Stratégie de trading multi-timeframes basée sur des indicateurs de compression

Aperçu

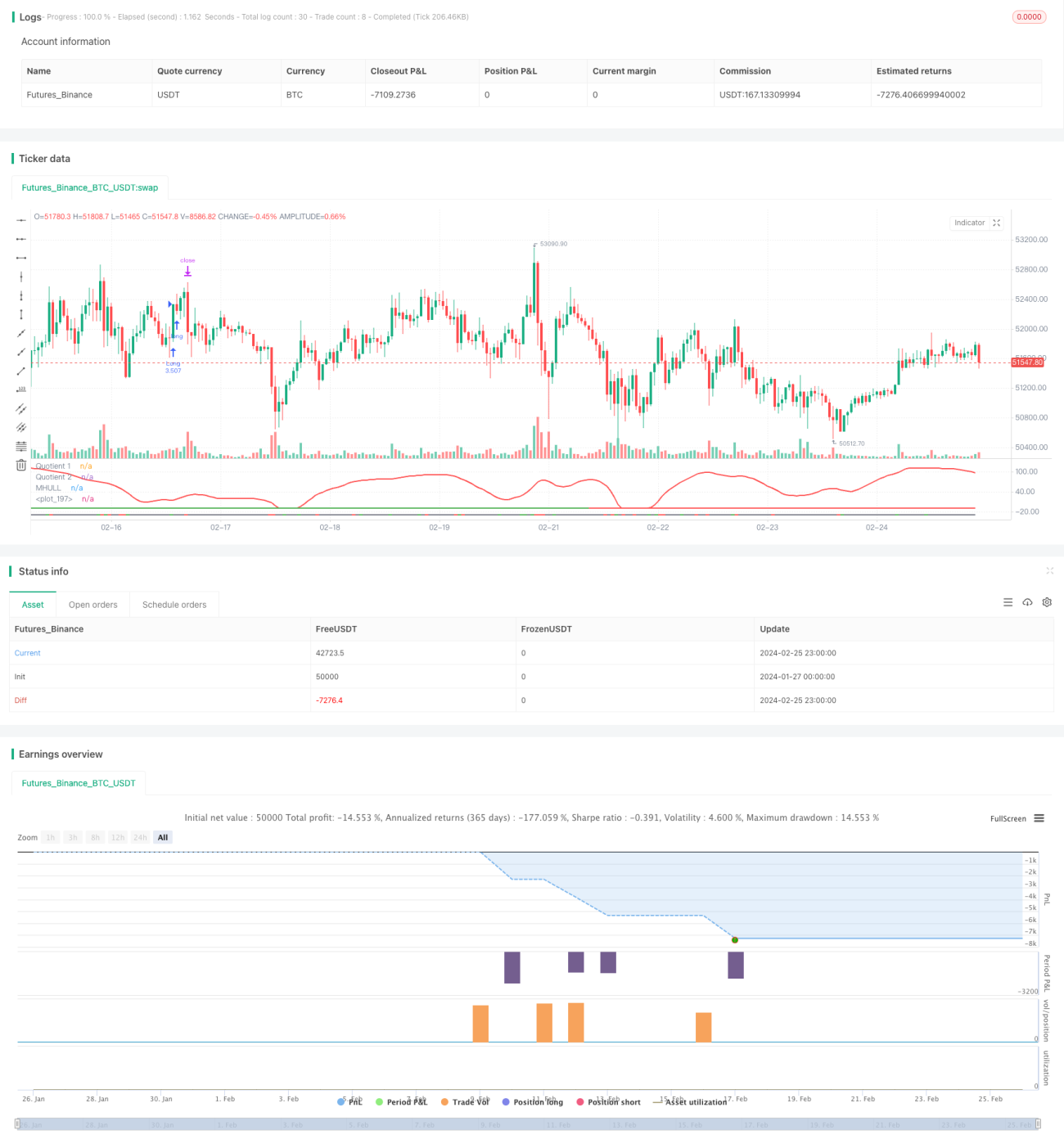

Cette stratégie combine trois indicateurs – le Boom Hunter, le Hull Suite et l’oscillateur de volatilité – pour réaliser un suivi de tendance et des transactions de rupture sur plusieurs cadres temporels. Elle est adaptée aux actifs numériques comme le Bitcoin, qui présentent une forte volatilité et des mouvements de prix soudains.

