Stratégie Kuberan : Stratégie de confluence pour la maîtrise du marché

Aperçu de la stratégie

La stratégie Kuberan, développée par Kathir, est une puissante stratégie de trading qui intègre plusieurs techniques d'analyse pour former une approche unique et robuste. Nommée d'après le dieu de la richesse Kuberan, elle symbolise l'objectif d'enrichir le portefeuille des traders.

Kuberan n'est pas seulement une stratégie, mais un système de trading complet. Elle combine l'analyse de tendance, les indicateurs de momentum et les indicateurs de volume pour identifier des opportunités de trading à haute probabilité. En exploitant la synergie de ces éléments, Kuberan fournit des signaux d'entrée et de sortie clairs, adaptés aux traders de tous niveaux.

Principe de la stratégie

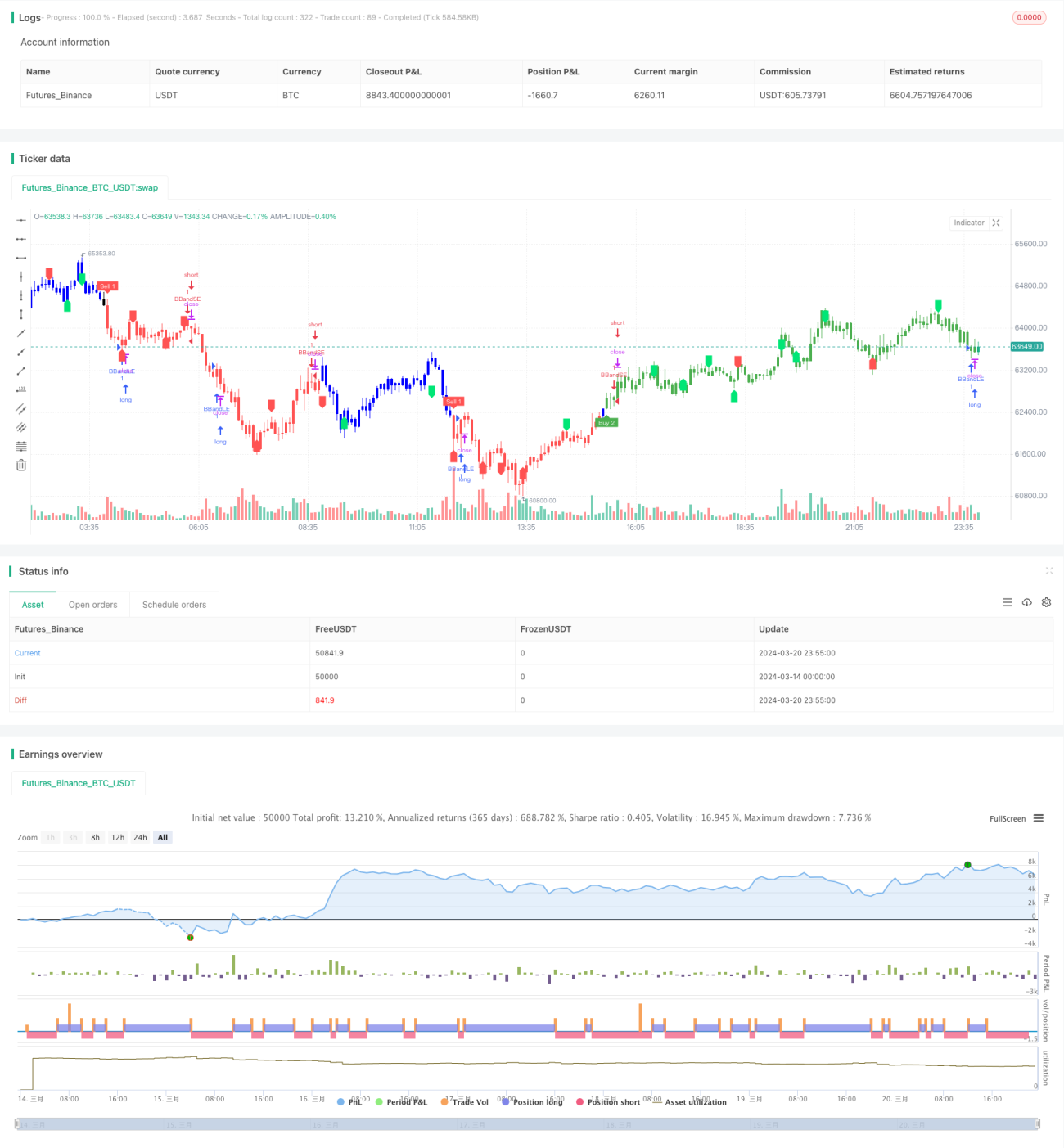

Le cœur de la stratégie Kuberan repose sur le principe de confluence de multiples indicateurs. Elle utilise une combinaison unique d'indicateurs qui travaillent ensemble pour réduire le bruit et les faux signaux. Plus précisément, la stratégie emploie les composants clés suivants :

