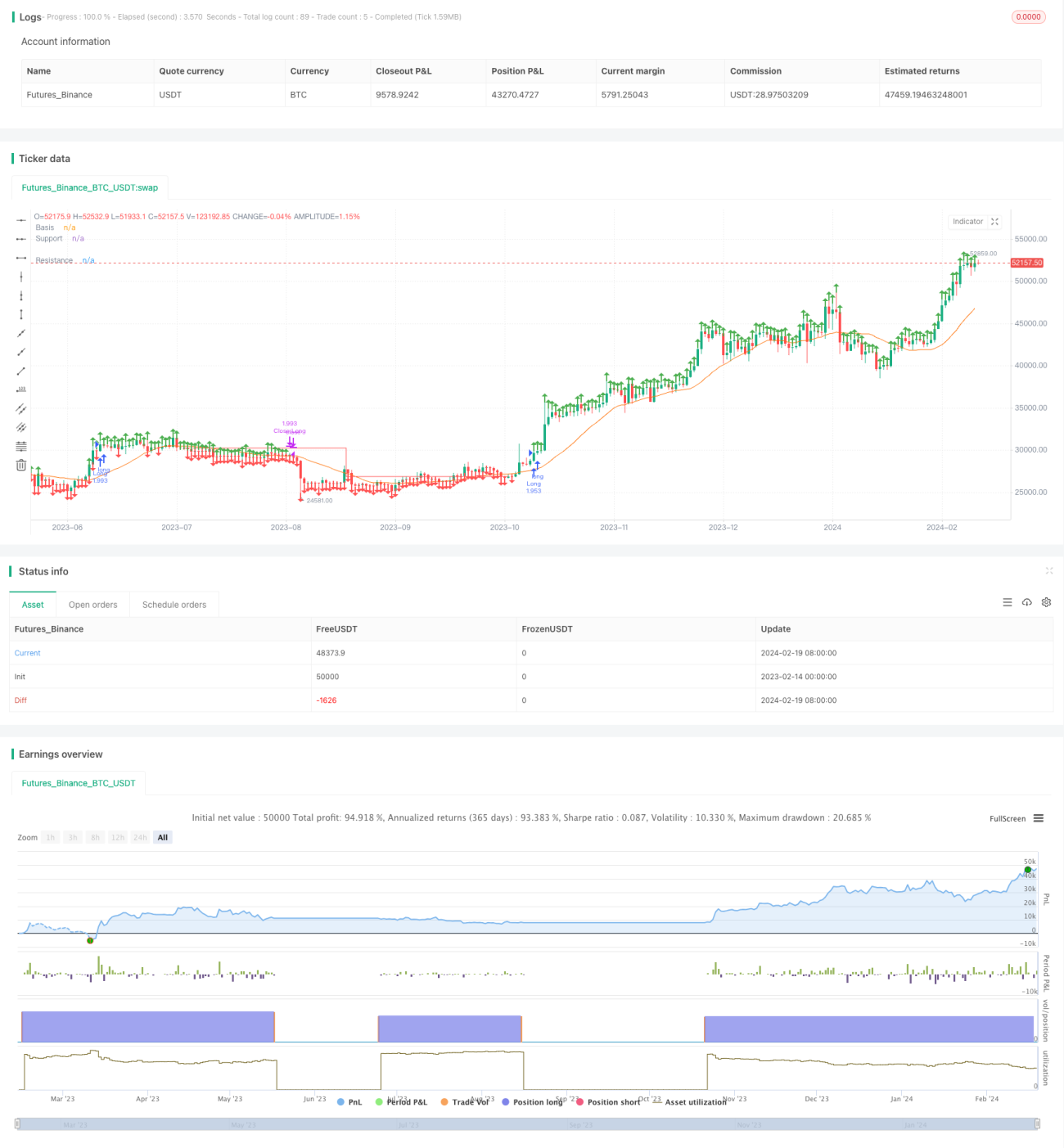

Esta estrategia es una estrategia de tenencia a largo plazo basada en una media móvil simple para determinar la dirección de la tendencia, combinada con líneas de resistencia y soporte para generar señales de ruptura. Al calcular los puntos máximos (Pivot High) y mínimos (Pivot Low) del precio, se dibujan líneas de resistencia y soporte. Cuando el precio supera la línea de resistencia, se toma una posición larga; cuando rompe la línea de soporte, se cierra la posición. Esta estrategia es adecuada para acciones con tendencias claras y puede ofrecer una buena relación riesgo-beneficio.

Principio de la estrategia

- Se calcula una media móvil simple de 20 días como línea de referencia para determinar la tendencia.

- Se calculan los puntos máximos (Pivot High) y mínimos (Pivot Low) según los parámetros definidos por el usuario.

- Se dibujan las líneas de resistencia y soporte con base en los puntos máximos y mínimos.

- Cuando el precio de cierre es superior a la línea de resistencia, se entra en largo.

- Cuando la línea de soporte cruza por debajo de la línea de resistencia, se cierra la posición.

La estrategia utiliza la media móvil simple para juzgar la dirección general de la tendencia y luego utiliza las rupturas de puntos clave para generar señales de trading, lo que la convierte en una estrategia típica de ruptura. Al combinar puntos clave con el juicio de tendencia, se pueden filtrar eficazmente las falsas rupturas.

Análisis de ventajas

- La estrategia ofrece suficientes oportunidades, adecuada para acciones de alta volatilidad y fácil de capturar tendencias.

- Control de riesgo eficiente, con una alta relación riesgo-beneficio.

- Utiliza señales de ruptura para evitar el riesgo de falsas rupturas.

- Parámetros personalizables, alta adaptabilidad.

Análisis de riesgos

- Depende de la optimización de parámetros; una selección inadecuada puede aumentar la probabilidad de falsas rupturas.

- Las señales de ruptura tienen retraso, lo que puede hacer que se pierdan algunas oportunidades.

- En mercados laterales o de rango, es fácil que se activen los stops.

- Si el ajuste de la línea de soporte no es oportuno, puede generar pérdidas.

Se puede reducir el riesgo mediante la optimización de parámetros en trading real y la combinación de estrategias de stop-loss y take-profit.

Direcciones de optimización

- Optimizar el período de la media móvil.

- Optimizar los parámetros de las líneas de soporte y resistencia.

- Añadir estrategias de stop-loss y take-profit.

- Incorporar mecanismos de confirmación de ruptura.

- Filtrar señales combinando indicadores como el volumen de negociación.

Conclusión

En general, esta estrategia es una estrategia típica de ruptura, que depende de la optimización de parámetros y la liquidez, adecuada para traders que buscan seguir tendencias. Como marco de referencia, se puede expandir modularmente según las necesidades reales, reduciendo el riesgo y mejorando la estabilidad mediante mecanismos como stop-loss, take-profit y filtrado de señales.

- 1