Estrategia de seguimiento de tendencia con cruce DEMA

Resumen

Esta estrategia se basa en el cruce de la media móvil exponencial doble (DEMA) como señal de trading, adoptando un enfoque de seguimiento de tendencia y estableciendo automáticamente un stop loss y un take profit. Sus ventajas son señales de trading claras, configuración flexible de stop loss y take profit, y un control de riesgos eficaz.

Principio de la estrategia

-

Calcular la DEMA rápida (8 períodos), la DEMA lenta (24 períodos) y una DEMA auxiliar (configurable).

-

Cuando la DEMA rápida cruza al alza la DEMA lenta, generando una señal de cruce alcista, se abre una posición larga; cuando la DEMA rápida cruza a la baja la DEMA lenta, generando una señal de cruce bajista, se abre una posición corta.

-

Se añade un filtro de señales de trading: solo se genera una señal si el valor actual de la DEMA auxiliar es superior al del día anterior, evitando así falsas rupturas.

-

Se emplea un mecanismo de stop loss de seguimiento de tendencia, que ajusta la línea de stop loss según la evolución del precio, asegurando que el punto de stop loss bloquee parte de los beneficios.

-

Al mismo tiempo, se establecen un stop loss y un take profit de proporción fija para controlar la pérdida máxima y el beneficio máximo de cada operación individual.

Ventajas de la estrategia

-

Las señales de trading son claras, lo que facilita la identificación de los momentos de entrada y salida.

-

El algoritmo de DEMA doble es más suave, evita la sobreoptimización y las señales son más fiables.

-

El filtro con la línea auxiliar mejora la efectividad de las señales y reduce las señales falsas.

-

El uso de un stop loss de seguimiento de tendencia permite bloquear parte de los beneficios y controlar el riesgo de manera efectiva.

-

El establecimiento de un stop loss y un take profit de proporción fija controla la pérdida máxima por operación, evitando exceder el rango de riesgo.

Riesgos de la estrategia

-

En mercados laterales o de rango, puede generar operaciones frecuentes, aumentando la exposición y provocando pérdidas en la estrategia.

-

Si el stop loss fijo se configura con un porcentaje demasiado amplio, en condiciones de mercado anormales podría desencadenar un stop loss de gran magnitud.

-

La señal de cruce de la DEMA es rezagada; en mercados de movimientos rápidos, comprar cerca de los máximos del movimiento puede aumentar el riesgo de pérdidas.

-

Al implementar la estrategia en trading real, los costos de deslizamiento pueden afectar la rentabilidad, por lo que es necesario ajustar los parámetros de take profit y stop loss.

Optimización de la estrategia

-

Se pueden ajustar los parámetros de la DEMA según las condiciones del mercado para encontrar el punto óptimo de equilibrio.

-

En el trading real, se deben considerar los costos de deslizamiento y ampliar adecuadamente el rango del stop loss fijo.

-

Se pueden añadir otros indicadores auxiliares, como el MACD, para mejorar la efectividad de las señales.

-

Se puede configurar un valor de paso para el stop loss de seguimiento, optimizando la lógica del stop loss.

Conclusión

Esta estrategia aprovecha la capacidad de la DEMA para identificar tendencias, combinada con un mecanismo de seguimiento de tendencia para controlar el riesgo. Es un ejemplo muy representativo dentro de los sistemas de estrategias de trading que determinan la dirección de la tendencia. En general, la estrategia ofrece señales claras, un stop loss y take profit razonables, y es fácil de dominar y controlar los riesgos. Al implementarla en trading real, combinando la optimización de los costos de deslizamiento y la evaluación con indicadores auxiliares, se pueden obtener buenos retornos de inversión.

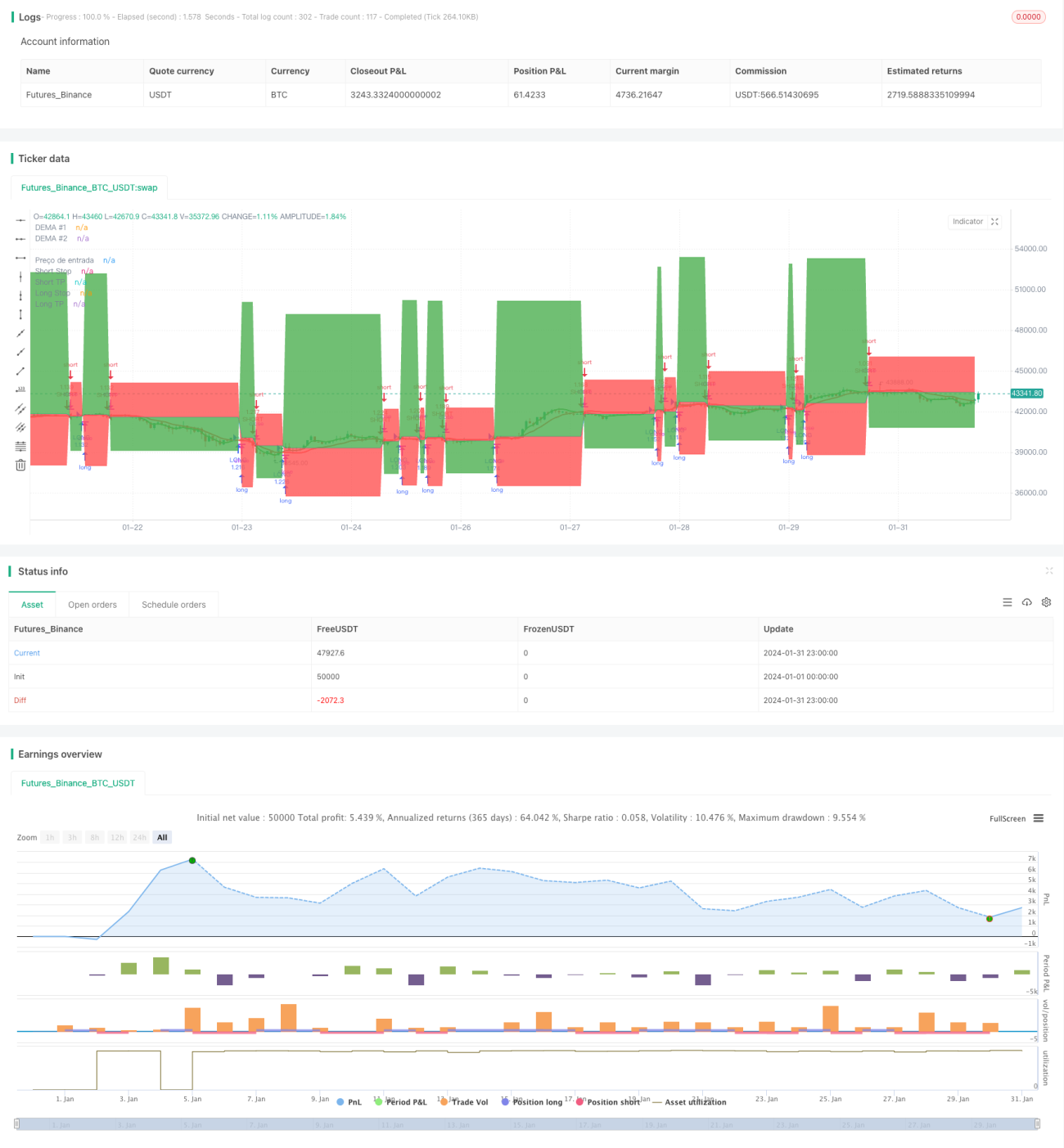

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1