Stratégie de trading de l'oscillateur arc-en-ciel

Aperçu

La stratégie de l'oscillateur arc-en-ciel utilise principalement plusieurs moyennes mobiles lissées exponentiellement et des indicateurs oscillateurs pour construire des canaux d'oscillation multicouches, générant des signaux haussiers et baissiers clairs et gradués. Il s'agit d'une stratégie de suivi de tendance. La stratégie combine les indicateurs RSI, CCI, Stochastic et MA pour évaluer la tendance générale du marché et les zones de surachat et survente, ce qui en fait une stratégie d'évaluation multifactorielle.

Principe de la stratégie

- Calculer la moyenne pondérée des trois indicateurs RSI, CCI et Stochastic pour construire un indicateur oscillateur composite appelé Magic ;

- Appliquer un lissage exponentiel multiple à l'indicateur Magic pour obtenir deux courbes : sampledMagicFast et sampledMagicSlow ;

- sampledMagicFast représente la moyenne rapide, sampledMagicSlow la moyenne lente ;

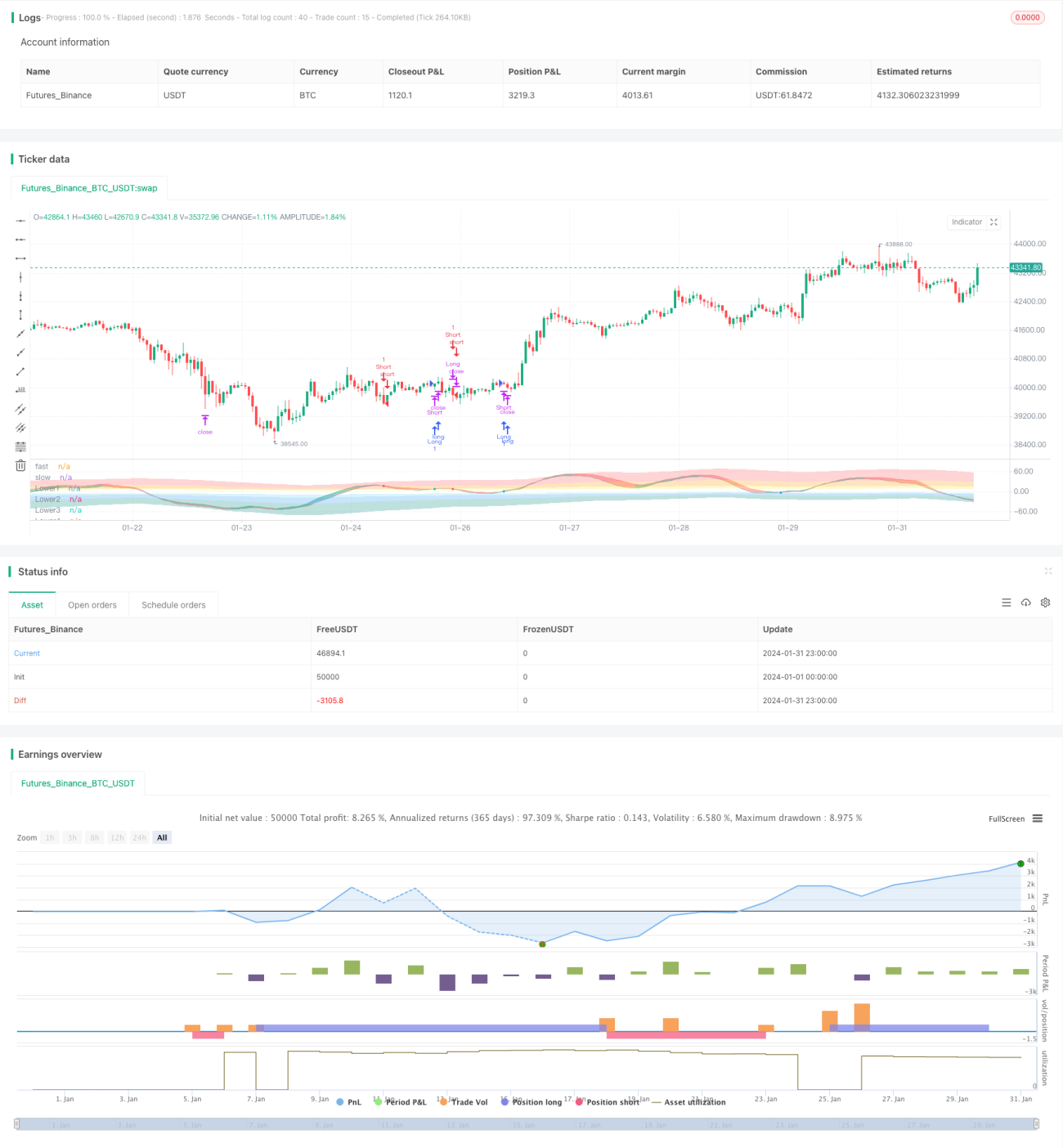

- Un signal d'achat est généré lorsque sampledMagicFast croise au-dessus de sampledMagicSlow ;

- Un signal de vente est généré lorsque sampledMagicFast croise en dessous de sampledMagicSlow ;

- Calculer la direction du changement de sampledMagicFast de la dernière barre par rapport à la barre précédente pour déterminer la tendance actuelle ;

- En fonction de la direction de la tendance et du croisement de sampledMagicFast et sampledMagicSlow, déterminer les points d'entrée et de sortie.

Avantages de la stratégie

- Combine plusieurs indicateurs pour évaluer la tendance générale du marché, améliorant ainsi la précision des signaux ;

- Basée sur des indicateurs MA lissés, elle réduit efficacement le bruit des signaux ;

- Les signaux d'oscillation sont progressifs et clairs, faciles à utiliser ;

- En intégrant un filtre de tendance, elle peut être configurée pour le suivi de tendance ou le retournement ;

- Possibilité de personnaliser l'intensité des zones de surachat et survente, offrant une grande adaptabilité.

Risques de la stratégie

