Strategi Penembusan Rata-Rata Bergerak Tingkat Tinggi

Ikhtisar

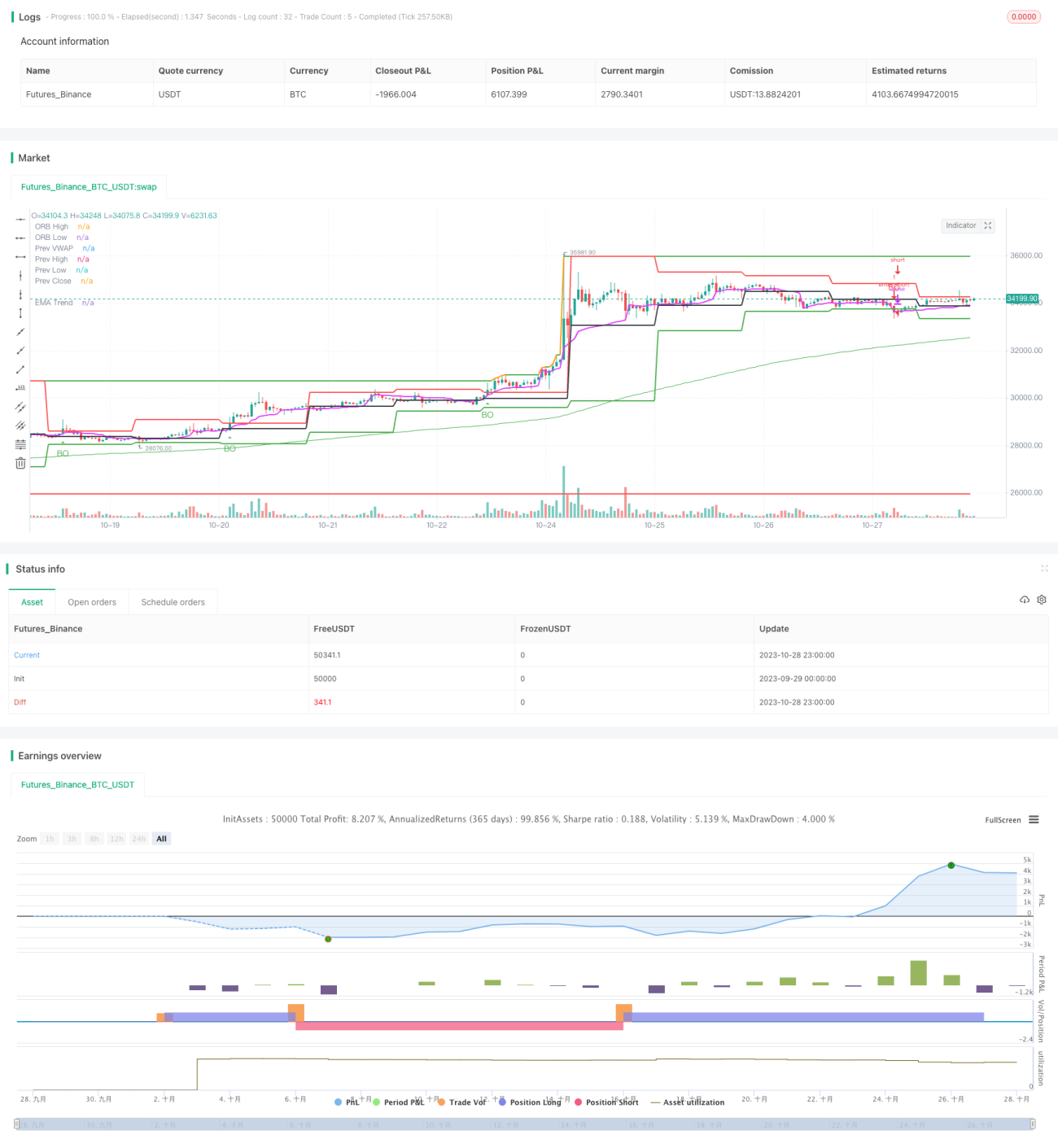

Ide utama dari strategi ini adalah memanfaatkan penembusan moving average pada timeframe yang lebih tinggi untuk melakukan trading tren. Pada kerangka waktu yang lebih tinggi, ketika harga menembus di atas atau di bawah moving average, awal tren dapat diidentifikasi, dan pada saat itu arah yang sesuai dapat dipilih untuk diikuti.

