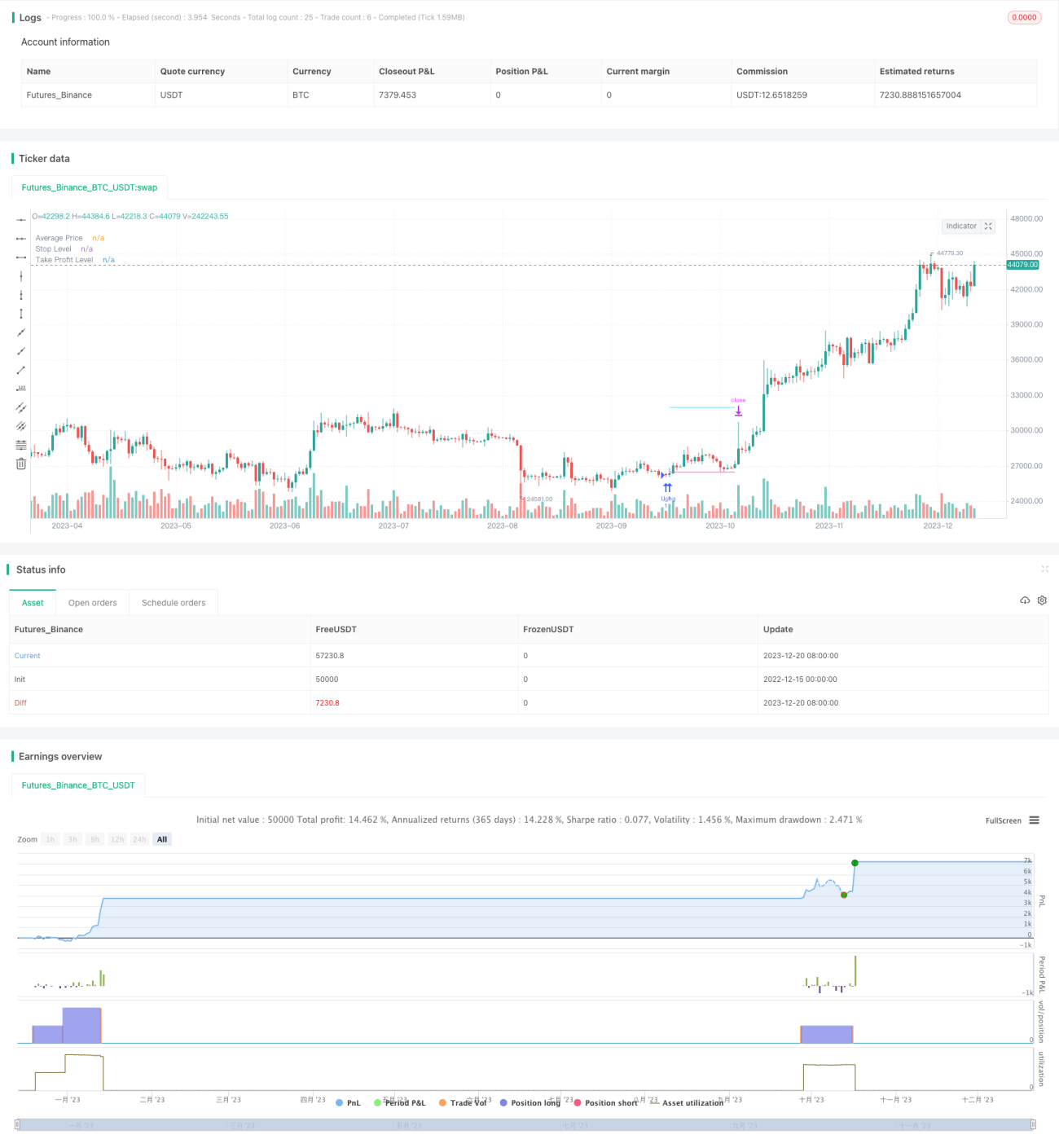

Stratégie de suivi à faible risque avec pyramide des points bas

Cette stratégie identifie les points bas potentiels dans les mouvements de prix en combinant différents indicateurs, et réduit les risques grâce à une approche de pyramide de suivi avec des entrées progressives. Elle intègre également des fonctions de stop-loss, take-profit et stop-loss suiveur pour un contrôle efficace des risques.