- Un mauvais réglage des paramètres peut rendre les courbes trop lissées, entraînant un manque du meilleur point d'entrée ;

- Un réglage inapproprié des zones de surachat et survente peut entraîner de longues périodes sans position ;

- La défaillance de certains indicateurs dans l'évaluation multifactorielle peut affaiblir l'efficacité des signaux.

Solutions correspondantes :

- Optimiser les paramètres pour obtenir un lissage modéré des courbes ;

- Ajuster l'intensité des zones de surachat/survente pour réduire les périodes sans position ;

- Tester la capacité prédictive de chaque indicateur et ajuster les pondérations en conséquence.

Axes d'optimisation de la stratégie

- Ajuster dynamiquement les paramètres des indicateurs en fonction des caractéristiques du marché ;

- Introduire des méthodes d'apprentissage automatique pour optimiser automatiquement la combinaison des pondérations des indicateurs ;

- Ajouter des facteurs tels que le volume et la volatilité pour filtrer les signaux d'entrée.

Résumé

La stratégie de l'oscillateur arc-en-ciel combine les signaux de plusieurs indicateurs et améliore la stabilité grâce au lissage exponentiel. Elle peut être configurée pour s'adapter aux marchés en tendance et en range, ou être utilisée uniquement pour des mouvements de range sur un actif spécifique. L'optimisation des paramètres et l'extension des indicateurs permettent d'améliorer encore la qualité des signaux. Dans l'ensemble, cette stratégie est logique, simple à utiliser et facile à maîtriser.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © businessduck

//@version=5

strategy("Rainbow Oscillator [Strategy]", overlay=false, margin_long=100, margin_short=100, initial_capital = 2000)

bool trendFilter = input.bool(true, 'Use trend filter')

float w1 = input.float(0.33, 'RSI Weight', 0, 1, 0.01)

float w2 = input.float(0.33, 'CCI Weight', 0, 1, 0.01)

float w3 = input.float(0.33, 'Stoch Weight', 0, 1, 0.01)

int fastPeriod = input.int(16, 'Ocillograph Fast Period', 4, 60, 1)

int slowPeriod = input.int(22, 'Ocillograph Slow Period', 4, 60, 1)- 1