Principe

La logique centrale de la stratégie repose sur les trois indicateurs suivants :

-

Boom Hunter : un oscillateur utilisant une technique de compression d’indicateurs, qui génère des signaux d’achat et de vente par le croisement de deux indicateurs (Quotient1 et Quotient2).

-

Hull Suite : un ensemble de moyennes mobiles lissées, dont la bande médiane et les bandes supérieure/inférieure permettent de déterminer la direction de la tendance.

-

Oscillateur de volatilité : un indicateur oscillateur quantifiant les informations de volatilité des prix.

La règle d’entrée en position est la suivante : lorsque les deux Quotients du Boom Hunter effectuent un croisement haussier ou baissier, le prix doit en même temps franchir la bande médiane du Hull Suite et diverger par rapport à la bande supérieure ou inférieure, tandis que l’oscillateur de volatilité se trouve en zone de surachat ou survente. Cela permet de filtrer les faux signaux de rupture et d’améliorer la précision des entrées.

Le stop-loss est défini en recherchant le plus bas ou le plus haut sur une période donnée (20 bougies par défaut). Le take-profit est obtenu en multipliant le pourcentage du stop-loss par le ratio de profit cible (3 fois par défaut). La taille de la position est calculée en fonction d’un pourcentage du capital total (3 % par défaut) et de l’amplitude du stop-loss propre à l’instrument.

Avantages

- Extraction des principaux signaux de trading à l’aide de la technique de compression des indicateurs, augmentant la probabilité de gains.

- Validation croisée par plusieurs indicateurs pour éviter les faux signaux de rupture et déterminer précisément la direction de la tendance.

- Stop-loss et take-profit dynamiques permettant un suivi de tendance avec un risque maîtrisé.

- Utilisation d’un indicateur de volatilité pour garantir des transactions dans des environnements de forte volatilité.

- Analyse multi‑temporelle améliorant la stabilité de la stratégie.

Risques

- L’indicateur Boom Hunter peut souffrir de distorsions liées à la compression, générant des signaux erronés.

- La bande médiane du Hull Suite peut présenter un retard, ne suivant pas immédiatement les variations de prix.

- En période de baisse de volatilité, des opportunités de trading peuvent être manquées ou des pertes peuvent survenir lors du débouclage des positions.

Solutions :

- Ajuster les paramètres de l’indicateur de compression pour équilibrer sa sensibilité.

- Essayer d’utiliser des moyennes mobiles exponentielles (comme l’EHMA) à la place de la bande médiane.

- Ajouter d’autres indicateurs de confirmation pour éviter les erreurs induites par la volatilité.

Optimisation

La stratégie peut être optimisée selon plusieurs axes :

-

Optimisation des paramètres : modifier les périodes, les coefficients de compression, etc., pour obtenir la meilleure combinaison.

-

Optimisation du cadre temporel : tester différentes unités de temps (1 minute, 5 minutes, 30 minutes, etc.) afin de trouver la plus adaptée.

-

Optimisation de la taille de position : varier le pourcentage alloué à chaque transaction pour déterminer l’utilisation la plus efficace du capital.

-

Optimisation du stop-loss : ajuster la distance du stop-loss selon les paires de trading pour obtenir le meilleur rapport risque/rendement.

-

Optimisation des conditions : ajouter ou retirer des filtres pour obtenir des entrées plus précises.

Résumé

En combinant le Boom Hunter, le Hull Suite et l’oscillateur de volatilité, cette stratégie réalise un suivi de tendance sur plusieurs cadres temporels, capable d’identifier efficacement les mouvements brutaux de prix. Elle convient aux actifs numériques à forte volatilité. Avec un risque maîtrisé et des optimisations possibles (paramètres, filtres, stop-loss, etc.), cette stratégie offre une grande robustesse et une bonne adaptabilité en conditions réelles.

- 1