Aperçu de la stratégie

La stratégie utilise d'abord la différence entre le RSI et l'EMA du RSI pour identifier les points bas potentiels des prix. Afin de filtrer les faux signaux, elle combine également une moyenne mobile et un stochastique multi-timeframes pour confirmation. Une fois le signal de point bas confirmé, des ordres longs sont progressivement ouverts légèrement en dessous de ce point, suivant le principe de la pyramide de suivi. La stratégie permet d'ouvrir jusqu'à 12 ordres de suivi, dont la taille augmente séquentiellement, ce qui permet de diversifier efficacement le risque. Tous les ordres sont fermés suivant un stop-loss global, tout en permettant un take-profit individuel pour chaque ordre. Pour renforcer le contrôle du risque, un stop-loss global basé sur un pourcentage des capitaux propres du compte est également mis en place.

Principe de la stratégie

La stratégie se compose de trois modules principaux : le module d'identification des points bas, le module de pyramide de suivi, et le module de contrôle des risques.

Module d'identification des points bas : il utilise la différence entre le RSI et sa moyenne exponentielle (EMA) pour repérer les points bas potentiels. Pour améliorer la précision, un indicateur de moyenne mobile et un stochastique multi-timeframes sont introduits pour filtrer les signaux. Le signal de point bas n'est validé que lorsque le prix est inférieur à la moyenne mobile et que la ligne K du stochastique est inférieure à 30.

Module de pyramide de suivi : c'est le cœur de la stratégie. Une fois le signal de point bas confirmé, le premier ordre est ouvert à un niveau 0,1 % en dessous de ce point bas. Ensuite, tant que le prix continue de baisser et qu'il se situe à un certain pourcentage en dessous du prix d'entrée moyen, des ordres longs supplémentaires sont ajoutés. La taille des nouveaux ordres augmente progressivement. Par exemple, le troisième ordre a une taille trois fois supérieure à celle du premier. Cette approche de pyramide permet de lisser le risque. La stratégie permet jusqu'à 12 ordres de suivi.

Module de contrôle des risques : il comprend principalement trois aspects. Premièrement, un stop-loss global calculé en fonction du plus haut sur une période récente. Tous les ordres sont stoppés simultanément à ce niveau. Deuxièmement, un take-profit indépendant pour chaque ordre, permettant de fixer un pourcentage par rapport au prix d'entrée. Troisièmement, un stop-loss global basé sur un pourcentage des capitaux propres, qui constitue la mesure de contrôle des risques la plus forte.

Avantages de la stratégie

- Réduction du risque individuel des ordres grâce à la pyramide de suivi, tout en diversifiant le risque global.

- Combinaison de plusieurs indicateurs pour améliorer la précision de l'identification des points bas.

- Les fonctions de stop-loss global, take-profit et stop-loss suiveur permettent un contrôle efficace des risques.

- Le mécanisme de stop-loss basé sur un pourcentage des capitaux propres protège le compte contre des pertes importantes.

- Possibilité d'ajuster les paramètres pour trouver un équilibre entre risque et rendement.

Risques de la stratégie

- La précision de l'identification des points bas reste limitée, pouvant entraîner des entrées manquées ou des faux signaux.

- L'ajout d'ordres peut exposer à des mouvements défavorables et aggraver les pertes.

- Un cycle de fonctionnement relativement long est nécessaire pour que la stratégie montre ses avantages.

- Un paramétrage inapproprié peut conduire à un contrôle des risques insuffisant.

Pour atténuer ces risques, plusieurs optimisations sont possibles :

- Modifier ou ajouter des indicateurs pour améliorer la précision de l'identification des points bas.

- Optimiser les paramètres tels que le nombre d'ordres, l'intervalle, le niveau de take-profit, afin de réduire le risque par ordre.

- Réduire la largeur du stop-loss pour protéger les profits.

- Tester sur différents instruments, en privilégiant ceux avec une bonne liquidité et une volatilité élevée.

Pistes d'optimisation de la stratégie

La stratégie offre encore des possibilités d'amélioration :

- Introduire des techniques plus avancées, comme l'apprentissage automatique, pour identifier les points bas.

- Ajuster dynamiquement le nombre d'ordres, la largeur du stop-loss et d'autres paramètres en fonction des conditions du marché.

- Ajouter une stratégie de stop-loss dans une fourchette pour éviter l'élargissement des pertes.

- Ajouter un mécanisme de rentrée.

- Optimiser les paramètres de la stratégie pour les actions et les crypto-monnaies.

Conclusion

Cette stratégie réduit efficacement le risque individuel des ordres grâce à l'approche de pyramide de suivi, et les fonctions de stop-loss global, take-profit et stop-loss suiveur assurent un bon contrôle des risques. Cependant, il reste des marges d'amélioration dans l'identification des points bas. L'introduction de technologies plus avancées, l'ajout d'un paramétrage dynamique et une optimisation des paramètres pourraient considérablement améliorer le ratio risque/rendement de cette stratégie.

- 1