Stratégie adaptative de take-profit et stop-loss basée sur un double timeframe et un indicateur de momentum

Aperçu

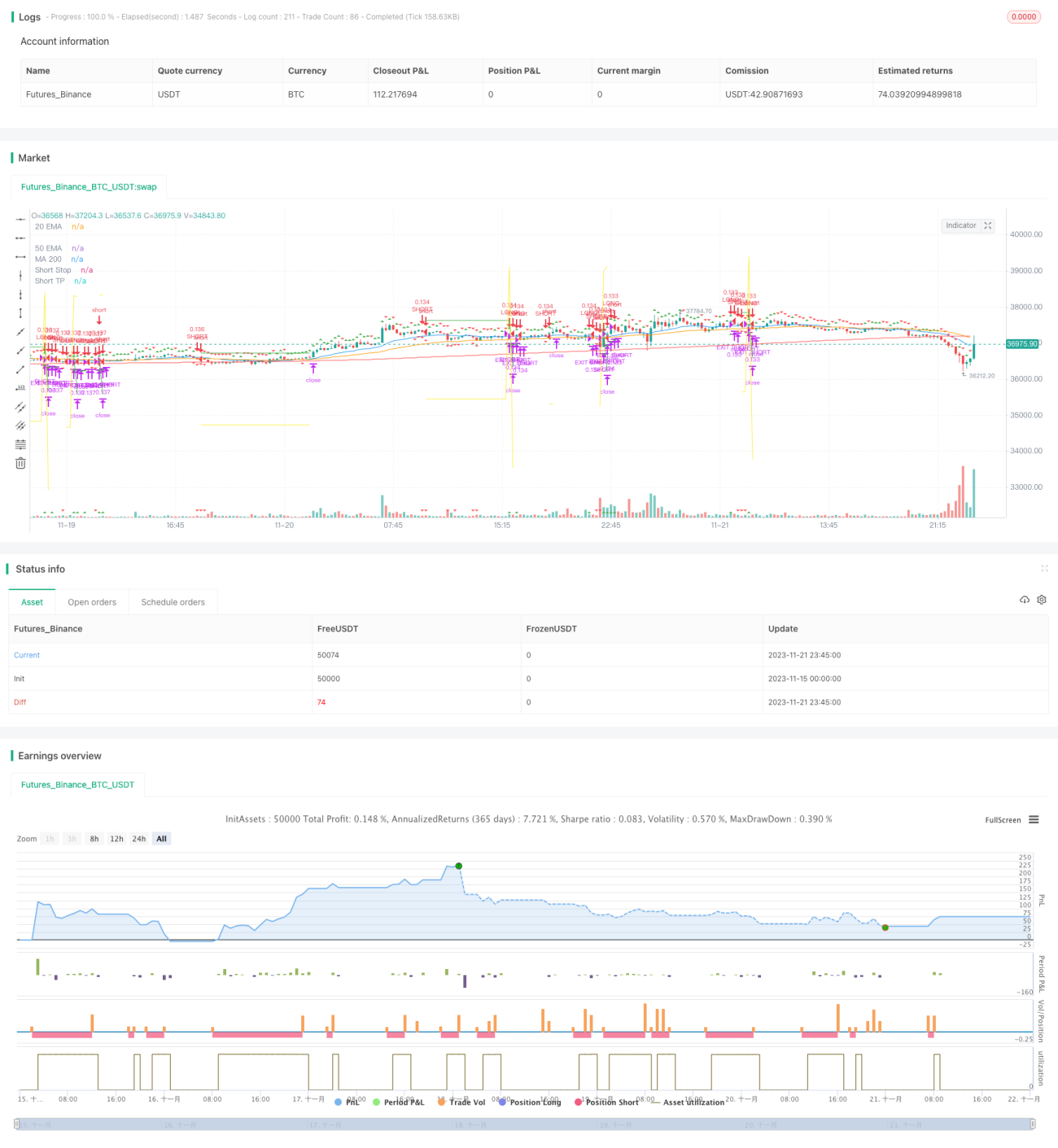

Cette stratégie combine un cadre temporel double et des indicateurs de momentum pour réaliser un take-profit et un stop-loss adaptatifs. Le cadre temporel principal surveille la direction de la tendance, tandis que le cadre temporel secondaire est utilisé pour confirmer les signaux. Lorsque les deux sont alignés, un signal de trading est généré. Après l'entrée en position, une méthode de take-profit progressif est utilisée pour mettre à jour les niveaux de take-profit et de stop-loss.

Principe de la stratégie

-

Le cadre temporel principal utilise l'indicateur de régression linéaire Squeeze Momentum (SQM) pour déterminer la tendance, tandis que le cadre temporel secondaire utilise une combinaison de moyennes mobiles exponentielles (EMA) de l'indicateur SQM pour filtrer les faux signaux.

-

Lorsque le SQM du graphique principal franchit à la hausse et que le SQM du graphique secondaire est également orienté à la hausse, on prend une position longue ; lorsque le SQM du graphique principal franchit à la baisse et que le SQM du graphique secondaire est également orienté à la baisse, on prend une position courte.

-

Après l'entrée, les niveaux initiaux de take-profit et de stop-loss sont définis selon les paramètres saisis. Lorsque le prix atteint le niveau de take-profit, les niveaux de take-profit et de stop-loss sont mis à jour. Concrètement, le take-profit augmente progressivement selon un ratio défini, tandis que le stop-loss diminue progressivement selon un ratio, réalisant ainsi un take-profit progressif.

Avantages de la stratégie

-

Le double cadre temporel filtre les faux signaux, garantissant la précision des signaux.

-

L'indicateur SQM détermine la direction de la tendance, évitant les interférences du bruit du marché.

-

Le mécanisme de take-profit et stop-loss adaptatif permet de verrouiller au maximum les gains et de contrôler efficacement les risques.

Analyse des risques

-

Un réglage inapproprié des paramètres de l'indicateur SQM peut entraîner des pertes en manquant les points de retournement de tendance.

-

Un choix inapproprié du cadre temporel secondaire peut ne pas filtrer efficacement le bruit, générant des transactions erronées.

-

Une amplitude de stop-loss trop large peut entraîner des pertes unitaires importantes.

Directions d'optimisation

-

Les paramètres de l'indicateur SQM doivent être ajustés en fonction des différents marchés pour garantir sa sensibilité.

-

Le cadre temporel secondaire doit également être testé sur différentes périodes afin de déterminer celle qui offre le meilleur filtrage.

-

L'amplitude du stop-loss peut être définie avec une plage de fluctuation plutôt qu'une valeur fixe, permettant ainsi de s'adapter à la volatilité du marché.

Conclusion

Dans l'ensemble, cette stratégie est très pratique : le double cadre temporel combiné à l'indicateur de momentum pour juger de la tendance, associé à un take-profit et stop-loss adaptatifs, permet de réaliser des bénéfices stables. En optimisant les paramètres de l'indicateur SQM, la période du graphique secondaire et le réglage de l'amplitude du stop-loss, l'efficacité de la stratégie peut être améliorée, ce qui la rend digne d'être appliquée et optimisée en trading réel.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1