Estrategia cuantitativa de seguimiento de tendencia dual

Resumen

La idea central de esta estrategia es combinar la estrategia de reversión 123 con el indicador oscilador arcoíris para lograr un doble seguimiento de tendencia, mejorando así la tasa de aciertos de la estrategia. Esta estrategia sigue las tendencias de precios a corto y mediano plazo, ajustando dinámicamente las posiciones para obtener rendimientos excesivos por encima del mercado.

Principio de la estrategia

La estrategia consta de dos partes:

-

Estrategia de reversión 123: Si el precio de cierre de los dos días anteriores bajó y el precio de cierre de hoy subió, y la línea lenta K de 9 días está por debajo de 50, se toma una posición larga; si el precio de cierre de los dos días anteriores subió y el precio de cierre de hoy bajó, y la línea rápida K de 9 días está por encima de 50, se toma una posición corta.

-

Indicador oscilador arcoíris: Este indicador refleja el grado de desviación del precio con respecto a la media móvil. Cuando el indicador supera 80, indica que el mercado tiende a la inestabilidad; cuando está por debajo de 20, indica que el mercado tiende a revertirse.

Esta estrategia combina ambos criterios: cuando aparecen señales simultáneas de compra y venta, se abre la posición; en caso contrario, se cierra.

Análisis de ventajas

La estrategia presenta las siguientes ventajas:

- Doble filtro: mejora la calidad de las señales y reduce la tasa de falsos positivos.

- Ajuste dinámico de posición: reduce las pérdidas en movimientos unidireccionales.

- Integración de indicadores de corto y mediano plazo: mejora la estabilidad de la estrategia.

Análisis de riesgos

La estrategia también conlleva los siguientes riesgos:

- Una optimización inadecuada de parámetros puede provocar sobreajuste.

- La doble apertura de posiciones incrementa los costos de transacción.

- En condiciones de volatilidad extrema del precio del activo, el stop loss puede ser fácilmente perforado.

Estos riesgos pueden mitigarse ajustando parámetros, optimizando la gestión de posiciones y estableciendo stop losses razonables.

Direcciones de optimización

La estrategia puede optimizarse en los siguientes aspectos:

- Optimizar los parámetros para encontrar la mejor combinación.

- Agregar un módulo de gestión de posición que ajuste dinámicamente el tamaño según la volatilidad y el drawdown.

- Incorporar un módulo de stop loss con stops móviles adecuados.

- Agregar algoritmos de aprendizaje automático para ayudar a identificar puntos de inflexión de tendencia.

Resumen

Esta estrategia integra la estrategia de reversión 123 y el indicador oscilador arcoíris para lograr un doble seguimiento de tendencia, manteniendo una estabilidad relativamente alta y ofreciendo cierto potencial de rendimiento excesivo. Con una optimización continua, se espera mejorar aún más la rentabilidad de la estrategia.

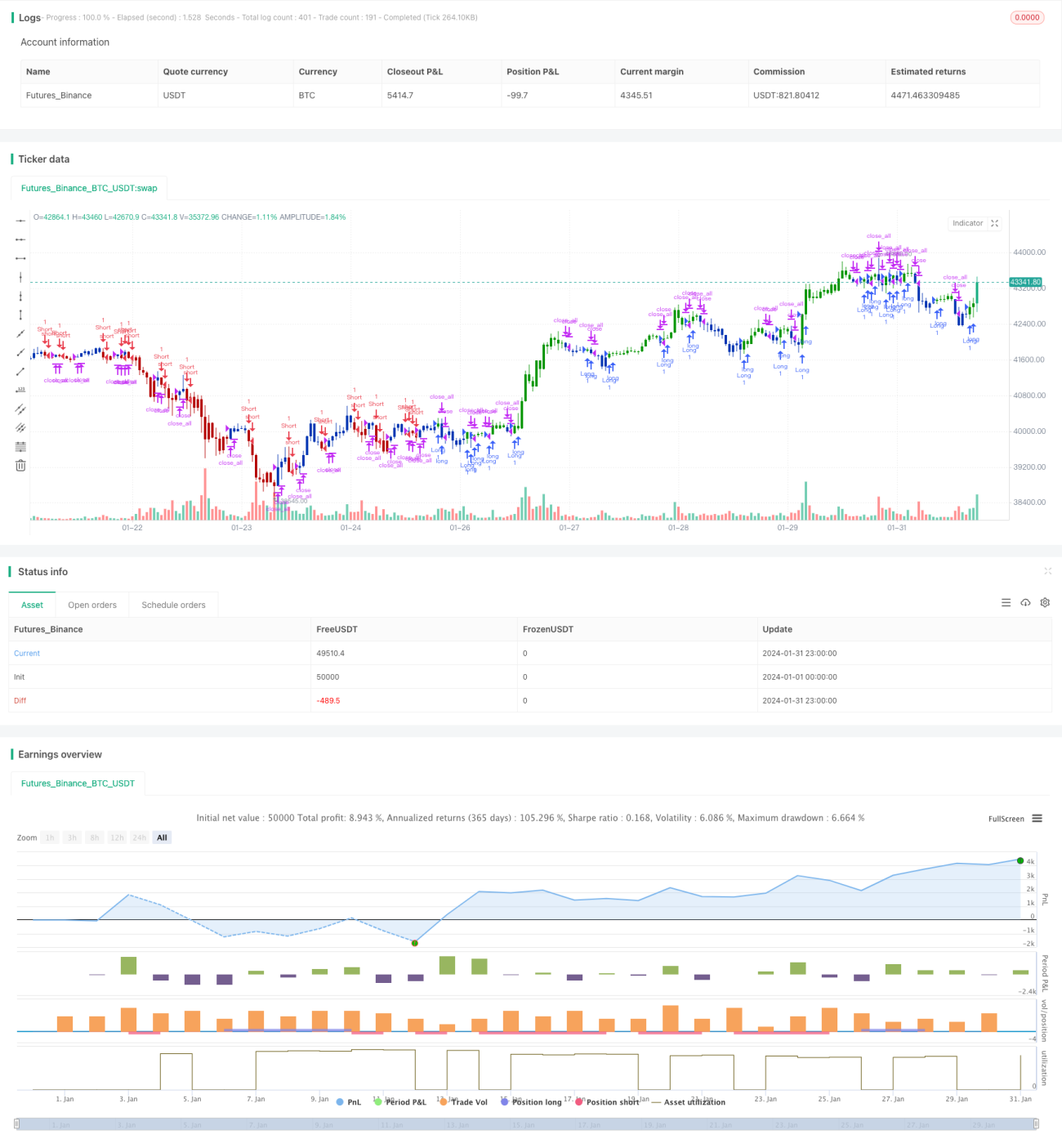

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/05/2021

// This is combo strategies for get a cumulative signal. - 1