Prinsip Strategi

Strategi ini dikembangkan menggunakan bahasa Pine Script, terutama terdiri dari beberapa bagian berikut:

-

Parameter Input

Mendefinisikan parameter periode moving average

period, dengan nilai default 200; mendefinisikan parameter kerangka waktu candletimeframe, dengan nilai default harian "D". -

Perhitungan Moving Average

Menggunakan fungsi

ta.emauntuk menghitung Exponential Moving Average. -

Deteksi Penembusan

Menggunakan fungsi

ta.crossoverdanta.crossunderuntuk mendeteksi apakah harga menembus di atas atau di bawah moving average. -

Plot Sinyal

Ketika terjadi penembusan, menggambar panah ke atas atau ke bawah pada candle.

-

Open/Close Posisi

Ketika terjadi penembusan, buka posisi sesuai arah, dan tutup posisi setelah jarak stop loss dua kali tercapai.

Strategi ini terutama mengandalkan kemampuan identifikasi tren dari moving average pada timeframe yang lebih tinggi, dengan operasi penembusan sederhana untuk mengikuti tren. Ini adalah strategi penembusan yang cukup tradisional.

Analisis Keunggulan

Strategi ini memiliki beberapa keunggulan berikut:

-

Konsep sederhana, mudah dipahami dan dikuasai.

-

Hanya mengandalkan satu indikator moving average, penyesuaian parameter mudah.

-

Operasi penembusan cenderung membentuk tren, tidak sering melakukan trading.

-

Periode yang lebih tinggi menunjukkan tren besar dengan jelas, tidak mudah terpengaruh fluktuasi jangka pendek.

-

Dapat dikonfigurasi dengan kombinasi kerangka waktu yang berbeda, sesuai untuk berbagai instrumen.

-

Dapat dengan mudah melacak banyak instrumen, sulit terjebak semuanya secara bersamaan.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

-

Sinyal penembusan mungkin palsu, tidak dapat menyaring fluktuasi pasar secara efektif.

-

Tidak dapat memanfaatkan peluang jangka pendek untuk mendapatkan keuntungan.

-

Ketika arah utama salah, kerugian bisa cukup parah.

-

Ketika periode moving average tidak cocok dengan periode trading, dapat terjadi overtrading atau kebocoran.

-

Tidak dapat melakukan stop loss real-time, kemungkinan kerugian membesar cukup besar.

Solusi untuk risiko yang sesuai meliputi: menggabungkan indikator tren, menambahkan filter, memperpendek periode hold posisi, menyesuaikan posisi stop loss secara dinamis, dll.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Menambahkan kombinasi indikator tren, seperti MACD, KD, dll., untuk meningkatkan keandalan penembusan.

-

Menambahkan filter seperti volume perdagangan atau Bollinger Bands untuk menghindari penembusan palsu.

-

Mengoptimalkan pencocokan parameter periode sehingga periode hold posisi lebih cocok dengan periode tren.

-

Menambahkan strategi stop loss real-time, menggunakan trailing stop untuk mengontrol kerugian per posisi.

-

Mempertimbangkan penggunaan teknik machine learning untuk optimasi parameter secara dinamis.

-

Mencoba kombinasi alokasi aset yang beragam untuk meningkatkan stabilitas secara keseluruhan.

Kesimpulan

Secara keseluruhan, strategi ini cukup sederhana dan praktis. Dengan menggunakan penembusan moving average sederhana untuk mengikuti tren, strategi ini mudah dikuasai dan dapat menjadi salah satu strategi awal untuk trading kuantitatif. Namun, masih ada beberapa masalah yang perlu diperbaiki melalui kombinasi indikator, optimasi parameter, stop loss dinamis, dll., agar strategi lebih stabil dan efisien. Strategi ini memiliki potensi optimasi dan ekstensibilitas yang besar.

- 1