- Détermination de la direction de tendance : En comparant le prix actuel aux niveaux de support et de résistance, elle détermine la direction de la tendance en cours.

- Niveaux de support et résistance : Elle identifie les niveaux clés de support et résistance à l'aide de l'indicateur zigzag et des points pivots.

- Détection de divergence : En comparant l'évolution des prix avec les indicateurs de momentum, elle détecte les divergences, signalant un possible retournement de tendance.

- Adaptation à la volatilité : Elle ajuste dynamiquement les niveaux de stop-loss via l'indicateur ATR pour s'adapter à différentes volatilités du marché.

- Analyse des motifs de chandeliers : Des configurations spécifiques de bougies confirment les signaux de tendance et de retournement.

En considérant l'ensemble de ces facteurs, la stratégie Kuberan s'adapte automatiquement à divers environnements de marché pour capturer des opportunités de trading à haute probabilité.

Avantages de la stratégie

- Confluence multi-indicateurs : Kuberan exploite la synergie de plusieurs indicateurs, améliorant considérablement la fiabilité des signaux et réduisant les interférences parasites.

- Forte adaptabilité : Grâce à des paramètres dynamiques, la stratégie s'adapte aux conditions changeantes du marché et reste efficace.

- Signaux clairs : Kuberan fournit des signaux d'entrée et de sortie explicites, simplifiant le processus de décision de trading.

- Robustesse en backtest : La stratégie a subi des backtests historiques rigoureux et démontre une performance stable dans diverses conditions de marché.

- Large applicabilité : Kuberan convient à plusieurs marchés et instruments, sans se limiter à un actif spécifique.

Risques de la stratégie

- Sensibilité aux paramètres : La performance de Kuberan est sensible au choix des paramètres ; un réglage inapproprié peut entraîner une baisse de performance.

- Événements imprévus : La stratégie se base principalement sur des signaux techniques et a une capacité limitée à gérer les événements fondamentaux soudains.

- Risque de surapprentissage : Une optimisation excessive sur des données historiques peut rendre la stratégie trop adaptée au passé et moins performante sur les marchés futurs.

- Risque de levier : L'utilisation d'un levier élevé expose au risque de liquidation en cas de drawdown important.

Pour atténuer ces risques, des mesures appropriées peuvent être prises, comme l'ajustement périodique des paramètres, la définition de stops-loss raisonnables, un contrôle modéré du levier et la surveillance des changements fondamentaux.

Pistes d'optimisation

- Optimisation par apprentissage automatique : Introduire des algorithmes de machine learning pour optimiser dynamiquement les paramètres de la stratégie et améliorer son adaptabilité.

- Intégration de facteurs fondamentaux : Prendre en compte l'analyse fondamentale dans les décisions de trading pour faire face aux situations où les signaux techniques échouent.

- Gestion de portefeuille : Au niveau de la gestion de capital, intégrer la stratégie Kuberan dans un portefeuille pour former une couverture efficace avec d'autres stratégies.

- Optimisation par segment de marché : Personnaliser les paramètres de la stratégie en fonction des caractéristiques de chaque instrument de marché.

- Transformation en trading haute fréquence : Adapter la stratégie à une version haute fréquence pour capturer davantage d'opportunités de trading à court terme.

Conclusion

Kuberan est une stratégie de trading puissante, fiable et sécurisée. Elle combine astucieusement plusieurs méthodes d'analyse technique et, grâce au principe de confluence des indicateurs, excelle dans la capture des tendances et l'identification des points de retournement. Bien qu'aucune stratégie ne soit exempte de risques, Kuberan a prouvé sa robustesse lors des backtests. Avec des mesures appropriées de contrôle des risques et d'optimisation, cette stratégie peut aider les traders à prendre l'avantage sur les marchés et à favoriser une croissance stable et durable de leur portefeuille.

/*backtest

start: 2024-03-14 00:00:00

end: 2024-03-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue- 1