Stratégie de suivi de tendance avec canal de triple moyenne mobile

Aperçu (Overview)

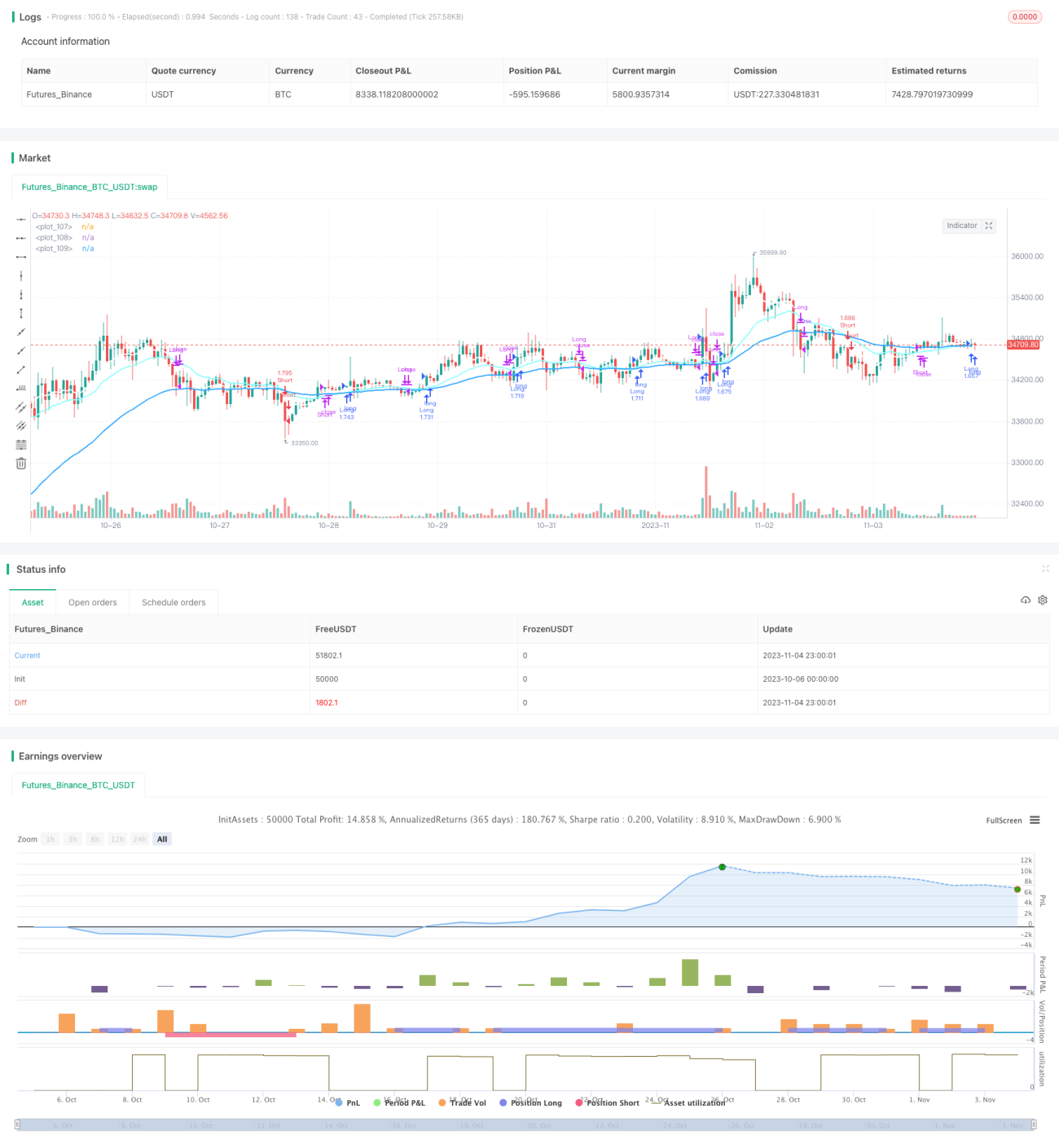

Cette stratégie utilise une combinaison de trois moyennes mobiles pour déterminer la direction de la tendance en fonction de leur ordre relatif, réalisant ainsi un suivi de tendance. Lorsque la moyenne mobile rapide, la moyenne mobile moyenne et la moyenne mobile lente sont alignées dans l'ordre décroissant, on prend une position longue ; lorsqu'elles sont alignées dans l'ordre croissant (lente, moyenne, rapide), on prend une position courte.

Principe de la stratégie (Strategy Principle)

La stratégie utilise trois moyennes mobiles de périodes différentes : une moyenne mobile rapide, une moyenne mobile moyenne et une moyenne mobile lente.

Conditions d'entrée :

- Position longue : lorsque moyenne mobile rapide > moyenne mobile moyenne > moyenne mobile lente, le marché est considéré en tendance haussière, on prend une position longue.

- Position courte : lorsque moyenne mobile lente < moyenne mobile moyenne < moyenne mobile rapide, le marché est considéré en tendance baissière, on prend une position courte.

Conditions de sortie :

- Sortie sur moyenne mobile : lorsque l'ordre des trois moyennes mobiles s'inverse, on ferme la position.

- Sortie sur stop-loss / take-profit : on fixe des niveaux de take-profit et stop-loss, par exemple un take-profit de 12 % et un stop-loss de 1 % ; la position est fermée lorsque le prix atteint l'un de ces niveaux.

Cette stratégie simple et directe utilise trois moyennes mobiles pour déterminer la direction de la tendance et réaliser un trading de suivi de tendance, adapté aux marchés présentant une tendance forte.

Analyse des avantages (Advantage Analysis)

- Utilisation de trois moyennes mobiles pour détecter la tendance, filtrant le bruit du marché et identifiant la direction.

- Des moyennes mobiles de différentes périodes permettent de mieux repérer les points de retournement de tendance.

- Combinaison des indicateurs de moyennes mobiles avec un take-profit/stop-loss fixe pour gérer le risque.

- Logique de stratégie simple et intuitive, facile à comprendre et à mettre en œuvre.

- Possibilité d'optimiser facilement les paramètres de période des moyennes mobiles pour s'adapter à différents horizons temporels.

Risques et améliorations (Risks and Improvements)

- Sur les grandes périodes, les moyennes mobiles peuvent générer davantage de faux signaux, entraînant des pertes inutiles.

- Envisager d'ajouter d'autres indicateurs ou conditions de filtrage pour améliorer le taux de gain.

- Optimiser la combinaison des périodes des moyennes mobiles pour s'adapter à un plus large éventail de conditions de marché.

- Intégrer des indicateurs de force de tendance pour éviter d'acheter au sommet ou de vendre au creux.

- Ajouter un stop-loss automatique pour éviter des pertes excessives.

Conclusion (Conclusion)

Cette stratégie de suivi de tendance basée sur trois moyennes mobiles a une logique claire et facile à comprendre, utilisant les moyennes mobiles pour identifier la direction de la tendance et réaliser un trading de suivi simple. Ses atouts résident dans sa simplicité de mise en œuvre et sa flexibilité grâce au réglage des paramètres de période pour s'adapter à différents contextes de marché. Cependant, elle comporte un certain risque de faux signaux, qui peut être atténué en ajoutant d'autres indicateurs ou conditions pour réduire les pertes inutiles et améliorer le taux de gain. Globalement, cette stratégie convient aux débutants intéressés par le trading de tendance pour apprendre et pratiquer.

- 1